Bangladesh on the brink-and beyond

How an economy shaken by unprecedented shocks is finding its footing again

Zaidi Sattar and Ahmed Sadek Yousuf

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Macroeconomic mismanagement that began in mid-2022 with squandering of the country's comfortable foreign exchange reserves lasted until the ouster of the autocratic regime. The Monsoon Revolution of August 2024, partly triggered by the economic malaise, dealt the next major blow to the economy. What was a political upheaval nearly upended the economy's growth trajectory dealing a major blow to the banking and financial sector. What happened could only be described as plunder of the banking system by the cronies of the old regime as they carted off billions of dollars worth of cash from the banks much of which, as we now know, was laundered to foreign shores. The magnitude of the plunder - with complicity of the powers that be -- was so massive that calling it a bank heist would be a gross understatement.

It was nothing short of a banking sector Armageddon. This kind of shock to the banking sector is unprecedented in world history and some 15 commercial banks are still reeling from the onslaught. Five smaller Shariah-based banks were left with over 90per cent of their loans non-performing (siphoned off by one particular group) while the largest and the best bank of the country, Islami Bank, was left with one-half of its loans as non-performing. All these banks were left insolvent and illiquid, except for the Islami Bank, which is recovering fast thanks to its receiving large inflows of migrant remittances that generated substantial liquidity for regular operations.

All these unprecedented shocks required unprecedented and bold moves to stem the rot in the banking and financial sector. Thankfully, the hemorrhage has been halted by the swift and bold moves by the Bangladesh Bank at a time when the central bank was besieged by multifarious financial sector anomalies running riot. The fact that a measure of confidence and stability in the banking system has been restored speaks volumes about the effectiveness of several restructuring transformations that were initiated with many more in the offing. The banking sector, however, is still not out of the woods.

The net outcome so far is a semblance of macroeconomic stability, however fragile that might seem. In so far as external balance is concerned, the situation is in stark contrast to the deeply worsening trends that were witnessed since the supply chain shock of 2022. The economy was dealt an exchange rate shock of 30 per cent in a year when BB failed to shore up the exchange rate at Tk.86/US$ while forex reserves depleted by over $10 billion in one year (FY2023-24).

All that had been a history of extreme macroeconomic mismanagement at the national level. As of now, trade and current account balances are very much at sustainable levels (CAD under 1per cent of GDP) with the much-blemished financial account (including capital account) in significant positive territory ($1.5 billion in FY2025). The overall BOP balance in FY2025 showed a decent positive figure of $3.4 billion fostering enhancement in foreign exchange reserves (further bolstered by BB buying of USD from the market, in contrast to the past practice of selling USD to shore up the exchange rate).

One little acknowledged policy measure was the adherence to flexibility in the exchange rate with minimal intervention from the central bank. Yet, there is every indication that exchange rate flexibility has been a pivotal instrument in restoring and maintaining balance of payments stability and fostering forex reserve accumulation. This critical policy swing in exchange rate management (grounded in sound trade economic principles) needs to be understood and put firmly in BB policy dictum for the future. Indeed, adoption of a flexible exchange rate regime (towards free float) by BB should be ingrained in the policy tool as a long-term strategy for stability of forex reserves and overall balance of payments.

Headline inflation, still high by historical standards for Bangladesh, continues to remain sticky at 8.36per cent as of September 2025. Though general inflation is down from 14per cent in late 2023, inflation control via tight monetary policy and high policy interest rate has not had the disinflationary impact as rapidly as expected. Nevertheless, BB is expected to stay the course until inflationary expectations are also tamed sufficiently. One is reminded of the Volcker approach (Paul Volcker, Chairman of US Federal Reserve lifted interest rates to over 20per cent in the early 1980s to thrash inflation) which took some 3-4 years to bring inflation down to 2per cent in the USA, a level that lasted until the Covid crisis of 2021). One could argue that due to weak monetary transmission mechanism in Bangladesh the disinflationary impact of high interest and tight monetary policy might also be a long-drawn-out affair. The only problem here is whether public patience will hold for that much longer while the poor and marginal population endures more suffering.

Meanwhile, the poverty problem continues to haunt us big time. The most recent poverty and inequality assessment by the World Bank ("Bangladesh Poverty and Equity Assessment: Navigating the Road to Prosperity", 25 November, 2025) has revealed that, though 25 million people were lifted out of poverty during 2010-2022, as many as 62 million (nearly a third of the population) are still in the vulnerable group, i.e. likely to fall under poverty from the onslaught of any shock - economic or political. Which leads the World Bank to project that poverty rate has likely risen by some 2-3 percentage point in 2025 compared to 18.7per cent estimated in 2022.

More disturbing is the finding that the inclusivity of Bangladesh's economic growth (i.e. its job creating potential) has been diminishing, particularly over the past decade. It is therefore crucial that Bangladesh redirect policy towards more job-creating growth. While agriculture may be employing 45per cent of the labor force now, that is not where future job creating potential lies. It is and will remain in our labor-intensive industrialization at least for the next decade along with the growing formal services sector. Export orientation of manufacturing and services, in addition to linking urban and rural enterprises with the global marketplace will be the next strategic policy challenge to be addressed with grit and determination for a more inclusive growth performance in the future.

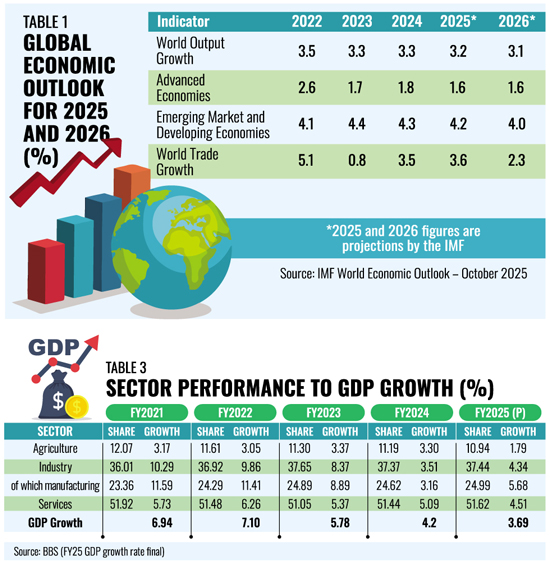

UNCERTAINTY IN GLOBAL TRADE AND INVESTMENT OUTLOOK: The global economic landscape in 2025 has been shaped by forces that extend beyond traditional macroeconomic cycles. The world economy is entering a new phase characterized by moderate growth, enduring policy uncertainty, and deepening geopolitical divisions. These developments are intensifying global fragmentation and creating complex challenges for economies such as Bangladesh, which remain closely linked to international trade and financial systems.

UNCERTAINTY IN GLOBAL TRADE AND INVESTMENT OUTLOOK: The global economic landscape in 2025 has been shaped by forces that extend beyond traditional macroeconomic cycles. The world economy is entering a new phase characterized by moderate growth, enduring policy uncertainty, and deepening geopolitical divisions. These developments are intensifying global fragmentation and creating complex challenges for economies such as Bangladesh, which remain closely linked to international trade and financial systems.

Global growth is settling into a modest rhythm, with world output projected to expand by 3.2 per cent in 2025, nearly matching the pace of 2024. Beneath this apparent stability lies persistent vulnerabilities: investment in advanced economies remains sluggish, productivity gains are stagnant, and medium-term global demand has softened. These weaknesses are further compounded by the spread of protectionist policies, which are reshaping production networks and eroding the traditional benefits of global integration.

