Investment in savings instruments

Inflation erodes yields for savers

Economists for interest rate raise to cushion inflation effect

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Savers are losing out as high inflation makes inroads on yields from the savings instruments this section of people have invested in as their last resort, sources say.

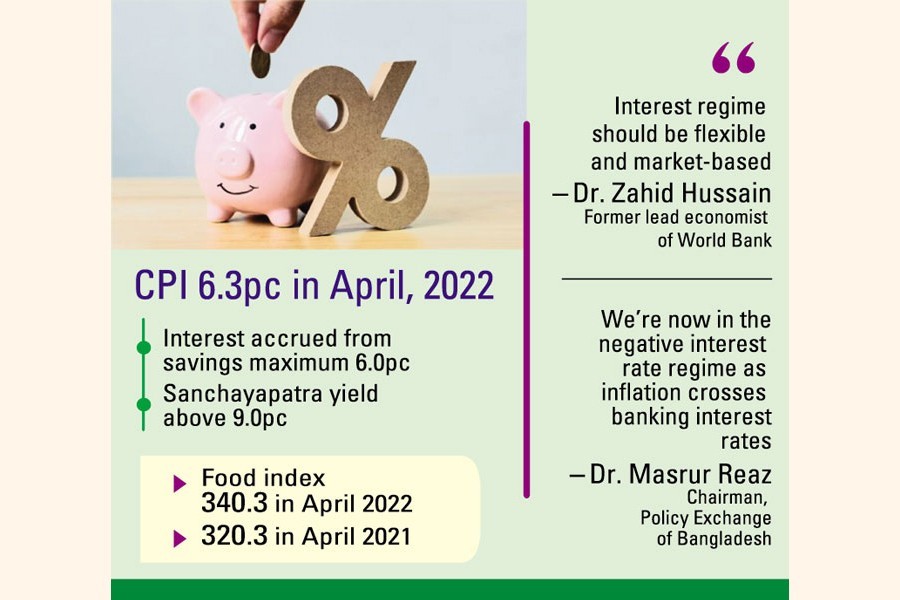

These individuals, who rely on savings to supplement their income, are finding it significantly harder to go along with the Consumer Price Index climbing to 6.3 per cent in April 2022, although public perception of the macroeconomic indicator is much higher than the official arithmetic.

Economists fear rising inflation means that the cost-of-living crunch will continue to get tighter over the coming months, particularly when energy bills will jump as per the recommendations by the authorities concerned.

The interest accrued from savings is a maximum of 6.0 per cent. The yield from the risk-free government sanchayapatra remained above 9.0 per cent, but real earnings of the investors also declined as a result of the higher inflation.

The scope for investment in the government savings instrument is believed to be part of social safety-net recipe meant for sustenance of disadvantaged groups of people, like the elders, orphans and widows.

Inflation figures published Wednesday showed the food index having surged to 340.3. It was 320.3 in April 2021. Inflation in Bangladesh increased not only because of volatility on the global market, especially for the war in Ukraine, but there are domestic supply-chain disruptions as well.

Bangladesh Bureau of Statistics (BBS), the country's national statistical outfit, also showed costly edible oils, wheat, and some vegetables, including brinjals/eggplants, as the most significant drivers behind the rise in annual inflation between May and April.

There are no inflation-beating accounts available in the banking system in the country for the limited-income groups of people. But the central bank recently asked the banks to maintain a gap with the rate of inflation applicable to term deposits.

But this is not applicable to general savings bank accounts consisting of around 22 per cent of total deposits in the banking system.

Dr Masrur Reaz, chairman of Policy Exchange of Bangladesh, told the FE this situation is called "financial depression".

"We're now in the negative interest-rate regime as the inflation has crossed the banking interest rates."

He points out that the weak local currency against the US dollar also sheds the BDT value, and feels that there is a need for raising the interest rates to help the beneficiaries gain benefit from the savings.

"People trying to save…will see inflation eating into their hard-earned savings faster than it grows unless they seek out the few accounts that can keep pace with inflation," he says.

Dr Zahid Hussain, a former lead economist of the World Bank, suggests that the interest regime should be flexible and market-based.

He also mentioned that the Bangladesh Bank recently asked the banks to consider the inflation rate while offering interest rates applicable to FDRs.

Banks, however, cannot raise interest much as there is a maximum restriction on lending at 9.0 per cent. "How much the banks can raise the interest when their lending cap is restricted at 9.0 per cent."

He also mentions that the BERC has recommended a bulk power-price hike by 57 per cent which will impact the rate of inflation in the coming months.

"Power-tariff hike is contagious and its spillover happens fast, leading to surges in the inflation," the economist told The Financial Express.

jasimharoon@yahoo.com