Mapping the Covid-19 implications for Bangladesh's stock market

Suborna Barua, Akramul Alam, Isfaqur Rahman and Rakibul Hossen

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Financial markets worldwide are responding abruptly to the on-going coronavirus pandemic. The Covid-19 pandemic is likely to produce widespread impacts on financial markets and institutions in almost each affected country. Bangladesh is no exception. Although the stock market is yet to prove its dominance in the market for capital financing in Bangladesh, the Covid-19 pandemic is not likely to spare it.

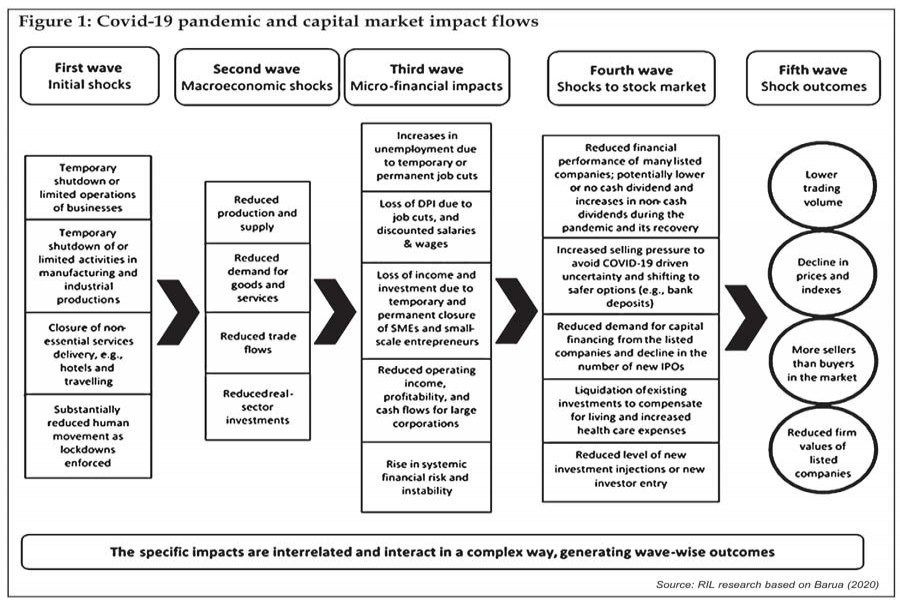

The already rattled stock market in Bangladesh has begun to reflect adverse impacts of the coronavirus pandemic since February 2020. During the pandemic period from February 27, 2020, to June 10, 2020, the market value of equities tumbled by 11.50 per cent along with daily market volatility (standard deviation) of 2.20 per cent (in annualised term it becomes as large as 98.30 per cent). The Dhaka and Chittagong stock exchanges resumed operations on May 31, 2020, after a prolonged lockdown period since the last week of March 2020. Yet, the situation so far doesn't seem to offer much hope. Few weeks before the lockdown was imposed, the Bangladesh Securities and Exchange Commission (BSEC) introduced floor prices for all the listed securities to recover the normally-declining market trends. However, that doesn't appear to help much so far as trade volume trends to decline, and the emergence of the Covid-19 pandemic adds to the injuries through adverse micro and macro-level impacts. After resuming the market, investors appear shaky and worried about overall economic and financial uncertainty, reflected by a sharp decline in trading activities. The trading value of the leading bourse was at 13-years low at Tk 430 million on June 5, 2020. Given the unprecedented level and nature of uncertainty triggered by the Covid-19 pandemic, the stock market in Bangladesh could see complex and severe consequences in the coming days. Figure- 1 shows the mapping of the likely implications of Covid-19 for Bangladesh's stock market. The Figure is mostly self-explanatory. The stock market is likely to experience different shocks arising from macro and microeconomic and financial shocks produced by the Covid-19 pandemics. Due to lockdowns and movement restrictions, production of and demand for goods and services in Bangladesh have already slumped and trade flows have already shrunk resulting in lower exports revenues. These impacts are generating massive job and pay cuts and forcing millions to embrace zero or minimal income and poverty. It is important to note that we are currently experiencing effects from the first to third waves, and thus the pure and visible stock market impacts shown in the fourth and fifth waves are mostly yet to emerge.

The stock market is a platform of demanders (e.g., investors) and suppliers (e.g., issuers and secondary market sellers) of financial assets or securities. Therefore, the pandemic's shocks to the stock market are likely to arise mainly from the economic and financial impacts generated by on the two sides of the market - demanders and suppliers of securities. To have a simplified understanding of the likely Covid-19 implications for the stock market, we shed light on Covid-19's major implications from the lenses of the two sides.

EFFECTS TRANSMITTING THROUGH THE DEMAND SIDE: The pandemic has already reduced consumer spending, particularly on non-essential goods and services, induced by nation-wide lockdowns and a drastic fall in income and savings. The key reason for income losses is the loss of employment and pay cuts due to temporary or permanent closure of businesses and industries in the face of lower demand for goods and services. The employment loss is likely to slash primary occupational disposable incomes (DPIs) for many stock market investors by a large margin, which otherwise could be used for investment in normal times. A recent BRAC survey shows that about 95.0 per cent of people in Bangladesh appear to experience income losses due to Covid-19, while earnings of 51.0 per cent have reduced to zero. As the crises prolong and lockdowns extend, many investors are fearful of losing income even further in the coming days, as Job cuts and employment losses are likely to keep going in the next several months. This shuts down the door for new investment injection into the stock market from the majority of small investors and new entrants. The situation is likely to worsen (or perhaps has begun to worsen already) further as many investors are to withdraw their savings (e.g., in banks) and/or liquidate their current investment from the stock market in a desperate effort to cope up and survive the prolonged economic and financial distress. Many retail investors are likely to dispose of their assets from the stock market to meet suddenly increased expenditures for healthcare, family maintenance, and interest payments to existing loans and credit cards. Many of those who do not need to liquidate investments at the moment but expect a worse future may dispose of their investments in risky assets such as in the stock market and divert funds to relatively safer investment platforms like different deposit scheme in banks. However, shifting towards bank deposits might still be worrisome as banks face growing criticism about increasing NPLs and competing in an overcrowded market.