A central force behind this growing fragmentation is the shift in US trade policy under the newly introduced Reciprocal Tariff Regime announced by President Donald Trump. By mirroring the tariffs imposed by its trading partners, the United States has raised effective tariff rates, particularly against economies with higher import duties. Combined with Washington's focus on strategic autonomy, reshoring, and stricter oversight of strategic competitors, this policy introduces a new layer of uncertainty into global trade. For emerging markets, the implications are mixed-some may benefit from trade diversion, while others face losses stemming from weaker US demand.

Over the past year, industrial subsidies, investment screening measures, and technology restrictions have expanded across major economies. At the same time, development assistance has declined for a second consecutive year, external financing conditions have tightened, and stricter immigration policies in advanced economies are constraining labor supply. Collectively, these developments are steering the global economy toward a more inward-looking and volatile path.

Over the past year, industrial subsidies, investment screening measures, and technology restrictions have expanded across major economies. At the same time, development assistance has declined for a second consecutive year, external financing conditions have tightened, and stricter immigration policies in advanced economies are constraining labor supply. Collectively, these developments are steering the global economy toward a more inward-looking and volatile path.

Even so, the WEO identifies elements of cautious optimism. The global inflation cycle has clearly turned: after the sharp increases of 2022-23, headline inflation is projected to fall to 4.2 per cent in 2025, supported by monetary tightening and easing supply pressures. Major central banks have begun lowering policy rates, which should help stabilize capital flow and reduce exchange-rate volatility for emerging markets. For Bangladesh, this trend may ease imported inflation pressures and provide some relief to external balances.

Global trade is also expected to recover gradually. Trade volumes are expected to grow by 3.6 per cent in 2025, reflecting firmer demand in parts of Asia and improved supply-chain conditions. While modest, this recovery is a welcome contrast to the disruptions of recent years. Regrettably, the forecast for 2026 is not encouraging for global trade expansion as trade growth (2.3per cent) is projected to be lower than output growth (3.1per cent). However, the extent to which Bangladesh can benefit will depend partly on how the US reciprocal tariff regime affects demand in its single largest export market.

The broader global policy environment remains uncertain. If US tariffs focus predominantly on China, Bangladesh could see opportunities through production relocation. But a more sweeping protectionist stance could dampen global demand, disrupt supply chains, and complicate export prospects. Policymakers will need to monitor these developments closely as the Trump administration's priorities become clearer.

Against this backdrop, FY25 stands as a critical juncture for Bangladesh. The country's recent experience has shown how closely its economic fortunes are tied to global trends through exports, remittances, and external financing. Navigating slow global growth, rising fragmentation, and shifting geopolitical priorities will require strategic positioning. The resilience of Bangladesh's recovery will depend on its ability to adapt domestic policies, strengthen macroeconomic stability, and implement reforms essential for sustaining long-term growth.

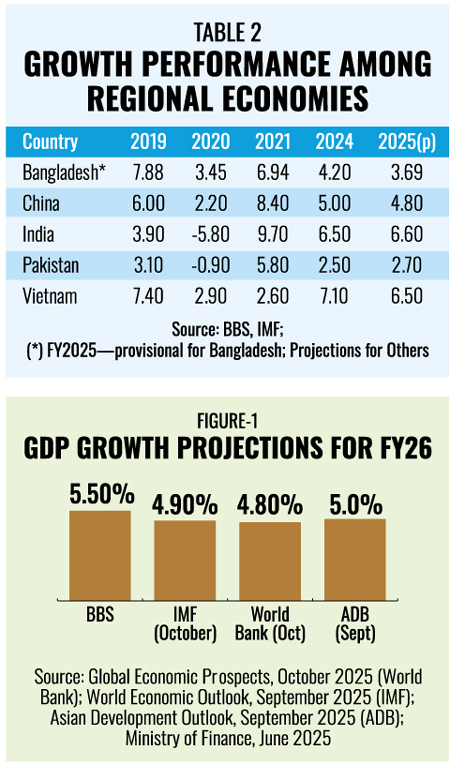

GROWTH PERFORMANCE: From free-fall to low gear. Bangladesh's economic recovery appears to be gradually taking hold, even as overall growth remains subdued. Recent improvements in exports, imports, remittance inflows, and a moderation in inflation have helped strengthen foreign-exchange reserves and enhance macroeconomic stability - internal and external -- signalling that the foundations of recovery have been laid for impending growth spurt.

Bangladesh's free-fall is over, but the economy has not yet found a new, confident stride. The balance-of-payments and foreign exchange reserves scare have eased, inflation is edging down, and high-frequency indicators show some signs of life. Yet the headline numbers in Table 2 tell a sobering story: growth has downshifted sharply, and there is no quick return to the earlier 7-8 per cent path in sight.

Before Covid, Bangladesh was expanding at a rapid until 2019. The pandemic cut growth to 3.45 per cent in 2020, but the rebound was strong: output jumped back to 6.94 per cent in 2021 and 7.10 per cent in 2022 as exports, remittances and domestic demand recovered. Since then, the growth engine has steadily lost steam. Growth slipped to 5.78 per cent in 2023, then to 4.20 per cent in 2024, and the latest BBS estimate puts FY2025 growth at just 3.69 per cent. In six years, Bangladesh has moved from being an above- average- growth economy to one growing below 4 per cent.

The regional comparison underlines the point. India is again growing above 6 per cent, Vietnam above 6 per cent, and even China-despite its own structural problems-remains around 5 per cent. Bangladesh now sits in the middle of the South Asian pack: doing better than countries with chronic instability, but no longer the standout performer it once was.

What FY26 forecasts say

Figure 1 looks ahead by lining up the main forecasts for FY2026 from international agencies and the national authorities. All of them expect some improvement from the FY2025 trough, but the rebound they foresee is modest. The projections cluster in the mid-single digits, with the official forecast at the upper end. The consensus is that growth will pick up from below 4 per cent to something closer to 5 per cent, but not return quickly to over 6 per cent before 2027. Unless reforms lift productivity and investment, slow growth would likely become the new normal rather than a temporary dip.

All engines running below capacity

Beneath the aggregate figures sits a broad-based slowdown across sectors. Agriculture's share in GDP has continued to drift down-from about 12 per cent in FY2021 to just over 11 per cent in FY2024, and likely below that in FY2025-while real growth in the sector has eased from a little above 3 per cent to under 2 per cent (Table 3). Higher input costs, limited access to affordable credit and energy interruptions have held back productivity gains, even though major weather shocks have been relatively contained.

Industry tells a similar, slightly more complicated story. After double-digit growth in FY2021 and robust performance in FY2022-23, industrial growth slowed sharply. Manufacturing-still the backbone of export earnings-dropped from high single-digit growth to just over 3 percent in FY2024 before recovering to around 5-6 per cent in FY2025 (Table 3). Recent high-frequency data suggest an uneven upturn. The Purchasing Managers' Index rose to about 62 in October 2025, comfortably above the 50-point threshold and signalling a faster expansion in both manufacturing and services. At the same time, the Index of Industrial Production shows that overall industrial output in August FY2026 was about 8 per cent higher than a year earlier, driven mainly by a surge in electricity generation. Mining contracted by roughly 15 per cent year-on-year and manufacturing fell on a month-to-month basis, reminding us that the recovery is fragile and patchy, not broad-based and secure.

Services sector, which now accounts for more than half of GDP, has also cooled. Growth in services has slipped from above 6 per cent in FY2021-22 to around 4½-5 per cent in FY2025 (Table 3), reflecting slower construction, weaker trade and transport activity, and more cautious spending by households and firms. There is no single "problem child" sector dragging everyone else down; the whole machine is running below capacity.

