Emerging vulnerabilities during COVID-19 crisis

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The impact of Covid-19 crisis on the livelihood realities of millions of poor and vulnerable people in Bangladesh has been exceptional. The importance of generating real-time evidence to analyse the extent and dimensions of poverty impact cannot be over-emphasised. To address the need for real-time research evidence, Power and Participation Research Centre (PPRC) and BRAC Institute for Governance and Development (BIGD) teamed up to conduct rapid response telephonic surveys on livelihood, coping and recovery dynamics during the Covid-19 crisis.

The organisations undertook the survey in two phases. Phase I of the survey captured the immediate impact of the crisis in April 2020 at the beginning of the crisis in Bangladesh and Phase II analysed the evolving nature of the economic impact of COVID-19 on the poor and economically vulnerable populations to understand the recovery journey of this demographic since the lifting of the 'general holidays'. The second-round survey questionnaire was designed to provide further insight on the respondents' current state taking into account their health conditions, expenses, financial life, and perceptions on relief governance and local leadership along with their needs and expectations. Phase II was carried out in June 2020 with the support of the World Food Programme (WFP) - the Nobel Peace Prize winner of this year. Given the restrictions on mobility and interaction because of Covid-19, PPRC and BIGD utilised respondent telephone databases from earlier surveys on urban slums and rural poor. The sample was mainly drawn from two databases - BIGD's census on 24,283 urban slum households and BIGD's nationally representative survey on 26,925 rural households.

Phase I was conducted on 12,000 households of which 5,471 households were successfully reached. In Phase II, 6,200 additional households were included from the same datasets. Of the final sample of 11,671 in Phase II, 7,638 were successfully interviewed, of which 4,424 are panel samples - those surveyed in Phase I. This article mainly focuses on the key findings of Phase II.

RESPONDENT PROFILES: The respondents of the study were classified into four income categories based on per capita reported income for February 2020 (pre-Covid) - (i) extreme poor or households with income below or equal to the lower poverty line, (ii) moderate poor or households with income above the lower and below or equal to the upper poverty lines, (iii) vulnerable non-poor or households with income between the upper poverty line income and the median income (BDT 3,872 for 2020) and (iv) non-poor households with per capita monthly income above the median income.

The sample had a strong poverty bias - 38 per cent of the sample were extremely poor, 18 per cent moderate poor, 18 per cent vulnerable non-poor and the remaining 26 per cent were non-poor. In terms of main sources of income, 40 per cent of the main earners were informal workers such as rickshaw-pullers, housemaids and day labourers, 28 per cent of them salaried wage earners such as garments workers, 20 per cent had business as their source of income and 8 per cent were involved in agriculture.

Overall, 56 per cent of the sample was from urban slum-dwelling households across city corporations and municipalities whereas 43 per cent was from rural Bangladesh; one per cent of households were from Chattogram Hill Tracts.

IMPACT ON INCOME AND THE EMERGENCE OF 'NEW POOR': The 'lockdown' or general holiday implemented by the government of Bangladesh to curb the pandemic had quite an impact on the income and poverty status of different categories of households, indicating a system-wide income shock. In June, the income of moderate poor, vulnerable non-poor and non-poor households dropped by 41-45 per cent compared to their income in February while the extreme poor who has a very low income to begin with, suffered an income drop of 34 per cent.

The emergence of 'new poor' has been a crucial finding of both phases of the study. The 'new poor' are the ones whose per capita income was above the poverty line in February but they fell below the poverty line immediately after the Covid-19 crisis; most of them belong to vulnerable non-poor households. According to Phase II of the study, the national estimate of 'new poor' was 21.7 per cent in June. This means that beyond the 20.5 per cent of the population officially recognised as poor, there are a vast number of additional people or the 'new poor' who need to be brought within the discussion on poverty.

POVERTY DYNAMICS: FEBRUARY-APRIL-JUNE 2020: The findings from the panel households in terms of their changing poverty status over the February-April-June cycle provided an opportunity to examine the short-term poverty dynamics. It was found that 54 per cent of the households under the study are chronic poor - those who were poor before the pandemic and remained poor during both phases of the survey. Then there are the new poor, as mentioned before, constituting 21.4 per cent of the panel sample. An additional segment of the 'new poor' are the later fallers - those who were not poor in February and April but fell below the poverty line in June. They were more prominent in the rural sample (8 per cent) than in the urban sample (3 per cent).

