Bangladesh's foreign-debt repayments are projected to aggressively outpace fresh foreign-fund receipts within the next three fiscal years, analysts alert.

Data from the Finance Division and the Economic Relations Division (ERD) reveal a looming fiscal squeeze, culminating in FY2028-29 when the country's total external debt -servicing obligations will peak at an unprecedented level.

According to government projections, Bangladesh is likely to need to repay a staggering amount of US$4.276 billion in principal against its total outstanding debts alone during the period up to FY2029. Compounding this burden, the government must simultaneously shell out nearly US$3.289 billion (Tk 403 billion) in interest payments.

This brings the total external debt-servicing liability for FY2029 to a historic high of US$7.565 billion, nearly doubling the US$4.09 billion record registered in FY2024-25.

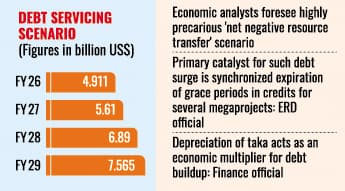

According to government projection, it may have need to repay a total of US$4.911 billion as principal and interest for the total external outstanding in the last FY2026, while $5.61 billion in the current FY2027, US$6.89 billion in FY2028 and $7.565 billion in FY2029.

Out of the loans, the interest payments have been rising faster than the principal amounts as the government is projected to repay almost double to $3.289 billion in the FY2029 from that of $1.79 billion in FY2025.

According to ERD data, Bangladesh has repaid $4.13 billion worth of funds-principal and interest combined-in the first 11 months (Jul-May) of the just-past fiscal year.

The country received $4.14 billion worth of foreign loans.

ERD officials have claimed that the total fresh loan disbursement in the last month, June, of the past FY2026 by the foreign lenders was to rise.

Economic analysts warn that this fiscal imbalance for higher growth in external loan repayments than lower inflow of foreign credits will create a highly precarious "net negative resource transfer" scenario.

For decades, Bangladesh has relied on incoming foreign aid and project loans to comfortably cover its older debts while funding new infrastructure.

"Within the next few years, however, the country will actively export more hard currency to service past loans than it receives in new foreign disbursements, creating a severe drain on national liquidity," one analyst has alerted.

A senior ERD official has said the primary catalyst for this debt surge is the synchronized expiration of grace periods in credits for several megaprojects.

Massive, capital-intensive initiatives funded over the last decade -- including the Rooppur Nuclear Power Plant, the Dhaka Metro Rail lines, and the Padma Rail Link -- are gradually entering into their principal -repayment phases, he added.

Furthermore, the global shift away from concessional borrowing has worsened the crisis, the official said.

"As Bangladesh graduated from low-income status, access to soft, fixed-rate loans dwindled. The country has been forced to rely on market-based, floating-rate credits tied to index rates like the Secured Overnight Financing Rate (SOFR)."

With global interest rates remaining elevated, the cost of servicing these floating-rate debts has ballooned exponentially, the ERD official further noted.

While the government faces a dollar deficit internationally, it faces a massive budgetary strain domestically. The steep depreciation of the Bangladeshi taka over the last few years has acted as an economic multiplier for this debt, a senior Ministry of Finance (MoF) official has said.

"Because external debt must be settled in US dollar, the government requires vastly more local revenue to buy the same amount of foreign currency. This is directly reflected in the skyrocketing interest budget."

The Tk 403 billion to be required just for interest in FY2029 will consume a massive chunk of national revenue, leaving significantly less fiscal space for annual development programmes, education, and healthcare, the MoF official added.

Economists and policy advisers stress that the next 24 to 36 months are critical for structural reform.

Economists urge the government to mobilise the estimated US$41.7 billion currently sitting idle in the undisbursed foreign- loan pipeline to counter the negative inflow-outflow balance.

Policy Exchange Bangladesh Chairman Dr Masrur Reaz thinks overall domestic tax collection to ensure the national budget can absorb the interest shock without crippling domestic bank borrowing.

"Enforce strict restrictions on high-interest, short-term commercial borrowing, prioritizing long-term concessional lines instead," he suggests.

Without swift structural interventions to boost export earnings, stabilise foreign -exchange reserves, and reform revenue generation, the impending debt-servicing spike risks pushing the country into a prolonged macroeconomic recession, the young economist says.

kabirhumayan10@gmail.com