Investment: the missing driver

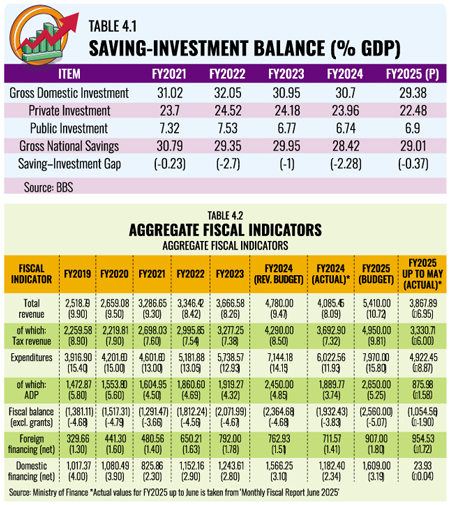

Behind this loss of momentum lies a straightforward investment story. Bangladesh growth performance is still investment driven. Table 4.1 shows that gross domestic investment peaked a little above 32 per cent of GDP in FY2022 and has since fallen back to around 29-30 per cent, with most of the decline coming from the private side. Private investment has slipped from roughly 24½ per cent of GDP in FY2022 to about 22½ percent in FY2025, while public investment has hovered near 7 per cent. This confirms what businesses have been saying for some time: firms are delaying new projects, scaling back expansion plans and waiting for clearer signals on policy, energy and the banking system.

Behind this loss of momentum lies a straightforward investment story. Bangladesh growth performance is still investment driven. Table 4.1 shows that gross domestic investment peaked a little above 32 per cent of GDP in FY2022 and has since fallen back to around 29-30 per cent, with most of the decline coming from the private side. Private investment has slipped from roughly 24½ per cent of GDP in FY2022 to about 22½ percent in FY2025, while public investment has hovered near 7 per cent. This confirms what businesses have been saying for some time: firms are delaying new projects, scaling back expansion plans and waiting for clearer signals on policy, energy and the banking system.

Private-sector credit growth is stuck around 6 per cent, less than half the pace seen in the 2010s, and imports of capital machinery were about 20 per cent lower in FY2025, with only a tentative improvement so far in FY2026. These are not numbers one would expect in an economy preparing for another investment-led growth spurt. They are the hallmarks of caution: banks reluctant to lend, investors wary of taking risks, and a corporate sector more focused on survival than expansion. Also to be acknowledged, machinery import figures of the recent past included copious amounts of over-invoicing with intent to launder money abroad. This contention is presumptive, based on circumstantial evidence, rather than proven by rigorous research (which is essential for future policy guidance).

On the public side, the government has kept overall investment ratios up only by budgeting ambitiously. Overall spending has been far below the target. ADP implementation fell to about 68 per cent in FY2025, the weakest outcome in two decades. That means projects are being approved faster than they can be financed and executed, and that much-needed infrastructure and social spending is being postponed just when it is most needed to crowd in private investment and support jobs.

Jobs, poverty and social stress

The social consequences of this low-growth, low-investment equilibrium are already visible. The latest poverty and labour-market assessments suggest that nearly 2 million additional people fell below the poverty line in 2024, with a further ½-1 million at risk in 2025. High and persistent inflation has eroded real incomes, especially for low-income urban households and the near-poor. At the same time, slower growth and weak investment have reduced the pace of job creation and pushed more workers into informal, low-paid activities. Rising inequality indicators suggest that the gains from earlier growth episodes are no longer being widely shared.

Seen through this lens, the current situation is best described as a stalled recovery. The emergency phase-marked by a sliding currency, rapidly rising inflation and fear of a full-blown balance-of-payments crisis-has been brought under control. But the country has not yet moved on to a healthier, more dynamic phase. Instead, it risks getting stuck in a zone where stabilisation is achieved by cutting back investment and squeezing living standards, rather than by lifting productivity and expanding opportunities.

Policy implications and LDC graduation

The big risk now is that Bangladesh gets used to this lower gear. Growth of 3½-4½ per cent is enough to avoid crisis, but not enough to create the jobs and income gains that people have come to expect. With private investment sliding and public projects delayed, it would appear that the country is slowly adjusting to weaker short-term prospects rather than pushing to restore its earlier momentum. The hope is all this could change for the better with forthcoming elections and a change of government that ushers in political stability.

This is happening just as Bangladesh approaches a once-in-a-generation milestone: graduation from LDC status in 2026, with most trade preferences likely to fade out by the end of the decade. Graduation will rightly be celebrated as a success story, but it also raises the bar. Exporters will face higher tariffs and tougher competition at a time when many firms are already cautious, profit margins are thin and access to reliable finance and energy is uneven. Entering the post-LDC world with slow growth and hesitant investment would make it harder to hold on to markets, let alone move up the value chain. Given that the economy and society suffered major internal and external shocks over the past 2-3 years - shocks that jolted past economic momentum to a low investment-low growth current and prospective scenario -- there is justification for seeking deferment of the graduation timetable.

The policy task in the growth space is therefore clear. Over the next few years Bangladesh needs to rebuild confidence so that firms feel safe to invest again, use its limited public resources to unlock private activity instead of spreading them thinly, and protect vulnerable households so that the adjustment does not permanently damage human capital. It has to move up the value chain in garments and other sectors, modernise customs and standards, and build a more capable state that can negotiate and defend market access. Otherwise, the country risks entering the post-LDC world as a developing country with its growth performance remaining stalled.

From a growth perspective, the message is simple: the emergency phase is over, but the hard work has only just begun. Unless these reforms are pushed through with an eye on LDC graduation, the economy could settle into a long stretch of "just-okay" growth that falls short of what the next phase of development demands.

Nevertheless, having attained macroeconomic stability, the foundation has thus been set up for higher growth once the election phase is over and a new political government takes charge.

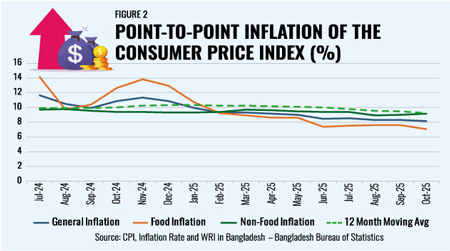

MONETARY POLICY AND BANKING SECTOR DEVELOPMENTS: Inflation and monetary management. If the growth story is one of a hard landing into a lower gear, inflation is the reminder that the shocks of the past two years have not fully faded. Headline CPI ran close to double digits through FY2023-24 and into early FY2024-25, after fuel and power price hikes, a large exchange-rate adjustment and weather-related food shocks hit in quick succession. Point-to-point inflation was still above 11 percent in late 2024, with food prices in the mid-teens and non-food inflation also high (Figure 2).

Since then, the picture has improved but not yet normalised. By June 2025, inflation had slipped below 9 percent, and by October 2025 it stood at about 8.2 per cent, the lowest reading in more than three years. Food inflation has eased to just over 7 per cent, but non-food inflation has climbed back above 9 per cent, showing that cost pressures in housing, transport and services remain entrenched. The 12-month average is still around 9 per cent, well above Bangladesh's medium-term comfort zone. Since late FY24, the central bank has pivoted towards more orthodox monetary policy. It has raised the policy rate, scrapped the 6-9 per cent interest-rate band, moved lending rates onto a T-bill-anchored SMART system, allowed more exchange-rate flexibility and cut back on direct budget financing. Lending rates are now in the low- to mid-teens and money growth has slowed. In its Monetary Policy Statement for the first half of FY26, Bangladesh Bank kept the repo at 10 per cent and lowered the private-credit growth target to about 7.2 per cent - a clear signal that it is willing to trade some growth for a quicker fall in inflation. The drop in inflation from nearly 12 per cent to around 8½ per cent shows that this tougher stance has started to bite. But the adjustment has been abrupt and uneven. Interest-sensitive activities and smaller firms have borne the brunt, while weaknesses in the banking system have blunted the effect of higher policy rates.

