Vote eases political, policy uncertainty, supports macroeconomic stability

Says Fitch Ratings, stresses reform for economic uptick

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

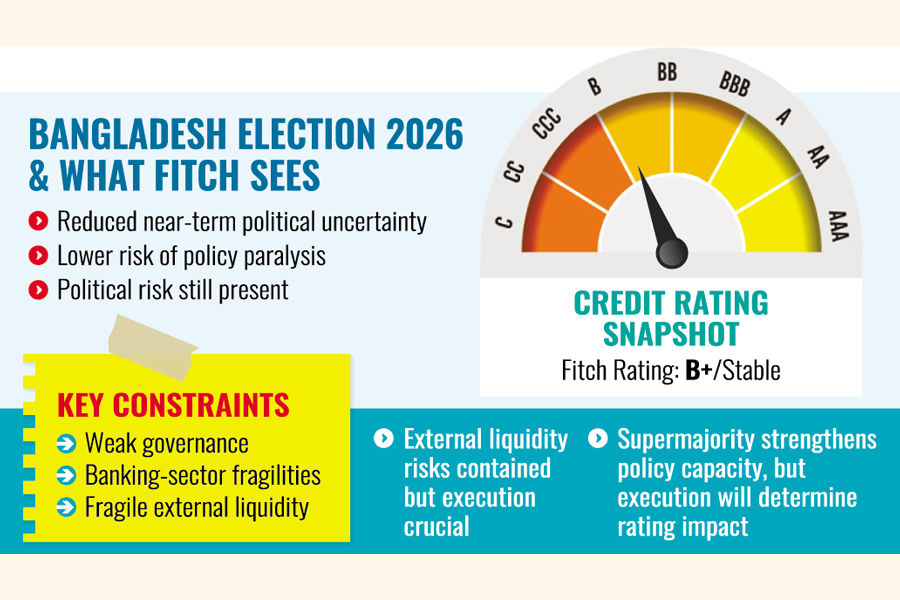

Bangladesh's general election has reduced near-term political and policy uncertainty in a turnaround that could support improvements in macroeconomic stability, says Fitch Ratings in its post-poll positive assessment.

The Bangladesh Nationalist Party (BNP)-led alliance has secured a parliamentary supermajority in the February-12th polls, alongside a majority "yes" vote in a referendum that could enable constitutional reforms, the credit-rating agency says.

However, longstanding credit constraints - weak governance, banking-sector fragilities and a fragile external liquidity position - mean the new government's ability to execute its macroeconomic and fiscal reform agenda will determine the rating impact.

It views that the election outcome provides greater political clarity following the August 2024 overthrow of the Awami League government and a prolonged caretaker period that advanced several significant reforms.

The BNP won 209 seats, with Jamaat-e-Islami and its allies taking 77 and smaller parties the remainder, of the 299 seats contested.

"The two-thirds parliamentary majority of the BNP alone should support its ability to implement its policy agenda", the British-American ratings agency says in its latest report.

The report also says election also reduces the risk of a prolonged political vacuum that could complicate economic decision-making.

"Political risk still remains, despite the election win," it alerts.

Bangladesh's (B+/Stable) history of political polarisation and periodic pre-election violence leaves scope for renewed tensions if election promises prove difficult to deliver and the government underperforms expectations.

The military may also continue to play a role in politics.

Meanwhile, the referendum approval could support constitutional changes aimed at strengthening institutions, for example, shifting to a bicameral system from unicameral, strengthening judicial independence and instituting term limits for the prime minister.

However, implementation could be complex and time-consuming, keeping execution risk elevated.

"Policy signals in the BNP manifesto indicate the new government is likely to sustain a path of economic and fiscal reforms initiated under the caretaker government."

The agenda also points to higher social spending, which could add pressure to public finances if revenue ?mobilisation measures underperform, and would test the authorities' ability to balance growth and electoral commitments with fiscal consolidation.

This reform agenda appears consistent with the macro-stabilisation agenda under the US$5.5 billion International Monetary Fund (IMF) programme that began in January 2023 and runs through 2026-2027.

However, there are still uncertainties around the economic agenda, and ongoing reform implementation and durability of such reforms beyond the IMF programme will be a key condition for facilitating macroeconomic stability and growth.

The manifesto's fiscal centrepiece is a medium-term goal to raise the tax-to-GDP ratio to 10 per cent through tax-administration reforms, fewer exemptions and a broader tax base, alongside a near-term revenue increase of 2.0 per cent of GDP, the report cites.

"This matters for credit quality because Bangladesh's structurally low revenue intake remains a key weakness. We project general government revenue-GDP to reach 8.6 per cent by FY27, from 7.8 per cent in FY25.

The manifesto also points to a pro-private-sector development agenda - simplifying licensing, offering incentives for export-oriented sectors and aiming to lift foreign direct investment to 2.5 per cent of GDP from a Fitch-estimated around 0.4 per cent of GDP in FY25.

Its pledge to strengthen banking governance and tackle non-performing loans could, if successful, address a key constraint on the sovereign credit profile.

External liquidity remains another near-term indicator even as reserves improve. Foreign-exchange reserves reached $29.7 billion as of 10 February, up from $22.3 billion in the fiscal year ended June 2024 (FY24) and $26.9 billion in FY25.

A manageable external debt-repayment profile and the prevalence of government-backed debt help contain refinancing risks, but also underscore the importance of maintaining macro-stabilisation policies that keep external financing risks in check.

jasimharoon@yahoo.com