On a positive note, 7 per cent households under the 'revival' category were non-poor in February, became poor after the pandemic in April but recovered to non-poor status in June. On the other hand, 4.23 per cent of the households were 'sustainable non-poor' - they did not fall below the poverty line between February to June.

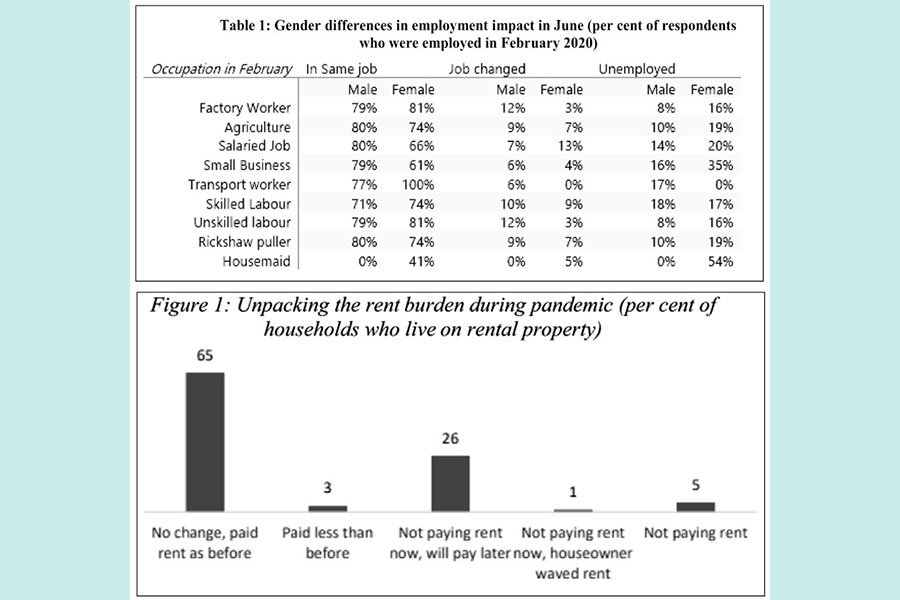

LABOUR MARKET DYNAMICS : The impact of the Covid-19 crisis on the livelihood of people is another major finding of the survey - 17 per cent households lost their livelihoods and became unemployed, 76 per cent held on to their jobs and 7 per cent shifted to another job. The livelihood impact can be seen not only in job loss but also in the loss of earnings among those continuing the same occupation. Rickshaw pullers suffered the highest income drop of 54 per cent whereas unskilled workers, transport worker and small businesses suffered nearly 50 per cent drop in earnings.

Female workers are considerably worse off compared to male workers during this crisis - housemaids are the worst affected with 54 per cent unemployment in June. On the other hand, 35 per cent female small business owners became unemployed compared to 16 per cent male business owners. In fact, the unemployment rate of women in almost all the common occupations was higher than men. While informal and women-centric occupations suffered significantly more in terms of loss of livelihood, no occupation was immune to the shock.

IMPACT ON FOOD SECURITY: Four indices were developed to examine the impact of the Covid-19 crisis in food security - hunger index, negative coping, post-opening food expenditure recovery and nutritional security. It was found that the extreme poor households suffered the most from hunger. In Dhaka, 15 per cent of the respondents reported taking less than three meals a day.

Overall, 38 per cent households in Phase I and 30 per cent households in Phase II reduced food consumption as a negative coping strategy to deal with reduced income.

With regard to post-opening food expenditure, a 25 per cent reduction in per capita daily food expenditure was observed between February and June for the urban sample and a 29 per cent reduction for the rural sample.

In terms of dietary diversity, households reported a significant shortfall of meat, milk, fruits and egg consumption. In fact, 86 per cent and 69 per cent of urban slum households reported never consuming milk and meat in the week prior to the survey. Consumption shortfall for meat was similar in rural households (68 per cent).

COPING REALITIES: The three main types of support mechanisms that vulnerable households turned to during the pandemic are - personal, social and institutional. Most of them resorted to personal coping strategies that include relying on household income, savings, loans, shop credit, consumption reduction, asset sale and remittance.

