Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Generally, the suppliers of goods or services are liable to pay Value Added Tax (VAT). They supply goods and collects VAT on behalf of the government, which is later paid to the government. In the case of reverse charge mechanism (RCM), the obligation to report the output tax payable from transactions is transferred from suppliers to purchasers. The recipient of the goods or services or both has to calculate VAT and accounts for this amount as "VAT Payable". This amount is declared on "VAT Return as output VAT and at the same time recoverable as "input VAT" through declaration on the "VAT Return" in the same month. The European Court of Justice in the Reemtsma Cigarettenfabriken Gmbh case has precisely described the Reverse Charge Mechanism as "the transfer mechanism of the tax obligation". In sum, a reverse charge switches the obligation to account for and remit VAT to the consumer, rather than the supplier. It is generally recognised that the reverse charge mechanism is not a viable collection mechanism in the B2C context. In the case of RCM, the supplier must inform the customers that the reverse charge applies and must ensure the customers (recipients) know they must account for VAT.

The main objective of RCM is to fight against VAT fraud. A recent study (Poniatowski et al., 2019) estimated the so-called VAT gap in the EU at EUR 137 billion in 2019. In a different case, VAT fraud is estimated to be approximately 10 per cent of VAT revenue within the EU. The VAT gap is a proxy of tax evasion. A significant part of total VAT gap is represented by missing trader frauds or carousel frauds.

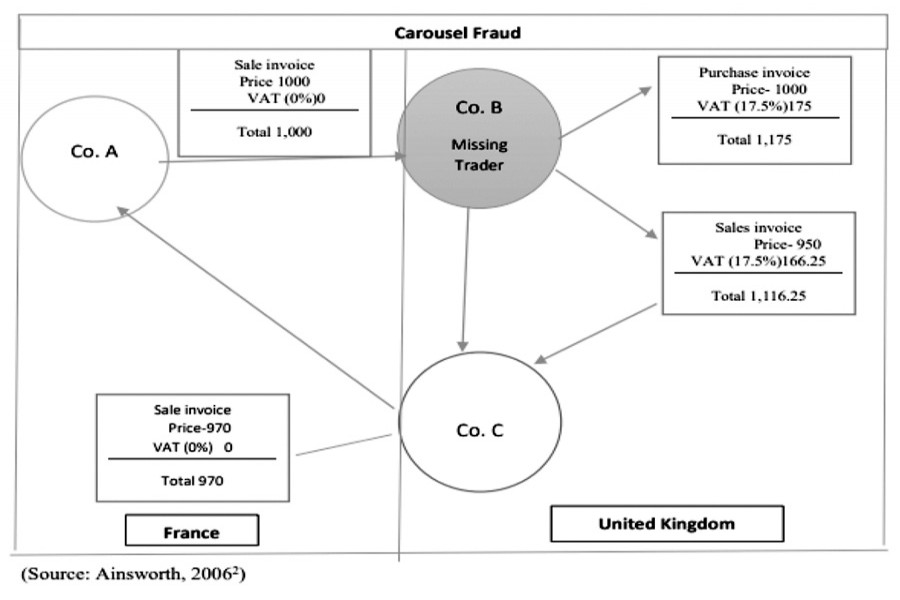

HOW CAROUSEL FRAUD OCCURS: Where the fraud involves repeated transactions between the same parties dealing with the same goods, this types of fraud is called 'Carousel fraud'. This fraud occurs when a seller (A) in a say EU member state X [France] makes an exempt intra-community supply of goods to a (soon to be) missing trader B in member state Y [UK]. This company B acquires goods without paying VAT and subsequently makes a domestic supply to a third company C (called the broker). Company B collects VAT on its supply to C (also called broker) and then disappears (the missing traders do not charge any margin on the goods traded; they even sell the goods cheaper than they bought them to find innocent buffer traders through which the goods can flow in the carousel) without paying VAT to the tax authority. In this case, C claims a refund of the VAT on its purchases from B (the missing trader); If the tax administrator refunds the VAT to Company C, the tax loss arises (which equals the VAT paid by C to B) for the country as the VAT refunded was never collected from the missing trader (Company B). In order to distort VAT investigations, the goods will often be supplied from B to C via intermediary companies, called 'buffers'. This fraud takes place in a cross-border context.