Since then, the picture has improved but not yet normalised. By June 2025, inflation had slipped below 9 percent, and by October 2025 it stood at about 8.2 per cent, the lowest reading in more than three years. Food inflation has eased to just over 7 per cent, but non-food inflation has climbed back above 9 per cent, showing that cost pressures in housing, transport and services remain entrenched. The 12-month average is still around 9 per cent, well above Bangladesh's medium-term comfort zone. Since late FY24, the central bank has pivoted towards more orthodox monetary policy. It has raised the policy rate, scrapped the 6-9 per cent interest-rate band, moved lending rates onto a T-bill-anchored SMART system, allowed more exchange-rate flexibility and cut back on direct budget financing. Lending rates are now in the low- to mid-teens and money growth has slowed. In its Monetary Policy Statement for the first half of FY26, Bangladesh Bank kept the repo at 10 per cent and lowered the private-credit growth target to about 7.2 per cent - a clear signal that it is willing to trade some growth for a quicker fall in inflation. The drop in inflation from nearly 12 per cent to around 8½ per cent shows that this tougher stance has started to bite. But the adjustment has been abrupt and uneven. Interest-sensitive activities and smaller firms have borne the brunt, while weaknesses in the banking system have blunted the effect of higher policy rates.

This disinflation has not happened by accident. Since late FY2023-24, Bangladesh Bank has abandoned the era of capped lending rates and a near-fixed exchange rate and moved towards more orthodox monetary management. The policy (repo) rate has been raised in stages to 10 per cent, where it has been held through successive Monetary Policy Statements, even as inflation has drifted down. The old 6-9 per cent interest-rate band has been scrapped; lending rates are now set under the SMART framework, linked to T-bill yields; and the exchange rate has been allowed more flexibility, with the central bank buying rather than selling dollars to rebuild reserves.

The result is that for the first time in years, the policy rate is meaningfully positive in real terms: nominal 10 percent against point-to-point inflation just above 8. This is a sharp contrast with the period when real rates were deeply negative and monetary policy was effectively accommodating the inflation shock. But the adjustment has been abrupt and uneven. Large, well-connected borrowers have found ways to live with higher rates or shift into safer assets, while smaller firms and new entrants face a much tougher credit environment.

Looking ahead, the central question is not whether the repo rate should be nudged up or down by 50 basis points in the next review. It is whether Bangladesh can stay the course long enough to bring inflation back towards the 5-6 percent range without triggering a political backlash or a collapse in credit to viable firms. That, in turn, depends on the health of the banking system.

Credit conditions and private-sector financing

Tighter money has landed on a banking system that was already weakened. Private-sector credit growth has slid to historic lows: by September 2025, it was only 6.3 per cent year-on-year, well below the central bank's own target of about 7.2 per cent for the first half of FY2025-26. This is a long way from the double-digit credit growth that supported the earlier high-growth years.

The slowdown is not only about high interest rates. Banks are now far more cautious in taking risk. After years of forbearance, audits and stricter supervision have forced many institutions to recognise loans that should have been classified as non-performing long ago. Provisioning costs have risen, capital buffers have been eroded, and boards are under pressure. In that environment, it is easier and safer for banks to load up on government paper than to extend fresh credit to small and medium-sized firms, exporters or new projects.

At the same time, deposit growth is hovering close to 10 per cent, suggesting that savers are gradually returning to the formal system, even though deposit rates still trail inflation for many households. Public-sector borrowing is rising much faster than private credit-government credit growth has jumped above 20 per cent-so scarce bank liquidity is being pulled into financing the budget.

From a narrow stabilisation perspective, this pattern helps: weaker private credit reduces pressure on imports, takes some heat out of domestic demand and gives the central bank extra room to defend the currency. But from a growth and jobs perspective, it is troubling. The firms that are being rationed out of credit are often the ones that generate employment and exports. If this configuration persists-slow private credit, fast public borrowing and a large share of bank assets tied up in government securities-it risks locking the economy into exactly the kind of low-growth, low-investment equilibrium that the country can least afford.

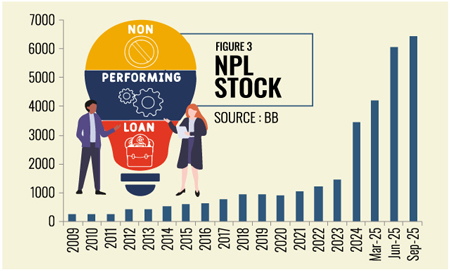

Before closing, it needs to be acknowledged that part of the credit volume and growth in the recent past included superfluous lending - the consequence of a highly skewed lending approach of the banking system where 1per cent of borrowers got 75per cent of all the loans (PRI research from nationwide banking data). So, if credit growth from a bruised banking sector is down should not be surprising to anyone. Another consequence of past recklessness, NPLs are reaching skywards (Figure 3), mainly due to the profligacies of the previous regime.

Before closing, it needs to be acknowledged that part of the credit volume and growth in the recent past included superfluous lending - the consequence of a highly skewed lending approach of the banking system where 1per cent of borrowers got 75per cent of all the loans (PRI research from nationwide banking data). So, if credit growth from a bruised banking sector is down should not be surprising to anyone. Another consequence of past recklessness, NPLs are reaching skywards (Figure 3), mainly due to the profligacies of the previous regime.

Banking sector vulnerabilities and NPL dynamics

The numbers on non-performing loans show how deep the problem runs. Official data indicate that the stock of classified loans surged from around Tk 2.1 trillion in mid-2024 to over Tk 5.3 trillion-more than a quarter of outstanding loans-by June 2025 (Figure 3). By September 2025, once newly recognised bad loans and overdue exposures were added, non-performing loans reached roughly Tk 6.4 trillion, or 35.7 per cent of total credit, the highest ratio in a quarter of a century. When rescheduled, restructured and written-off loans are taken into account, total "distressed assets" are estimated at around Tk 9½ trillion-roughly half of the banking system's loan book.

These bad loans are heavily concentrated in a handful of weak private banks and several state-owned commercial banks. In some institutions, the effective NPL ratio is so high that capital has been virtually wiped out, leaving them dependent on regulatory forbearance and public support to stay afloat. Five financially troubled Islamic banks are already in various stages of merger, with combined bad-loan exposures of about Tk 1.4 trillion, and at least nine non-bank financial institutions are being liquidated.

In practical terms, a banking system this clogged with bad assets cannot transmit monetary policy in a predictable way. When the central bank raises rates, fragile banks do not respond by pricing risk and lending more carefully; they respond by cutting back lending altogether and parking funds in government securities. When rates eventually fall, the same banks may still refuse to lend because they are busy repairing their balance sheets or because they fear another wave of defaults. In both directions, the link from the policy rate to credit conditions is muffled: the central bank moves, but the real economy feels only part of the signal.