Phase II of the study reveals that 50 per cent of the urban and 30 per cent of the rural households relied on savings as a coping strategy against the economic shock. Urban households also incurred debt at a higher ratio (36 per cent) than rural households. Moreover, a third of the respondents in both urban and rural samples relied on shop credits. However, as economic activities gradually resumed after April, households relied more on current income for food consumption instead of depleting their savings. In comparison, social and institutional support systems were much less significant means of support.

The survey found that 25 per cent of urban slum residents, 18 per cent of rural households and 24 per cent of households in the CHT region opened a mobile banking account after the lockdown was announced in March to send and receive cash assistance within both formal and informal support networks. This indicates that digital finance can play a pivotal role for the poor and vulnerable people to receive emergency support.

An in-depth look at inelastic non-food expenditure burdens including house rent, utilities, healthcare, and transportation revealed that these have serious implications for the economic recovery of the poor. The biggest non-food expenditure burden is house rent as it is not possible for most urban households to cut down on their rental expenses as they live in rental housings. In most cases, rent in urban slums was not reduced by the house owners and the tenants did not receive any financial assistance to pay rent either. The respondents who live on rental property reported in June 2020 that 65 per cent of them paid rent as before; 26 per cent did not have to pay rent but informed that they would have to pay later.

SOCIAL PROTECTION REALITIES: The survey found some serious gaps in the process realities of the relief mechanism during the Covid-19 crisis. Urban slums had considerably higher coverage compared to rural areas - 62 per cent of urban slums were listed for relief programs as opposed to only 35 per cent of rural households.

Poverty targeting was not quite effective either. Nearly half of the extreme poor and moderate poor households were not listed as beneficiaries. On the contrary, 42 per cent of the non-poor were listed for relief. In terms of actual relief received, 61 per cent of the urban households reported to have received some relief whereas only 22 per cent rural households received support. Mistargeting in relief distribution was again noticeable for non-poor households as 32 per cent of them received support whereas half of the poorest two categories did not. Moreover, the monetary value of the support received was minimal, ranging between BDT 500 to 2000 approximately.

UNPACKING RECOVERY: APRIL TO JUNE 2020: After the re-opening of the economy, economic activity considerably improved in June but did not translate into sufficient recovery in either income or food expenditure. Reported daily per capita income in June was BDT 66.86 in urban slums and BDT 53 in rural areas, which were significantly lower than pre-Covid income at BDT 108 and BDT 95.63 respectively.

On the other hand, per capita daily food expenditure in June was BDT 45 in urban and BDT 37 in rural areas respectively; it was higher at BDT 61 and BDT 52 respectively in February. Daily food expenditure of all the four income groups decreased as well.

Food intake of rural households in June nearly recovered to their February intake level, however, the food intake of urban households in June remained quite below the pre-Covid consumption level. In the case of extreme poor households, 73 per cent of them had three daily meals in April, which increased to 88 per cent in June while the rate was 98 per cent before the pandemic.

MOBILITY TRENDS: The survey found that only 6 per cent households moved from urban to rural areas in April and 13 per cent of the panel sample migrated from one district to another in June. A slightly higher percentage of non-poor migrated to other districts than the other three income groups as migration is expensive and cities have more income generating opportunities for the extreme poor, especially since many of them lack any fallback option in villages. Only 36 per cent of total migrating households were employed in April which increased to 74 per cent in June. This implies that migration was mainly driven by unemployment or lack of income sources and that the migrants experienced significant employment recovery.

To conclude, regression of the vulnerable non-poor to poverty is a major setback for Bangladesh. Their fragile recovery and emerging vulnerabilities must be taken seriously. Some of the other critical policy recommendations of the study include implementing more effectively targeted cash support programme for the 'new poor' and addressing nutritional poverty of the extreme poor. Specific skill and financing support programmes for urban and rural women should be initiated to address the widening gender gap in the labour market. Extending social protection to the urban poor and stimulus packages for small enterprises need to be prioritised as well.

[The report of the Phase II of the "PPRC-BIGD Rapid Response Survey: Livelihoods, Coping and Recovery During COVID-19 Crisis" was launched on October 31, 2020. This article provides a summary of the key findings from the report.]

Sabrina Miti Gain is a Research Associate at PPRC.