Investors who still will try to stick to the stock market and grow their investments will have to do it with a widened range and increased level of uncertainties, making their investments in the stock market even riskier. For example, many investors are already worried about the likely operating, profitability, and cash flow impacts of the Covid-19 pandemic on the listed companies in the next years. Reduced levels of corporate incomes, profit, and cash flows could lower dividend returns substantially, particularly for those who have made long-term investments in different stocks. Furthermore, because Covid-19 exerts a complex economic and financial market across the economy, stock market behaviour may not be the same in the future as it was doing before the pandemic. This might reduce returns from price gains for day-trading investors, as the market may become more volatile with lesser liquidity in the coming days.

EFFECTS TRANSMITTING THROUGH THE SUPPLY SIDE: There are at least three ways how Covid-19 impacts could be translated through the supply side. First, the publicly listed companies in the stock market fall into a big trap of losing business activities due to demand fall and operation and factory closures. Fresh investments in new projects as well as Balancing, Modernisation, Rehabilitation and Expansion (BMRE) investments are likely to be reduced substantially due to capital shortage and lack of financial viability. This could further worsen future growth and financial performance of the listed companies, forcing existing plans of long-term investment to cancel or put on hold. Second, the forced shutdown and voluntary closure of many businesses and industries to avoid health hazards will substantially limit exports and imports, corporate operations, industrial production, operating income, profitability, and cash flow generation. Similar global trends observed are to further worsen conditions for companies who largely rely on export revenues and imported materials. In such cases, companies may choose to offer more non-cash dividends to maintain investor confidence and abandon cash dividend offerings. Third, for some non-cyclical industries e.g. foods, pharmaceuticals, and utilities may not be able to fund their business at full scale because of lesser credit availability. Shortage of credit may arise as banks and financial institutions face liquidity shortage due to aggressive investment liquidations and fund withdrawals by depositors to survive the pandemic. The credit shortage could turn out a blessing for the stock market. As the companies find it hard to get loans from banks and other non-bank financial institutions (NBFIs), some of them may consider going for IPOs in a desperate move to raise large funds. However, the number of companies opting for an IPO may be subdued by overall economic distress faced by businesses and industries in the economy.

SECTORAL IMPLICATIONS FOR LISTED COMPANIES: The Covid-19 hits on growth and performance of most of the listed companies is generally to be reflected by the drop in the market value of their stocks. Since the global, as well as the national economic activities, decline significantly in the area of trade and commerce, transport and logistics, production of heavy industries; the majority of the publicly traded companies' business prospects and financial performance affected significantly. Research by the Research and Innovation Lab (RIL, 2020) shows that 13 out of 18 equity sector categories in the Dhaka Stock Exchange could embrace growth and performance downturns; while four of the sectors have the potential for generating growth and performance gains from the ongoing pandemic.

DSE listed sectors as Pharmaceuticals, Food & allied, Fuel & power and IT are expected to see significant benefit. The Pharmaceuticals sector could see a surge in their business as the pandemic pushes demand for medicines and healthcare to go up and creates the opportunity of new health products and necessary medicines targeting a local and global market. One such example is Beximco Pharma and Beacon Pharma being the front runners in producing Remdesivir - a potential treatment for Covid-19. Telecommunications and IT could long-lasting increases in customer demand and business performance, as demand for online shopping, meetings, webinar, podcasts, and video games etc. spikes up manifold while people work, socialize, and enjoy alternative entertainments staying at home. Among others, non-cyclical industries such as utility sector are expected to perform consistently, as power generation and transmission are not axed directly by the lockdowns and performance and business prospects are likely to remain the same.

ASSET ALLOCATION AND POLICIES ARE CRITICAL: All considered, the overall effects could be translated into a decline in investments, stock prices, trade volumes, and market value of the listed companies. Higher selling pressures relative to buying could result in lower prices and trade volumes. From a purely fundamental perspective, Covid-19 effects on revenue growth, profitability, cash flows, and business prospects could affect intrinsic firm values also. In this scenario, investors would need to actively watch out and rebalance their asset allocation to avoid potential losses. The mapping in Figure-1 shows impacts assuming no policy responses. As we are currently experiencing the first to third-wave impacts set out in the Figure, an early response with specific and targeted policies could help the stock market avoid the adverse outcomes. It is true that as long as the pandemic persists, the primary focus of the whole nation remains fighting the pandemic, keeping healthy and safe, and saving lives, and thus, all resources are to be diverted towards fighting the pandemic. This means there may be lesser scope for the government to concentrate on stock market recovery with specific and targeted responses. Yet, investors are hopeful about the role of the newly formed BSEC commission in rebuilding the market fundamentals even in the times of the pandemic.

Suborna Barua is Assistant Professor at the Department of International Business, University of Dhaka, and Consultant at the Research and Innovation Lab (RIL), Royal Capital Limited; Akramul Alam is Senior Research Analyst, Isfaqur Rahman is Research Analyst, and Rakibul Hossen is Research Assistant with RIL. Comments are welcome at

akram@royalcapitalbd.com.

[The opinions expressed in the article does not constitute any investment advices and not necessarily represent that of Royal Capital Limited].