In a fully operational carousel, C will resell the goods back across the border (France) to the initial seller A. This sale is also an exempt intra-community supply. The same goods can then be supplied once again on the carousel to B. As this is an intra-community supply, the supply is zero-rated out of France, and company B is obligated to self-assess the VAT due --17.5 per cent [Euro 175]. This amount is never reported or remitted to the government as company B has the intent to become a 'missing trader''. To complete the carousel, Company C would sell the same goods back to Company A located in France for Euro 970, for a modest profit of 20. Company C will file a return seeking a full refund of input tax (it paid to B) of 166.25 against an output VAT of zero.

The above diagram illustrates the 'Carousel Fraud' cycle.

The reverse charge mechanism is aimed at thwarting VAT fraud. Especially, several EU countries have taken steps to combat the growing problem of EU VAT fraud, by introducing the reverse charge mechanism. The French government has recently introduced the mechanism in respect of supplies made by non-resident suppliers (Quigley,2007).

DOMESTIC REVERSE CHARGE: The VAT legislation of different countries has provision for a RCM to apply on certain domestic supplies. Reverse charge is only relevant if both the customer and supplier are VAT registered. For example, a local reverse charge applies for domestic supplies to VAT registered (or required to be registered) customers in Bulgaria on the acquisition of Investment gold, Waste and related services, such as scrap metal and similar supplies. The UAE government introduced VAT RCM on supplies of gold, diamond and (or products where the principal component is of gold or diamonds, such as jewelry) between registered businesses. The UAE VAT RCM only applies in B2B situation (retail sales are not subject to RCM) where the diamonds and gold are sold to a VAT registered recipient for resale or manufacturing. The supplier has to verify that the recipient is VAT registered. The stated objective of the UAE VAT RCM is to maintain the competitiveness of the precious metals sector and stimulate investment in this sector. The registered recipients of gold can recover the tax they incurred on their purchases in the same tax return in which they show their output taxes due, thus maintaining liquidity and cash flow. In Austria, if construction or building work is performed by a subcontractor to a general contractor, the liability to pay the VAT shifts from the supplier (subcontractor) to the customer (general contractor). The RCM was first applied on gold in 2006 in Czech Republic and gradually extended to other commodities: on emission allowances, certain metals, scrap and waste, in 2011, followed by reverse charge on construction works in 2012. French, Germany and Latvia also have Domestic Reverse-Charge System for the domestic B2B supplies of specific products

REVENUE IMPACT : In the case of RCM, the recipient (customer) of the supply is entitled to input tax credit on the same return, on which he has already reported the amount of VAT to be paid (output VAT). In this self-assessment situation, the case is revenue neutral. The government does not stand to gain any tax amount when the entire amount is available to the VATable person as credit. However, if part of the output is exempt, then RCM mechanism also result in an increase in revenue for the government. This is illustrated in the following example:

Example: A VATable person in Bangladesh imports interior design services for his offices in Dhaka from an overseas supplier. Assume such services are subject to 15 per cent standard VAT rate. As the supplier is situated overseas and the customer is a VATable person in Dhaka, the person liable for the VAT due on import of these services is the customer under the reverse-charge mechanism. The fee for the service is BDT 20,000. The customer will self-account for VAT @15 per cent (i.e. Tk. 3000), will treat this VAT as output VAT due as well as input VAT (as per section 20 of VAT & SD Act 2012). In this case, the net amount of VAT due by the customer to the NBR is 'nil' since the output VAT due is fully netted against the input VAT credit which is the same amount. However, if the customer is only entitled to recover 50 per cent of the VAT incurred on this business expenses (i.e., it uses the expense for interior design services for making both VATable and exempt supplies), he will only be able to recover BDT 1500 (50 per cent of Tk. 3000) as input credit The net amount of VAT due by the customer to the NBR for this supply will amount to BDT. 1500 (BDT 3000 output VAT less BDT 1500 recoverable input VAT).

