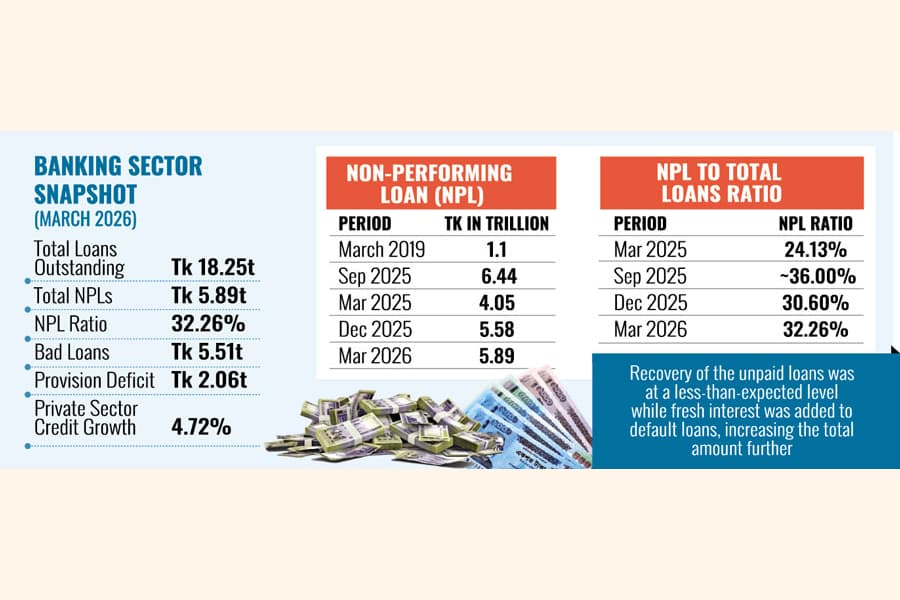

Extensive policy support and partial writeoff facility prove ineffective as the volume of classified loans in Bangladesh's banking sector makes a quantum leap again by around Tk 315 billion in just three months to March.

With such fresh buildup of non-performing loans (NPLs), the aggregate bloats to around Tk 5.89 trillion by the end of March 2026, accounting for 32.26 per cent of the entire loans worth Tk 18.25 trillion disbursed by the country's all commercial banks.

By the end of December last, the share of NPLs was recorded at 30.60 per cent.

The highest level of defaulted loans in the country's history was recorded in September 2025. At the time, nearly 36 per cent of total loans had become defaulted. In monetary terms, this amounted to Tk 6.44 trillion.

Constrained by such a huge volume of non-performing assets, banks have become extremely conservative and limit their credit supply to the borrowers. Besides, banks' profitability is also dented as they have to maintain a portion of funds for NPL provisioning.

Sources at Bangladesh Bank (BB), the country's central bank, have said the recovery of the unpaid loans was at a less-than-expected level while fresh interest was added to default loans, increasing the total amount further.

The sources cite reasons like persisting energy crisis, exchange-rate shocks, higher lending rate and disruption in global supply chain due to various external shocks behind the NPL buildup.

Spokesperson for the central bank Arief Hossain Khan says private- sector credit growth has been disappointing for months. As a result, interest on existing default loans has been added, causing both the total amount and the ratio of defaulted loans to increase.

"Defaulted loans were not recovered to the extent they were expected to be, increasing the total amount further," adds Mr. Khan, also executive director of the BB.

According to the March-end NPL-related data released by the BB on Tuesday, the share of classified loans rose to 32.26 per cent of the total outstanding loans during the period under review from 24.13 per cent a year before.

Classified loans include substandard, doubtful and bad/loss of total outstanding credits. Of the classified loans, the share of bad loans was 93.69 per cent or Tk 5.51 trillion.

In terms of the category of banks, the ratio of classified loans in the state-owned commercial banks (SoCBs), like on other occasions, remained high. During the period, the total amount of NPLs with six state-owned banks rose to Tk 1.50 trillion or 45.85 per cent.

On the other hand, the total amount of classified loans with private commercial banks (PCBs) comes to Tk 4.16 trillion or 30.11 per cent until March last.

The NPLs of nine foreign commercial banks (FCBs), on the other hand, recorded Tk 32.63 billion or 4.82 per cent during the period under review.

The classified loans with three specialised banks (SBs), however, rose to Tk 192 billion (40.72 per cent) by end of March last from 185 billion in the last quarter of the calendar year 2025.

But the most concerning part was provisioning shortfall with 44.54 per cent of the classified loans lacking provisioning coverage. The volume of provisioning deficit reached Tk 2.06 trillion.

Such faster NPL ballooning in banks caused serious concerns to bankers who fear further pressure on their liquidity situation in the months ahead.

Managing director and chief executive officer of Mutual Trust Bank (MTB) Syed Mahbubur Rahman says the economic vulnerability continues to grow due to both internal and external factors and these severely impacted businesses here.

As a matter of fact, the experienced banker notes, the credit demand by private sector reached a historic low of 4.72 per cent in March last and this economic downturn hit hard many SMEs (small and medium enterprises) in recent times.

Citing the NPL data trend, Mr. Rahman says, "Both volume and ratio of NPL normally go up in the first quarter of a calendar year but it drops at yearend when banks get busy for partial writeoff to maintain a healthy balance sheet."

Dr Md. Touhidul Alam Khan, Managing Director & CEO of NRBC Bank, attributes the current NPL surge to a convergence of long-hidden problems and fresh economic pressures that have created a "perfect storm for the banking sector".

At the heart of the crisis lies the emergence of previously concealed legacy bad loans. Years of financial irregularities involving major corporate conglomerates are finally surfacing under improved oversight, revealing the true extent of historical mismanagement that was artificially kept off balance sheets.

"The situation has been further complicated by the recent expiration of pandemic-era moratoriums and regulatory relief measures. As these protective policies ended, banks were forced to reclassify previously deferred accounts, causing a dramatic spike in reported NPLs that reflects both old problems and new realities." the banker explains.

He says economic headwinds have intensified the challenge, with persistent inflation, rising borrowing costs, and global trade disruptions squeezing business cash flows.

Even legitimate enterprises are struggling to service their debt obligations in this harsh operating environment marked by "political instability and economic uncertainty".

"Underlying these immediate pressures are systemic governance failures, including weak risk-management practices, poor credit- evaluation systems, and the corrosive influence of political interference in lending decisions. This has fostered a troubling "culture of default" where influential borrowers exploit institutional weaknesses to avoid repayment without consequences," Dr Khan says.

jubairfe1980@gmail.com