Transfer pricing law starts paying off

Seven out of 1,000 MNCs contribute Tk 100m addl taxes

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

After five years of its framing, transfer pricing law has started showing results, contributing additional taxes worth Tk 100 million.

At least seven multinational companies (MNCs) paid income taxes through re-adjustment of their tax files following the transfer pricing guidelines, officials said.

The Transfer Pricing Cell (TPC) under the National Board of Revenue (NBR) has found the MNCs including a mobile phone operator, four readymade garment exporters and two branch offices of a global electronics brand.

Officials said the revenue authorities received the additional taxes against the tax returns of MNCs submitted during 2017-18 tax assessment year.

They expected the amount of tax by MNCs to rise substantially by June 30, 2018.

Transfer pricing is a new concept to be dealt with by the tax administration. It usually takes three to four years to come into full operation as capacity development of taxmen is needed, officials said.

Talking to the FE on Thursday, NBR chairman Md Mosharraf Hossain Bhuiyan said the multinationals have started paying taxes voluntarily after the framing of the law.

"Now, the MNCs have felt the need for cross-checking their paid taxes on international transaction. It's an achievement of taxmen," he said.

The NBR chairman said the Netherlands Tax and Customs Administration has assured the board of providing technical cooperation for building staff expertise on the topic.

"We've designated seven officials as transfer pricing officers for the cell," he said.

The MNCs have voluntarily paid the amount conducting self-assessment of their international transactions.

A senior official of the cell said the outcome came after the wing took various steps to encourage MNCs to increase their voluntary compliance.

The cell will encourage MNCs to follow the law willingly so that foreign investors remain comfortable, he said.

The board held several seminars with the Chief Financial Officers (CFOs) of the MNCs to make them aware of the provisions of the law, he added.

The NBR framed the law in 2012 to check tax evasion and capital flight by MNCs through the misuse of transfer pricing system.

In 2014, the NBR set up the cell, which was almost non-functional until 2016 due mainly to the lack of logistic support including database of comparable international transfer pricing, experts and dedicated manpower and proper initiative of the tax authorities.

Already, the cell has collected statements of international transaction (SIT) from the MNCs to audit those.

Some 120 MNCs have submitted their SITs to the NBR, although the cell found the number of MNCs in Bangladesh to be around 1,000.

According to law, all MNCs have to submit statements with their tax returns.

An official said they would encourage voluntary compliance so that MNCs adjust the tax amount if the price remained below at an arm's length price.

An arm's length transaction is one in which the buyers and sellers of a product act independently and do not have any relationship to each other, and it ensures that there is no collusion between the buyers and sellers.

In the approach, MNCs will assess whether their transactions fall under the international transaction category, if yes, then they will check the arm's length price using international database of pricing.

The official said the cell would conduct audit on those MNCs who did not carry out self-assessment.

Officials will also check whether MNCs conduct self-assessment properly, he said.

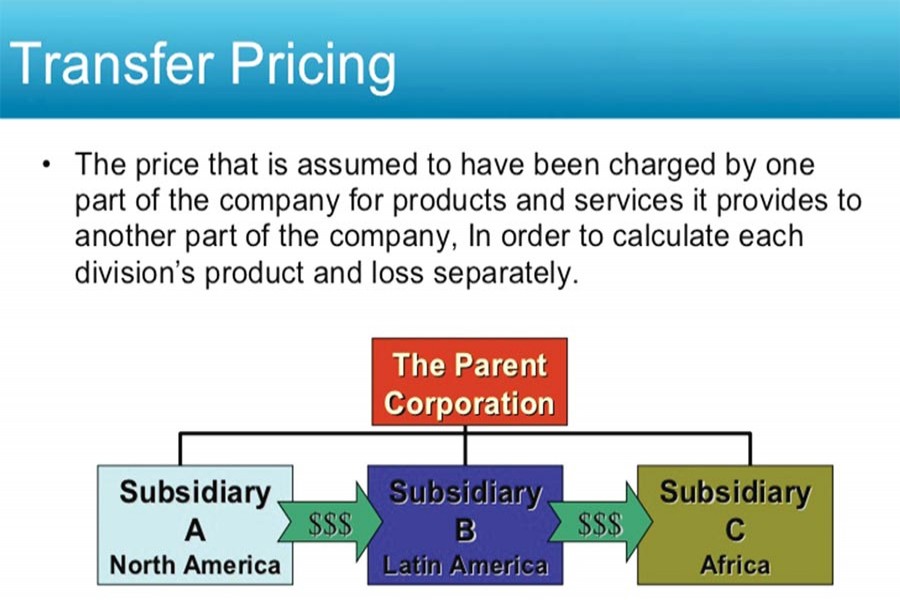

Transfer pricing takes place when an MNC pays or gets payment for the purchase or sale or transfers of any tangible or intangible output to any of its associated or subsidiary company in which the MNCs have substantial interest in any form.

There are allegations that many MNCs evade tax through transfer mispricing by over-invoicing and under-invoicing during transactions of goods and services within their associated companies.

They also evade taxes and drain capital from the country through transfer of dividend and profit to its parent companies located in tax heavens or low tax regime.

In South Asia, India was the first country to formulate transfer pricing regulations in 2001. It became fully operational in 2005-06.

Sri Lanka is the second nation in the region that introduced such regulations in 2008. However, the law was not fully operational until 2015.

At present, about 75 countries have adopted the transfer pricing regime.