ADVANTAGES OF REVERSE CHARGE MECHANISM: First, shifting the VAT liability from the supplier to the recipient (of goods or services or both) removes the possibility for suppliers to disappear with VAT that they collected from their customers without remitting to the tax authorities. In other words, RCM helps tackling VAT fraud by removing the possibility of 'missing trader fraud and 'carousel fraud, thus result in reduced 'VAT Gap'. Second, the application of the RCM relieves the foreign supplier of the formalities for tax in the jurisdiction of taxation. It allows foreign suppliers to have business presence in the country of recipient without having VAT registration. Last but not least, it is almost impossible to collect tax from the unregistered dealers. Application of RCM for supply of goods or services or both by unregistered persons to registered buyers helps prevent tax evasion. In sum, it is always hard to collect service tax from the numerous unorganized sectors such as goods transportation, insurance agents etc. Collection of taxes from unorganised sectors becomes possible through RCM.

RATIONALE OF RCM: When the number of tax payers (suppliers of goods or service or both) is large with small tax liability (by each of them) and the recipient of goods or services or both are few, RCM may be a better option for the tax administration. This mechanism makes recovery of tax from the recipients simpler and less expensive. For example, there are thousands of insurance agents who are employed by insurance companies to provide life insurance services. The commission received by each agent is a small amount. By reverse charging insurance companies [as is done under Rule 2(1)(d) of the Service Tax Rules, 1994, CBIC, India] instead of agents, the government can collect the same amount of tax, even more for the services rendered by insurance agents. RCM may also be a better option when the government jurisdictional problem i.e., when the supplier is located outside Bangladesh/overseas). Example- RC on imported service

Governments also find RCM a preferable option to collect tax from some class of professionals and service providers such as security service providers, legal service (individual advocate), service provided by a recovery agent to a banking company or a financial institution or NBFIs etc. Tax recovery from such suppliers is difficult. This provision, will, however, will fail if the supplier and the receipt are unregistered. The recipient will have to be registered.

VAT PAYMENT UNDER RCM: Usually, the supplier of goods or services pays the tax on supply. In the case of Reverse Charge, the recipient of goods or services becomes liable to pay the tax, i.e., the chargeability gets reversed.

RCM IN BANGLADESH VAT SYSTEM: RCM for collection of VAT is in practice on import of services in Bangladesh. The importer of services, if registered, will pay VAT on RCM by depositing the amount through treasury chalan. As per section 20 of the VAT & SD Act, 2012, an importer of services will show the VAT on imported service as payable in part-3 of the VAT Return and avail input tax credit simultaneously by showing the same amount (shown as 'payable' in part 3) in part-4 of the same return. This dual treatment of VAT on the return will not increase or decrease the VAT liability of the importer of services. In the case of import of services by a person not registered or enlisted, banks or relevant financial institution (of the service importer) deducts VAT on import of services while making payment (bill of service import) and deposits to the Government through its own VAT return (Rahman,2020). The importer of services declares this import service cost as an input cost in Mushak-4.3. This creates a positive (although very little) impact on the revenue collection. However, NBR reaps some benefits of the RCM in the case of rent of office/factory. Although the NBR did not mention the words 'reverse charge', the VAT payable on rents of office space by business tenants is an VAT by RCM. The acquirer of services i.e. the tenant is paying VAT instead of the unregistered supplier i.e. individual owners of houses/real estate.

SELF-INVOICING FOR RCM: Self-invoicing (or billing) is to be done when the recipient has purchased from an unregistered supplier and such purchase of goods or services falls under reverse charge. This is because the supplier cannot issue a VAT-compliant invoice to the recipient, and thus the recipient becomes liable to pay taxes on their behalf. The supplier's name has to be entered as the 'Vendor Name' in the invoice. Since the recipient (customer) has the VAT registered business, they are the ones who must include their VAT registration number on the invoice. It is not clear from our legislation if self-invoice is to be made.

