Formal credit growth for private sector plummeted to a historical low of 4.72 per cent as per latest data available up to March, indicating holdback in economic pickup for multiple adversities.

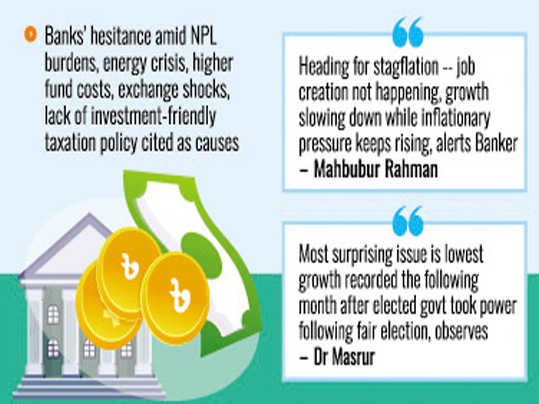

Such ebb tide in investment credits is attributed to banks becoming more cautious amid higher non-performing loan (NPL) regime and private borrowers losing their credit appetite due to multiple anti-business factors, including energy crisis, higher lending costs, exchange-rate shocks, and existing taxation policy which is deemed not investment-friendly.

Data from Bangladesh Bank (BB) on private-sector credit growth, available since 2003, show that the growth has never dropped this low, even during previous financial shocks.

According to the central bank, the private-sector credit growth plummeted to 4.72 per cent by end of March last -- the lowest in the history of Bangladesh. The previous lowest growth recorded in the previous month of February 2026.

In fact, growth in private-sector credits has hovered around single digits since August 2024, reflecting prolonged sluggishness in the $460-billion economy, which is largely private-sector-led.

Seeking anonymity, a BB official says the central bank continues its contractionary monetary policy stance (MPS) with the policy rate kept at 10 per cent as part of inflation-control measures, despite criticism from business circles.

"The higher lending rate, energy crisis and external shocks steaming from the crisis in the Middle East are major reasons behind the plummeting credit demand," the official adds.

He mentions that the half-yearly MPS projection for private-sector credit growth up to June next is 8.50 per cent, but the current growth remains below this target. However, growth could pick up in the last quarter of FY'26.

President of Bangladesh Knitwear Manufacturers and Exporters Association (BKMEA) Mohammad Hatem says entrepreneurs have been battling hard to survive on the market under these prevailing extreme business and investment climate.

He lists multiple factors like ongoing prolonged energy crisis, higher borrowing costs and "anti-business taxation policy" that make survival of the businesspeople difficult.

"Under such circumstances, who dares to think of business expansion? I don't know how the growth (4.72 per cent) has happened and who are the borrowers? Will they be able to repay the loans? I have enough doubt," he says.

Managing Director and Chief Executive Officer of Mutual Trust Bank (MTB) PLC Syed Mahbubur Rahman says the volume of opening LCs (letter of credits) has dropped significantly in recent times because of persisting prolonged economic sluggishness.

Because of the plummeting credit appetite from the private sector, he notes, the commercial banks have intensified their concentration on investing in state-secured government securities (treasury bills and bonds) to make some gains amid the ongoing economic slowdown.

The experienced banker thinks the country is basically heading towards stagflation as job creation is not taking place and growth is slowing down while inflationary pressure keeps rising.

"In fact, both internal and external factors are not conducive to investment and business expansion. That is the reason behind the plummeting credit growth," he told The Financial Express.

Managing Director and CEO of NRBC Bank Dr Md. Touhidul Alam Khan says this prolonged sluggishness is primarily due to the central bank's tight monetary policy, implemented to combat inflation, coupled with elevated commercial lending rates that have dampened borrowing enthusiasm.

Furthermore, he says, a subdued appetite for new industrial investments, exacerbated by broader economic uncertainties and severe liquidity constraints within the banking sector, has significantly curtailed lending capacities.

"These constraints are further compounded by rising non-performing loans and increased government borrowing from commercial banks to finance the budget deficit," says the seasoned banker.

Dr. Khan adds that this sustained decline in credit flow to productive sectors could impede capital-machinery import, stifle manufacturing output, and ultimately jeopardise Bangladesh's broader economic recovery in the current fiscal year.

Director-General of Bangladesh Institute of Bank Management (BIBM) Dr Md. Ezazul Islam thinks private -sector credit growth to the volume of around 5.0 per cent is not bad if it goes to the productive sectors.

"A double-digit growth will bring nothing positive if the money goes to non-productive sector, which would fuel inflation further," he says.

Chairman of Policy Exchange Bangladesh Dr M Masrur Reaz says the private-sector credit growth remains a matter of concern for the country for more than a year but the growth was over 6.0 per cent.

"Now, it dropped below 5.0 per cent. It goes to severe worrying level from concerning level. But the most surprising issue is the lowest growth recorded in the following month after an elected government took the state power following a fair election," he notes.

About the reasons, the economist says Bangladesh under the immediate- past interim government saw scanty reforms activities in streamlining trade and investment ecosystem here.

As a matter of fact, the business environment significantly weakened in recent times and the ongoing crisis in the Middle-Eastern countries worsened the situation further, according to him.

jubairfe1980@gmail.com