Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Global Factoring (GF) or international factoring is a finance-packed mechanism for cross-border transactions through banks that combine working capital financing, credit risk protection and receivables discounting and collection services. The related parties in GF transactions include seller (exporter), buyer (importer), export factor (bank in exporters' country) and import factor (bank in importers' country). Unlike contemporary documentary transactions or letters of credit (LCs), GF transactions provide more security, flexibility, cost-effectiveness and ease in international transactions.

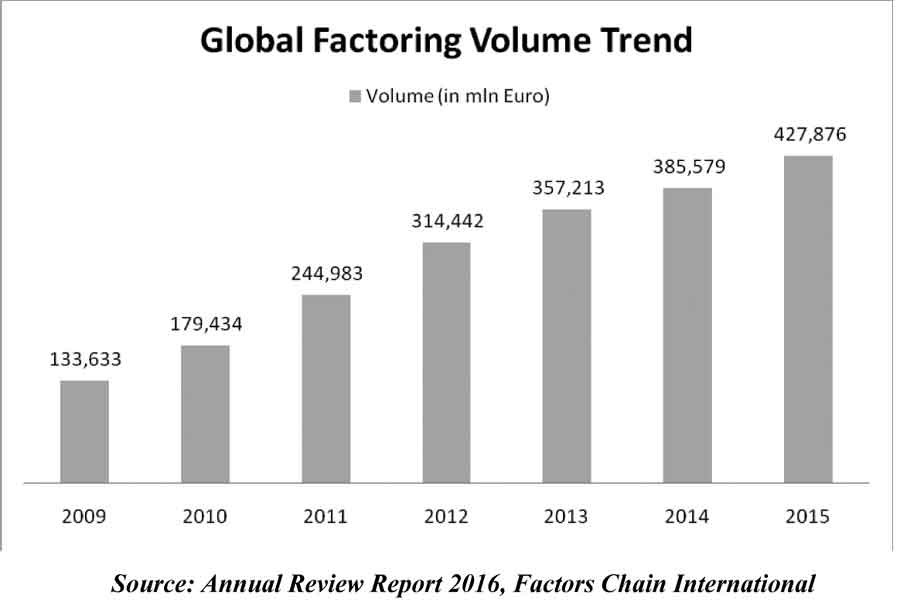

Domestic factoring began in the US in the mid-19th century. International factoring started in the 1960s, with European countries as its pioneers. For the year ending on December 31, 2013, total global factoring volume was $3 trillion or an increase of about 10 per cent over comparable 2012 data. The increase in cross-border factoring has been driven by a rise in open account trade, especially from suppliers in the developing world, pushed by major retailers/importers in the developed world, including acceptance of factoring as a suitable alternative to traditional forms of trade finance.

China has played an important role in this impressive international growth over the past five years, increasing at a rate of 54 per cent per annum and becoming the largest factoring market in the world today. Even though China now is the largest factoring market in the world, as a region Europe remains the largest factoring market on the globe. Europe accounts for a little over 60 per cent of the total $ factoring volume in the world as of the end of 2013. Of the $3 trillion total global factoring volume, Europe's total was about $1.9 trillion, according to the press release by Factors Chain International. Among the Asian economic giants, some have gained double digit growth - China (15 per cent), Hong Kong (15 per cent), Korea (61 per cent) and Singapore (20 per cent) in the same period.

So why has been Global Factoring transaction becoming the most thriving tool in international trade? Being in the 21st century, trading in international market has still been disrupted by currency systems, legislations, languages, business practices and other barriers. Mostly, small and medium importers/exporters of developing or emerging countries are trading over the frontier through letter of credit and open account system where the payment is received after many weeks or months causing hindrances in cash flows and risks of non-payment. Through GF transactions, being a small firm or a large corporation, an exporter can get credit protection facilitated by its bank (the export factor). The major role of the bank in importers' country (the import factor) is to collect money owed to exporters by approaching buyers in their own country, in their own language and in the locally accepted manner.

How does Global Factoring work? The aim of global factoring is to make international sales as easy as local transaction. Unlike LCs, it does not involve any confirming bank, negotiating bank and reimbursing bank and other roles. Basically, GF transactions process involves four parties - exporter, export factor, importer and import factor. For instance, ABC Apparels, a readymade garments manufacturer in Bangladesh, is interested to supply 100 shirts to AG Consumer Worldwide, Germany. To conduct a Global Factoring transaction, the process would be as follows:

- ABC Apparels (the exporter) receives purchase order or invoices from AG Consumer (the importer);

- ABC Apparels approaches its bank (export factor) for limit approval on the importer;

- The export factor forwards a request to factor arrangement to a pre-set and partner bank (import factor) in the country of the importer;

- The import factor checks the credit-worthiness and evaluates the risk of non-payment of AG Consumer and sets a credit limit;

- The import factor and export factor start a factor arrangement where AG Consumer asks the ABC Apparels/export factor to put a specific assignment clause on the invoices;

- ABC Apparels ships the underlying goods and prepares shipping documents;

- ABC Apparels submits shipping documents to the export factor and export factor provides discounted invoice value, let's assume 80 per cent;

- After receiving intimation from export factor, the import factor collects the full invoice value plus the charges from AG Consumer;

- After reimbursement, the export factor provides the remaining 20 per cent of the unpaid invoice value less the factoring charges to ABC Apparels.

In case of non-payment of the importer, the import factor is liable for making payment to the export factor within specified period. To start global factoring, both the export and import factors must be members of Factors Chain International (FCI).

What are the inherent risks for banks in Global Factoring? There are several risks involved both in export side and import side. In case of export factoring, the prime risks are - performance of exporters, payment risk of importer/import factor, fake/false invoices and documents; direct payment by the importer despite assignment of receivables etc. On the other hand, the import factor has to determine whether importers are sufficiently creditworthy and check their payments record using reliable, up-to-date information on solvency, payment ethics and organisational structure. Because, the import factor will have to pay the invoice value from their own funds to export factor in case of inability of importer to pay. Currently, GF transactions are being governed and regulated by General Rules for International Factoring (GRIF) by FCI which addresses several disputes and frauds in GF transactions. Disputes arise due to technical shortcomings of exporters, lack of experience, poor documentation, use of sub-standard materials and the like. In some transactions, both exporter and importer can be fraudsters, but the reputational risk of the factors can be costlier than the transactions.

Global factoring allows exporters to increase their cash flows and balance ratios by discounting invoices and collecting proceeds through export factors from the frozen accounts of foreign receivables. Since the import factor is liable to pay on behalf of the debtor/importer under credit guarantee, it apparently provides risk coverage to the exporters. As GF transaction involves fewer financial intermediaries unlike documentary credits, it is considered cost-effective and time-saving. On the other side, importers exercises flexibility through GF transactions through procuring goods based on open account terms. In case of opening letter of credit, the importer has to bear LC opening charges, negotiation fees, confirmation charges and most importantly, has to build up cash margin against each deals which are not prevalent in global factoring transactions.

Factors Chain International (FCI) has been the only global representative body for cross-border factoring transactions since 1968. This global factoring network consists of 400 financial intermediaries around 90 countries including 80 banks in China, 9 banks in India, 4 banks in Thailand and 3 banks in Japan. Since international trade transactions in Bangladesh are mostly routed through letter of credit, the banks and FIs need to escalate its security platform, trade database, correspondence banking, block chain-based solutions, greater associations with fintech companies and access to FCI network to provide cutting edge, cost-effective and hassle-free trade transactions platform for entrepreneurs.

The writer is a financial services professional.

adnaan.jml@gmail.com