This is why the current situation is best described as a banking crisis intertwined with a growth slowdown, rather than a simple case of temporary liquidity stress. Without a decisive clean-up of NPLs and a credible plan for recapitalising or resolving weak institutions, neither monetary easing nor fiscal stimulus will deliver the growth response that policymakers hope for.

Reform priorities and the role of central bank independence

The good news is that the policy debate has shifted. Since mid-2024, the authorities have accepted-at least on paper-that incremental tweaks are not enough. Under the IMF-supported reform programme and domestic pressure for change, a broad roadmap is emerging.

On the legal side, a package of new laws and amendments is being prepared or rolled out: a modern Bank Resolution Ordinance to give Bangladesh Bank clear powers to intervene in failing banks; changes to the Bank Company Act to tighten fit-and-proper criteria for directors and major shareholders; a Distressed Asset Management Act to license professionally run asset-management companies; and reforms to the deposit-insurance scheme to raise coverage and allow the fund to co-finance resolutions.

Supervisory practice is also being upgraded. Asset-quality reviews are under way for a large share of private banks, risk-based supervision is being phased in, and the central bank has moved to replace boards and senior management in some of the most problematic institutions. Five weak Islamic banks are being merged, and insolvent NBFIs (Non-bank financial institutions) are being wound up rather than kept alive indefinitely.

Perhaps the most politically sensitive reform is the proposed Central Bank Independence Ordinance, which would strengthen Bangladesh Bank's operational autonomy and help insulate monetary and supervisory decisions from day-to-day political pressure.

If passed and implemented in spirit, this could help break the pattern in which rate hikes, exchange-rate adjustments and tough enforcement actions are postponed until crises force them onto the agenda.

But laws and roadmaps are only as good as their execution. Three practical tests will determine whether the current clean-up really changes behaviour:

1. One rulebook for all banks. State-owned and private banks need to face the same classification standards, capital requirements and enforcement actions. A dual system guarantees arbitrage and keeps NPLs high.

2. Time-bound resolution of weak institutions. Chronic defaulters and non-viable banks cannot be allowed to hold the system hostage indefinitely. Asset-management companies must be given the tools and incentives to work out bad loans quickly, not simply warehouse

3. Transparent communication. The central bank has to explain not just what it is doing but why-linking its interest-rate decisions, supervision actions and bank-resolution steps to a clear narrative about inflation, growth and financial stability.

If these reforms gain traction, high NPLs will gradually be written down, recapitalised or recovered, and monetary policy will regain much of its bite. If they stall, Bangladesh risks living with a permanently weakened banking system: one that survives behind regulatory shields but cannot provide the long-term finance needed for growth, export diversification and job creation. In that world, inflation may eventually come down, but the economy would remain stuck in a low-growth, low-investment equilibrium, with rising frustration among households and firms who may feel that the rules only bite when they are on the wrong side of the counter.

FISCAL MANAGEMENT AND DEBT DYNAMICS

Fiscal stance in FY24-25. With monetary policy already tight, Bangladesh has been trying to steady the economy with a cautious budget rather than shock therapy. On the surface, the headline numbers look reassuring. In FY2024, total revenue came in at about Tk 4.1 trillion, a little over 8 per cent of GDP, against a revised target close to 9½ per cent of GDP. Total spending reached roughly Tk 6.0 trillion, or about 11.9 per cent of GDP, well below the revised budget envelope. The net result was a deficit of about 3.8 per cent of GDP-smaller than planned and comfortably within the range Bangladesh has lived with for years (Table 4.2 on page 4).

FY2024-25 has followed a similar pattern. The Finance Division now puts the full-year deficit at about 4.1 per cent of GDP, lower than the 4.6 per cent originally budgeted, confirming that the government has chosen to hold the gap down rather than let borrowing run. The FY2025-26 budget, in turn, aims to reduce the deficit further to around 3.6 per cent of GDP, extending this gradual consolidation into the next year.

This restraint has helped stabilise the macro picture. Lower-than-planned deficits relieve pressure on domestic borrowing, support the fight against inflation and reduce the risk of a sudden loss of confidence. But the way this has been achieved matters. The deficit has not been squeezed by a surge in tax effort; it has been contained mainly by holding back spending, especially on development projects. In plain language, the state is doing less than it promised, because it cannot safely finance more. That may be understandable in a period of stress, but it also shows how narrow Bangladesh's fiscal "comfort zone" has become.

Revenue mobilization and composition of spending

The structural weak point is revenue. For more than a decade, total revenue has hovered in the 8-10 per cent of GDP range, with tax revenue usually between about 7 and 9½ per cent. Recent data point to a softening rather than an improvement: the tax-to-GDP ratio has slipped toward roughly 6½ percent, even as nominal collections have risen and the economy has grown.

Early FY26 numbers underline the problem. Between July and October, overall revenue grew by a strong double-digit rate compared to a weak base a year earlier, but the momentum faded quickly-growth in October dropped to just over 2 per cent year-on-year. Beneath the surface, the pattern is uneven: value-added tax and direct taxes have been growing by around 10 per cent, while customs revenue has contracted sharply, by about 16 per cent. This mix confirms what practitioners have long known: Bangladesh still leans heavily on taxes at the border and on consumption, while income and property remain lightly taxed.

On the spending side, pressures are building even inside a tight envelope. Interest payments are rising as domestic debt is rolled over at higher rates and the weaker taka raises the cost of servicing foreign loans. Subsidies-especially on energy and fertiliser-remain sizeable despite repeated price adjustments. Put together with wages, pensions and transfers, these items absorb most of the modest revenue base. The more space they take up, the less room is left for infrastructure, health, education and climate-related investment.

The government has rightly signalled that it wants to lift the tax-to-GDP ratio into double digits over time and has launched a major institutional shake-up by dissolving the old revenue board and splitting policy and administration functions under the finance ministry. Whether this experiment succeeds will be judged not by organisational charts but by outcomes: a broader base, fewer exemptions and para-tariffs, better VAT and income-tax compliance, and modernised systems that make it harder to evade and easier to pay. Without that kind of shift, "fiscal discipline" will continue to mean stop-start spending cuts rather than a durable capacity to finance development.

The government has rightly signalled that it wants to lift the tax-to-GDP ratio into double digits over time and has launched a major institutional shake-up by dissolving the old revenue board and splitting policy and administration functions under the finance ministry. Whether this experiment succeeds will be judged not by organisational charts but by outcomes: a broader base, fewer exemptions and para-tariffs, better VAT and income-tax compliance, and modernised systems that make it harder to evade and easier to pay. Without that kind of shift, "fiscal discipline" will continue to mean stop-start spending cuts rather than a durable capacity to finance development.

ADP execution and the investment constraint

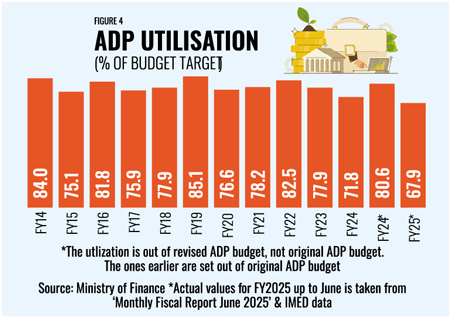

The strain shows up most clearly in the Annual Development Programme (ADP). In FY2024, actual ADP spending was about Tk 1.88 trillion-roughly 3.7 per cent of GDP-against an allocation of Tk 2.54 trillion, or about 4.9 per cent of GDP (Figure 4). Thus, almost Tk 560 billion of planned development spending never happened.

