Government decision dissolving the National Board of Revenue into tax- policymaking and tax-administration divisions is to improve efficiency, reduce conflicts of interest, and widen tax base, the CA Office says.

The explanation came Tuesday from the office of the head of interim government as a section of NBR staff took it amiss and went on a pen-down protest against the much-discussed measure.

The post-uprising government has announced the major structural reform that effected dissolution of the National Board of Revenue (NBR) to be replaced by two distinct entities under the Ministry of Finance-Revenue Policy Division and Revenue Management Division.

A group of NBR officials swung into protest against the move as soon as the announcement came to light.

"Established over fifty years ago, the NBR has consistently failed to meet its revenue targets. Bangladesh's tax-to-GDP ratio is approximately 7.4 per cent, one of the lowest in Asia. For context, the global average is 16.6 per cent, while Malaysia's stands at 11.6 per cent. To achieve the development aspirations of its people, Bangladesh must raise its tax-to-GDP ratio to at least 10," says the CA office in the statement to substantiate the recast.

Restructuring the NBR is critical to this goal, said a spokesman, adding that there is growing consensus that a single institution should not be responsible for both creating tax policy and enforcing it-such an arrangement breeds "conflicts of interest and promotes inefficiencies".

For years, businesses in Bangladesh have complained that policies have often prioritized revenue collection over fairness, growth, and long-term planning.

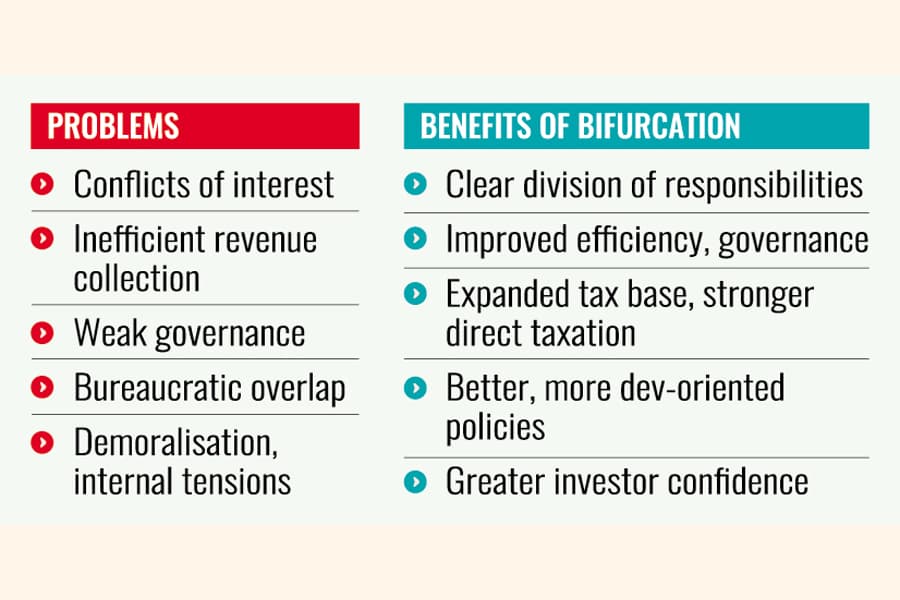

Saying that several longstanding issues have plagued the revenue board, the CA Office cites 10 reasons why it is done.

Conflicts of interest: Housing both policy-making and enforcement under one roof has led to compromised tax policies and widespread irregularities. Under the current system, officials responsible for tax collection are not subject to any accountability framework and are often able to negotiate payments from tax defaulters compromising public interest. In many cases, tax collectors are reluctant to take action against tax-evaders and assist them in doing so for personal interest.

There is no system and process in place for objectively measure the performance of tax collectors and their career progression has not been linked with measurable performance indicators.

Inefficient revenue collection: The dual mandate diluted focus on both policy formulation and institutional capacity-building. As a result, the tax net remains narrow, and revenue collection has lagged far behind potential.

Weak governance: The NBR has suffered from inconsistent enforcement, poor investment facilitation, and systemic governance issues, all of which have eroded investor confidence and weakened the rule of law.

Bureaucratic Overlap: The existing structure-where the head of Internal Resources Division also leads the NBR-has created confusion and inefficiency, hampering effective tax-policy design and delivery.

Demoralisation and internal tensions: The reform process has triggered anxiety among seasoned tax and customs officers, some of whom feel they may be sidelined or overlooked.

How the restructuring to help: The new structure is designed to address these chronic problems through a clearer, more accountable framework.

Clear division of responsibilities: The Revenue Policy Division will be responsible for drafting tax laws, setting rates, and managing international tax treaties. The Revenue Management Division will oversee enforcement, audits, and compliance. This separation ensures that the officials setting tax obligations are not the same as those collecting them, eliminating opportunities for any sort of connivance.

Improved efficiency and governance: By allowing each division to focus on its core mandate, the reform will enhance specialisation, reduce conflicts of interest, and improve institutional integrity.

Expanded tax base and stronger direct taxation: The reform is expected to broaden the tax net, reduce dependence on indirect taxation, and strengthen direct tax collection by placing skilled professionals in appropriate roles.

Better, more development-oriented policies: A dedicated policy unit can craft evidence-based, forward-looking tax strategies instead of reactive policies driven solely by short-term revenue goals.

Greater investor confidence: Transparent, predictable policies and a professional tax administration are expected to attract investment and reduce complaints from the private sector.

Ultimately, the government clarification concludes, this restructuring is not just a bureaucratic reshuffle-it's a necessary step toward building a fairer, more capable tax system. Strengthened policymaking and cleaner tax administration will be vital for Bangladesh to meet the needs-and realise the hopes-of all its citizens.

mirmostafiz@yahoo.com