COMPLIANCE UNDER RCM, AND INPUT TAX CREDIT: A person who is required to pay tax under RCM has to compulsorily register under VAT irrespective of the threshold limit of registration. Legal provisions in this regard will be needed in the VAT Act. It is necessary to ensure (as per R-46 of the Indian CGST Rules 2017) that every tax invoice issued by the registered person mentions whether the tax in respect of supply in the invoice is payable on reverse charge.

MAINTENANCE OF ACCOUNTS BY REGISTERED PERSONS: Every registered person is required to keep and maintain records of all supplies attracting payment of tax on reverse charge.

PAYMENT OF TAX LIABILITY: Any amount payable under reverse charge shall be paid by debiting the bank account/depositing cash into the treasury. Indian GST regulation does not allow Reverse charge liability to be discharged by using input tax credit. However, after discharging reverse charge liability, credit of the same can be taken by the recipient, if he is otherwise eligible.

The recipient who pays VAT on reverse charge basis can take the input tax credit of the tax paid under reverse charge. VAT (or GST) paid on goods or services under reverse charge mechanism is available for input tax credit to the registered recipient if such goods and/or services are used, or will be used, for business or furtherance of business.

FEW CONSIDERATIONS: Fraudsters usually commit Carousel frauds by a combination of the VAT exemption of the cross-border supply of goods (between Member States where transactions are VAT exempted (due to being the member of the same Union/Single Market) and an accumulation of high input and output tax obligation within one company acquiring goods from another member state. In this case, the tax evasion occurs on subsequent domestic supply cases. As Bangladesh is not a member of such a Single Market (like the EU) and the cross-border supply is not VAT exempted, the risks of carousel fraud is low in Bangladesh. However, NBR may consider adopting Reverse Charge Mechanism in a limited scale in the following cases to expand VAT network and to check VAT fraud:

- On imported services (to remedy the jurisdictional problem),

- Supply by an unregistered person-- when a registered person purchases taxable goods or services or both from an unregistered supplier, then the registered taxpayer may be required to pay VAT on reverse charge basis (only for certain goods/services);

- Reverse charge VAT may be imposed on goods or services or both notified by the government. The specific list of goods and services (which are prone to VAT fraud; in this regard, a clue can be had from the EU regime; EU Member States apply the RCM to domestic supplies in economic sectors plagued by a low tax morale; source: Walpole, 2014), may be selected by a high powered committee. Indian government imposes RCM VAT on the recommendations of the GST Council [constituted under Article 279 (1) of the Amended Indian Constitution] on specified goods and services such as cashew nuts, silk yarn, raw cotton, bidi wrapper leaves, tobacco leaves, supply of lottery etc.

- Professional services may also be subjected to RCM. For example, Legal Services by an individual advocate to any business entity located in the taxable territory, service provided by a goods transport agency (GTA) in respect of transportation of goods by road, where the person liable to pay freight is any factory registered under or governed by the Factories Act, 1948, construction services between builders, renting of motor vehicles to corporate entities, and services provided by the Recovery Agents.

RCM is aimed at combating VAT fraud. It will contribute to increased VAT compliance for the country as a whole. However, it may be burdensome for the small supply receivers. RCM may be useful if the modus operandi is made available on applicability of RCM (i.e., when reverse charging of VAT is required), what are the specified goods and services to be subject to RCM input tax credit mechanism and the records to kept under RCM. The reality is that without section 20 of the VAT & SD Act, 2012 we do not have any rule/guidance concerning VAT RCM. In the case of import of services, the standard practice with regard to VAT on inbound supplies is to collect VAT through a reverse charge mechanism for B2B supplies.

Dr Mohammad Abu Yusuf is a Trainer at the Foundation of Chartered Taxation of Bangladesh (FCTB), and a VAT analyst. ma_yusuf@hotmail.com