FY2024-25 turned out even weaker. IMED data indicate that ministries and divisions spent only about Tk 1.53 trillion out of a revised ADP of Tk 2.26 trillion, an implementation rate of roughly 68 percent- a record low in the IMED series and far below the usual 80-85 percent seen in earlier years. Early FY2025-26 figures tell a similar story from a different angle. In the first four months of FY26, ADP disbursements amounted to about Tk 199 billion, or 8.33 per cent of the annual programme. That is slightly higher as a share of the smaller FY26 ADP (Tk 2.387 trillion) than in the same period a year earlier, but in absolute terms it is the lowest first-four-month disbursement in eight years.

Thus with total revenue stuck at around 8-9 per cent of GDP and routine obligations and current expenditures eating up most of it, there is very little fiscal space in the budget left to finance ADP. In practice, almost the entire ADP-typically 3½-4 per cent of GDP in a normal year-needs to be financed by borrowing, whether from domestic savers or development partners. A larger ADP therefore means a larger deficit and more debt; holding the deficit down, in turn, means slowing or shrinking the ADP.

Thus with total revenue stuck at around 8-9 per cent of GDP and routine obligations and current expenditures eating up most of it, there is very little fiscal space in the budget left to finance ADP. In practice, almost the entire ADP-typically 3½-4 per cent of GDP in a normal year-needs to be financed by borrowing, whether from domestic savers or development partners. A larger ADP therefore means a larger deficit and more debt; holding the deficit down, in turn, means slowing or shrinking the ADP.

Because the ADP is the main vehicle for roads, power, urban services and other public investments, weak execution has real economic costs. When projects stall, contractors scale back, supply chains thin out, and the private sector faces poorer infrastructure and more uncertainty. Bangladesh is effectively buying short-term macro stability by accepting slower progress on its capital stock. The risk is that this "temporary" adjustment hardens into a new normal of low execution and modest ambition.

A smarter approach would be to treat development spending as something to protect and prioritise, not the easiest line to cut. That means narrowing the ADP to a realistic pipeline of ready projects, speeding up procurement and implementation, and using concessional project loans more aggressively where they clearly raise productivity. The goal should be fewer schemes on paper but more that actually turn into completed bridges, power connections and urban services.

Debt dynamics and medium-term fiscal strategy

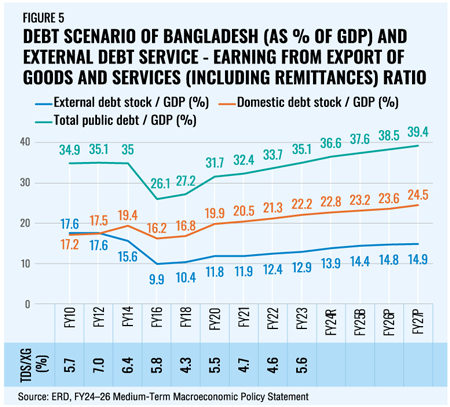

On debt, the picture is mixed. Bangladesh is not yet a high-debt country and historically its total public debt-to-GDP ratio has been within a comfortable range (Figure 5). However, the current direction is worrying. By end-June 2025, total public debt had climbed to about Tk 21.44 trillion, up roughly 13½ per cent in a year. This represents 38.61 per cent of GDP, about 2.3 percentage points higher than a year earlier. Domestic debt reached around Tk 11.95 trillion, while external public debt rose to about Tk 9.49 trillion and now accounts for roughly 44 per cent of the total. Interest payments grew by around 17 per cent year-on-year, with foreign debt service rising by about 21 per cent and domestic interest by 16 per cent.

External debt rose faster than domestic debt (17 per cent versus 11 per cent) and now accounts for 44 per cent of the total, but domestic liabilities still make up the majority of the portfolio. On paper this is still below the IMF's 55 per cent threshold for low-income countries, and the ratio of external debt service to exports and remittances remains in the mid-single digits. The burden shows up somewhere else: the ratio of external public debt service to total foreign-exchange earnings edged up to 6.4 per cent, from just over 6.1 per cent a year earlier-still safely below stress thresholds, but clearly rising. In parallel, interest costs jumped by 17 per cent in a single year, with payments on treasury securities up by over 40 per cent and external interest up by just over 20 per cent.

Every year a slightly larger slice of tax revenue and foreign-exchange earnings is pre-committed to service old loans, leaving a slightly smaller slice for new infrastructure, social spending and climate resilience. If growth and revenue stay weak while this trend continues, debt will still look "moderate" as a share of GDP, but it will feel much heavier in the budget.

The message from these numbers is straightforward. Debt is being used to plug a persistent gap between low, stagnant revenues and rising demands on the budget, while large infrastructure projects continue to face delays and cost overruns. As debt builds up faster than the state's ability to collect taxes, fiscal space shrinks. More of every taka collected goes to interest and repayments, leaving less for schools, hospitals and climate-resilient infrastructure. The risk is not an immediate default, but a slow squeeze in which development spending is crowded out and the quality of growth deteriorates.

The recent decision by the IMF to complete combined reviews of Bangladesh's programme and to augment access, extend the timeline and disburse additional funds has eased short-term external financing pressures and helped unlock more budget support. But this breathing space comes with strings attached: faster progress on revenue reforms, a cleaner and better-governed banking system, and a more credible exchange-rate regime. Concessional programme finance is meant to be a bridge to a stronger fiscal and external position, not a substitute for domestic adjustment.

Looking ahead, a sensible fiscal strategy would rest on three simple principles. First, keep the overall deficit on a path that allows public debt to grow more slowly than the economy, so that investors and citizens see a clear ceiling rather than a moving target. Second, tilt new borrowing toward concessional, long-term finance and away from expensive, short-term domestic instruments that quickly ratchet up interest costs. Third, use the limited borrowing space to back high-return investments-infrastructure, human capital and climate resilience-rather than routine subsidies or recurring losses in state-owned enterprises.

Seen this way, FY2024-25 should be read less as a sign that "all is well" and more as an early warning. Bangladesh has shown that it can avoid a fiscal blow-up by holding the deficit down and squeezing investment. The task now is harder: to rebuild the state's capacity to raise and spend money in a way that supports growth, protects the vulnerable and keeps debt on a responsible path.

EXTERNAL SECTOR DEVELOPMENTS

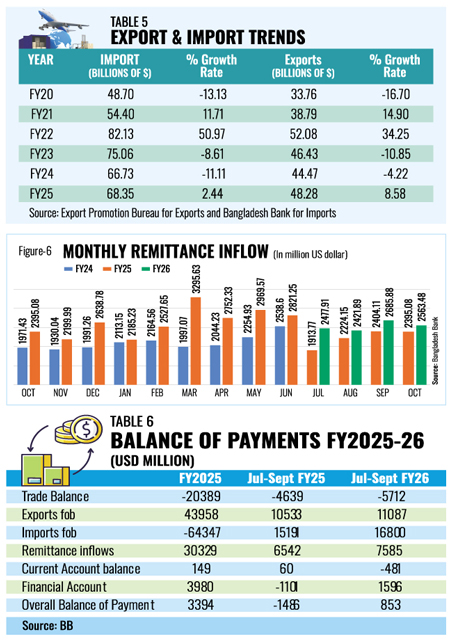

The cost of Bangladesh's current stabilisation strategy also shows up clearly in the external sector. Table 5 shows where it is most visible: in the trade account. In the recent past, Bangladesh balanced its external books more by slamming the brakes on imports than by turbo-charging exports. After the post-Covid surge, exports dipped and have only now crawled back to around US$48 billion in FY25. That is a recovery, but not a transformation.

