The International Monetary Fund (IMF) agrees to lend Bangladesh US$4.5 billion to help replenish its foreign-currency reserves, weighed down by high global inflation, in a package that includes wide-scale reforms.

As a visiting IMF mission wound up spot check of the country's financial health and economic fundamentals, both sides in separate press declarations Wednesday revealed the preliminary agreement that would need the seal of approval from the Fund's board in Washington.

Bangladesh is currently confronted with a twin problem: it counts a budget deficit and its US-dollar reserves plummeted for having to foot high import bills against lower remittance inflow and export-earnings fall.

As such, mounting global inflation threatens macroeconomic stability of the country, as it does in case of many other countries.

Of the total sum, $3.2 billion will be given under the Extended Credit Facility (ECF) and the Extended Fund Facility (EFF) while $1.3 billion under the Resilience and Sustainability Facility (RSF).

The IMF gave an announcement to this effect Wednesday in Dhaka after conducting the 15-day-long staff-level mission which reached an agreement with the government of Bangladesh.

To grant the loan amount the IMF put forward some reform priorities to the government, which include raising the tax-to-GDP ratio, modernising monetary policy framework, improving business climate, and mobilising additional financing to meet the spending needs.

Also, the exchange rate flexibility, enhancing governance and the regulatory framework in financial sector, developing capital markets, boosting growth potential, and building climate resilience, among others also on the priority list of the IMF.

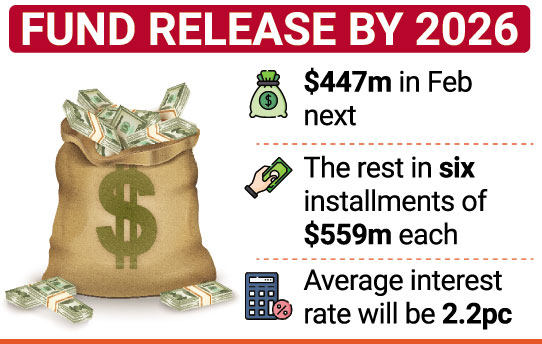

The funds will be available in seven instalments by 2026 with the first instalment of $447 million coming in February. The rest will come in six instalments with each amounting to $559 million. With floating interest rate in nature, the average rate on the loans will be 2.2 per cent, according to Finance Minister AHM Mustafa Kamal.

IMF country chief Rahul Anand, who led the IMF delegation, at a press briefing said out of the war in Ukraine the global commodity prices rose significantly and Bangladesh being an import- dependent country has to import fertiliser, energy, capital machinery-almost all items-which put pressure on import payments leading to high current-account deficit.

"…we have reached a staff-level agreement to support the authorities' reform agenda to support what they are trying to do to stabilise the macroeconomy and also to meet the immediate challenges," he told the press.

He anticipates the country's balance of payments to remain under pressure for some time. Also due to higher need of subsidies and expenditure with lower tax base, Anand said, the budget deficit may also remain high this fiscal year.

The IMF in a statement said higher revenue mobilisation and rationalisation of expenditures will allow increasing growth-enhancing spending. "The impact on the vulnerable will be mitigated by higher social spending and better-targeted social-safety- net programs."

"The monetary stance will be guided by the inflation outlook. Monetary policy modernisation will promote macroeconomic stability and improve policy transmission. Increased exchange-rate flexibility will help buffer external shocks," it said.

The IMF also says reducing financial sector vulnerabilities, strengthening oversight, enhancing governance and the regulatory framework, and developing capital markets will help mobilise financing to support growth objectives.

"Creating a conducive environment to expand trade and foreign direct investment, deepening the financial sector, developing human capital, and improving governance to enhance the business climate will lift growth potential," says the agency.

The US-based lender further says strengthening institutions and creating an enabling environment will help meet climate objectives, support large-scale climate investments, and help mobilise additional climate financing.

In a separate press briefing on the day, the Finance Minister, AHM Mustafa Kamal, said the IMF agreed to provide the loans in line with the government's plea and did not impose any new conditions.

"The IMF has prioritised the same reforms the government had been carrying out," he added.

He mentions that the government has been working on raising revenue earnings, the formation of an asset-management company to dispose of non-performing loans, supplying adequate machines to raise VAT collection etc which the IMF team also reminded of.

Asked whether the IMF team put conditions like raising interest rates on deposits and loans in banking sector, the minister answered in the negative.

"Unless there was a cap of 6.0 per cent and 9.0 per cent interest on bank deposits and loans, the country might have been destroyed meantime," Mr Kamal said, pointing at the impacts of pandemic.

On a question about continuation of tax waiver, he said it has to be continued for the sake of common people, otherwise people will suffer seriously.

Bangladesh Bank Governor Abdur Rouf Talukder said the reform proposals the finance minister placed in parliament during the last four years, and the reform pledges the Prime Minister made on different occasions on climate issues are the main conditions tagged with this loan package.

He said the government reiterated its position to the IMF on continuation of subsidy on fertiliser as agriculture is main product of the country.

On energy, the IMF was apprised that the prices had already been adjusted with the international market. The IMF has suggested adjusting the energy prices periodically, but there was no proposal for further adjustment at this moment.

"In line with the IMF proposal the central bank agreed to calculate net position of foreign-currency reserves alongside the gross amount," says Mr Talukder, adding that according to the IMF calculation the present forex reserves are worth $28.3 billion.

syful-islam@outlook.com