The cost of Bangladesh's current stabilisation strategy also shows up clearly in the external sector. Table 5 shows where it is most visible: in the trade account. In the recent past, Bangladesh balanced its external books more by slamming the brakes on imports than by turbo-charging exports. After the post-Covid surge, exports dipped and have only now crawled back to around US$48 billion in FY25. That is a recovery, but not a transformation.

The real adjustment has come from the other side of the ledger: import payments have been forced down from their FY22 peak through high LC margins, administrative controls and weaker domestic demand. The smaller trade deficit, in other words, is less a story of new competitiveness and more a story of an economy learning to live with fewer imported inputs.

This mix buys time but carries a price. When we protect reserves by rationing capital goods and raw materials, we also ration growth. Factories delay expansion, ADP projects stall, and the investment slowdown described earlier becomes baked into the external account. On paper, the trade numbers look healthier; on the ground, firms face thinner order books, patchy access to inputs and weaker incentives to move up the value chain.

The policy choice is therefore simple, even if the execution may not be. Bangladesh cannot keep its external balance looking tidy by holding imports underwater forever. A sustainable strategy has to flip the logic: let imports normalize as confidence and reserves rebuild and make the trade balance hinge on earning more rather than importing less, while letting a flexible exchange rate ensure the stability of trade and current account balance. That means pushing beyond a narrow RMG base, locking in more predictable market access, and using exchange-rate, logistics and energy reforms to help exporters compete on productivity instead of on episodic deals and crisis-era rationing.

Be that as it may, the projected trade deficit (in goods and services) for FY2026 is still around $28 billion, which will be adequately compensated by remittance inflows projected to be around $35 billion, if current trends persist. The current account deficit is expected to remain well within the sustainable limit of under 1per cent of GDP.

Be that as it may, the projected trade deficit (in goods and services) for FY2026 is still around $28 billion, which will be adequately compensated by remittance inflows projected to be around $35 billion, if current trends persist. The current account deficit is expected to remain well within the sustainable limit of under 1per cent of GDP.

Remittance inflows reached USD 10.15 billion in July-October FY26, up 14per cent from USD 8.9 billion (Figure 6) in the same period last year, supported by a more stable foreign exchange market, reduced reliance on hundi channels, and a narrower gap between official and informal exchange rates.

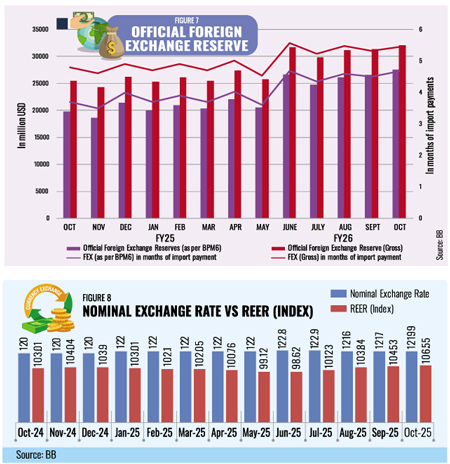

Balance of Payments figures at the end of FY2025 demonstrate the robustness of the restoration of external balances, with BoP posting a decent positive overall balance of $3.3 billion, which contributes to the growth of FE reserves (Figure 7). As of October 2025, official FE reserves stood at $27.5 billion (IMF's BPM6) or $32.1 billion gross reserves (BB).

This continuous robust recovery in our external balances will have to be attributed to, among other measures, the adherence to a flexible exchange rate policy which has stood us in good stead thus far. It would therefore be prudent to continue on this track for the foreseeable future without the proclivity to depart from this policy in the face of temporary developments. One such quirky step was seen when BB sought to prevent appreciation pressure on the exchange rate by buying over $1 billion of foreign exchange from the market. That is tantamount to intervention in the exchange market that violates the principle of exchange rate flexibility. A better option for now would be to loosen up imports further and let the market determine movements in the exchange rate. We can already see some divergence between the nominal exchange rate and REER trends (Figure 8).

The Real Effective Exchange Rate (REER) index, which indicates export competitiveness, showed appreciation of 7per cent since Jun 2025, increasing from 98.1 in May 2025 to 106.55 in October 2025. A REER above 100 signals currency appreciation, which typically erodes export competitiveness and slows remittance inflows, while making imports cheaper. Nominal exchange rate of Bangladesh Taka against USD depreciated by 1.71 per cent y-o-y at the end of October 2025 compared to the end of October 2024 - a favorable trend in light of the fact that our inflation has been consistently above US inflation of around 3 percent during this time.

Economic impact of US reciprocal tariffs

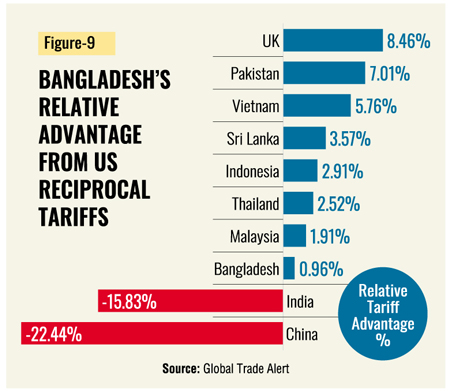

Amidst the macabre political shock of 2024 that dealt a near catastrophic blow to a thriving Bangladesh economy, there came the external trade shock from US reciprocal tariffs. The 2025 U.S. Reciprocal Tariff Policy marks a major realignment in global trade. Under this regime, the United States has adapted a strategy to counter high tariffs imposed by its trading partners, creating a new system of parity in protection that reshapes competitiveness across developed and developing economies. For Bangladesh, the implications are mixed but moderately favorable.

Amidst the macabre political shock of 2024 that dealt a near catastrophic blow to a thriving Bangladesh economy, there came the external trade shock from US reciprocal tariffs. The 2025 U.S. Reciprocal Tariff Policy marks a major realignment in global trade. Under this regime, the United States has adapted a strategy to counter high tariffs imposed by its trading partners, creating a new system of parity in protection that reshapes competitiveness across developed and developing economies. For Bangladesh, the implications are mixed but moderately favorable.

The Relative Tariff Advantage (RTA) shows how much more or less favorably a country is treated under U.S. reciprocal tariffs relative to its competitors (Figure 9). A positive RTA indicates a competitive edge through lower average tariffs, while a negative value signals a relative disadvantage. Vietnam, for example, holds an RTA of +5.76 compared with Bangladesh's +0.96, even though both face a nominal 20 percent reciprocal tariff. The difference arises from their effective rates 21.9 per cent for Vietnam and 35.1 per cent for Bangladesh reflecting differences in export composition and trade exposure. Historically, exports to the United States were driven by Bangladesh's comparative advantage in labor-intensive garment production. In the age of reciprocal tariffs, that advantage is being redefined by the relative gains emerging from tariff structures themselves.

A Computable General Equilibrium (CGE) model based on the GTAP Version 9 database helps quantify these dynamics. Simulation results suggest modest but positive outcomes for Bangladesh: real GDP increases by 0.32 per cent, the terms of trade improve by 0.34 per cent, and welfare measured through Equivalent Variation shows a small net gain. These benefits largely stem from trade diversion as U.S. importers shift purchases away from major suppliers like China and India.

Among export sectors, the textile and apparel industry Bangladesh's mainstay registers an 8.1 percent rise in shipments to the U.S., while leather and footwear exports expand by about 19 percent. These reflect shifts in sourcing decisions driven by cost and tariff realignment. Yet, the scale of these gains remains smaller than those observed in Vietnam and Cambodia, revealing persistent constraints in diversification, port efficiency, and energy supply.

For Bangladesh, this new trading landscape demands renewed policy attention. Competing successfully in a reciprocal tariff world requires strategic positioning through better logistics, diversification (product and geographic), faster trade facilitation, and deeper integration into regional and global supply chains. Policy priorities should focus on improving ports and inland transport links, digitizing customs operations, reducing non-tariff costs, and supporting investment in value-added manufacturing. A coherent export competitiveness strategy anchored in trade diversification, skills development, and infrastructure modernization will determine whether Bangladesh remains a marginal beneficiary or evolves into a leading regional production hub under the emerging tariff order.

Strategic Policy Priorities for Bangladesh

In light of the above, to compete effectively under a reciprocal tariff system, Bangladesh must strengthen trade competitiveness and supply-chain integration. Therefore the key political priorities are:

• Improve port performance and inland transport connectivity

• Accelerate trade facilitation through customs digitization and streamlined procedures.

• Reduce non-tariff costs and logistics bottlenecks.

• Promote export diversification across products and markets.

• Support investment in value-added manufacturing and skill development.

Thus a coherent export strategy-anchored in infrastructure modernization, skills, and integration into regional/global value chains-will determine whether Bangladesh becomes a marginal beneficiary or a competitive regional production hub under the new tariff regime.

CONCLUDING THOUGHTS ON THE STATE OF THE BANGLADESH ECONOMY 2025

As the sun sets on the year 2025 -- another tumultuous year no doubt - how does one assess the state of the economy in light of the multifaceted challenges the economy faced in the past year and what do we see as the prospects going forward. For one, the nation and its policymakers must be prepared to face all challenges head on without being cowed down on account of the internal and external shocks that the economy had to withstand.

This economy has faced political and consequent economic shocks in the past. Each time the economy recovered and went on to become more vibrant and prosperous compared to the past. This time can be no different. The foundational pillars of the economy--- RMG industry, migrant remittances, and a vibrant agriculture sector--- remain intact, to take on challenges for the future. And most important, demography is still in our favor. The fact that two-thirds of the population is reported to be below 35 years of age, with a median age of 27, tells us that the demographic dividend is ours to harness for the future. But challenges are many and complacency could be our worst enemy.

So Bangladesh closes the year 2025, after stemming the rot that transpired within the financial sector and the singular mismanagement of the external sector during FY2023-24, the economy has achieved a state of macroeconomic stability, though still fragile: the balance of payments is robustly stable, reserves are rebuilding, and the exchange rate shock of 2022-24 has been absorbed largely thanks to a decisive shift toward exchange-rate flexibility and tighter monetary policy. Yet this stabilization has come at a high cost-growth is muted with investment still hamstrung as investors, both foreign and domestic, adopt a wait and see approach with elections looming on the horizon.

The prospect that Bangladesh gets "stuck" in a low-growth, low-investment equilibrium must be avoided at all cost through long overdue structural reforms. Going forward, policy must pivot from stabilizing by cutting back to stabilizing by expanding capacity, reviving private investment, easing good-quality imports and aggressively supporting export diversification through energy, logistics and trade policy reforms.

Taming inflation fast remains high priority. It continues to hurt the poor disproportionately. Tight monetary policy and removal of interest-rate caps were necessary and should not be prematurely reversed. The core policy lesson is to institutionalize a more independent, rules-based central bank that can act early on inflation and exchange-rate pressures, rather than delaying adjustment until the eventual cost is much larger. At the same time, any further relative-price and interest-rate adjustments must be paired with more agile and better-targeted social protection to avoid pushing near-poor households back into poverty. Poverty and inequality must also be addressed through inclusive and job-creating growth strategies.

NPL explosion and shock to the banking sector are now recognized as systemic, not marginal. Cleaning up bank balance sheets, enforcing a single rulebook for state-owned and private banks, and operationalizing the new legal tools for resolution and asset recovery are urgent. Until the banking system is recapitalized and governed at arm's length from vested interests, monetary policy will remain blunt and credit to productive firms, especially SMEs and exporters will stay rationed. Banking reform is thus not just a financial-sector agenda; it is central to restoring growth and investment.

The fiscal story is nightmarish for the country with chronic revenue weakness and under-execution of development spending. Deficits look modest only because ADP has been repeatedly cut or delayed; tax revenue remains stuck near 6-7 per cent of GDP, among the lowest in Asia. With debt still moderate but getting more expensive, the clear policy priority is to implement a medium-term revenue strategy in earnest-widening the tax base, reducing exemptions, rationalizing tariffs and para-tariffs, modernizing VAT and income-tax administration-so that higher, more predictable revenues can finance infrastructure, human capital and climate resilience without jeopardizing debt sustainability.

The Way Forward

Bangladesh will enter 2026 after a period of exceptional turbulence-external shocks, a once-in-a-generation political transition, and deep stresses in the banking system. Yet the events of the past two years have also revealed something fundamental: the economy's underlying engines remain remarkably resilient. Exports are recovering, remittances are rising strongly, inflation is slowly being tamed, and, most importantly, macroeconomic stability has been restored. The task now is to convert this stabilization into a confident forward stride.

The restoration of sound macroeconomic management, the decisive shift toward exchange-rate flexibility, and the rebuilding of foreign-exchange reserves have changed the tone of the economy. The "fear phase"-marked by a sliding currency, dwindling reserves and panic behaviour-is behind us. A robust current account position, a healthier balance of payments, and stronger remittance inflows signal that Bangladesh has regained control of its external accounts. These achievements, though fragile, give policymakers the policy space they lacked even a year ago.

The shock to the banking system was unprecedented, but so too was the response. Insolvent banks have been identified, mergers initiated, supervision tightened, and a new playbook for resolution and asset recovery is emerging. For the first time in years, the central bank is asserting discipline-raising policy rates, enforcing asset-quality reviews, and embracing transparency. If this momentum is sustained, 2026-27 could mark the beginning of a more disciplined, credible financial system-one capable of supporting investment rather than distorting it.

Can rapid growth resume? The answer is 'YES', as Bangladesh's structural strengths remain unshaken:

• a globally competitive RMG sector poised to benefit from trade diversion under the US reciprocal tariff regime; industrial progress can continue with trade and industrial reforms

• strong and rising remittance flows, supported by exchange-rate flexibility;

• a resilient agriculture base; and

• a young workforce-two-thirds of the population under 35-ready to drive industrialization, services expansion, and digital transformation.

High-frequency indicators already show a turnaround: Purchasing Managers' Index (PMI) and industrial production are ticking up, export orders are stabilizing, and energy supply disruptions are gradually easing. Once political clarity returns after the 2026 elections, a release of pent-up investment-domestic and foreign-could lift growth back toward 6 percent and more by FY27.

The emerging global order raises the stakes for Bangladesh. With targeted reforms-trade policy reforms, logistics, tax modernization, stronger financial governance, and export diversification-Bangladesh can convert global turbulence into strategic advantage and move into the next generation of export-led growth.

The country has overcome crises before-and each time has emerged stronger. With disciplined policy, a fair election, and continued structural reforms, it can do so again. A free and fair election under the auspices of the Interim Government, in February 2026, will be the ultimate gift this nation and its people can hope for.

Dr Zaidi Sattar is Chairman and Dr Ahmed Sadek Yousuf is Senior Economist at Policy Research Institute of Bangladesh (PRI). zaidisattar@gmail.com; ahmed.sadek87@gmail.com