Future profitability to drive IPO share pricing under 2025 rules

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The revised public issue rules introduced a new component-future profitability-to determine the value of primary shares, aiming to encourage companies with strong growth prospects to enter the equity market.

The 2025 rules were formulated amid complaints from issuers and issue managers that faulty valuation methods under the previous framework had contributed to the drying up of IPO flows in recent years. While drafting the new rules, regulatory bodies had to ensure sufficient flexibility while simultaneously preventing price distortion.

Profitable companies with good business potential seek a premium during the valuation of their IPO shares. This means that if a company with business as usual is willing to issue shares at Tk 10 against its net asset value of Tk 10, a promising enterprise may not issue shares even at Tk 30 because its productivity is, for example, ten times that of its competitors.

"The new rules are very good. They allow [under the book building method] taking a company's future performance into consideration," said Tanzim Alamgir, founding managing director and CEO of UCB Investment Limited (UCBIL).

According to the revised rules, issue managers, in consultation with issuers, shall determine the indicative prices based on valuations received from eligible investors, derived from their demand during roadshows.

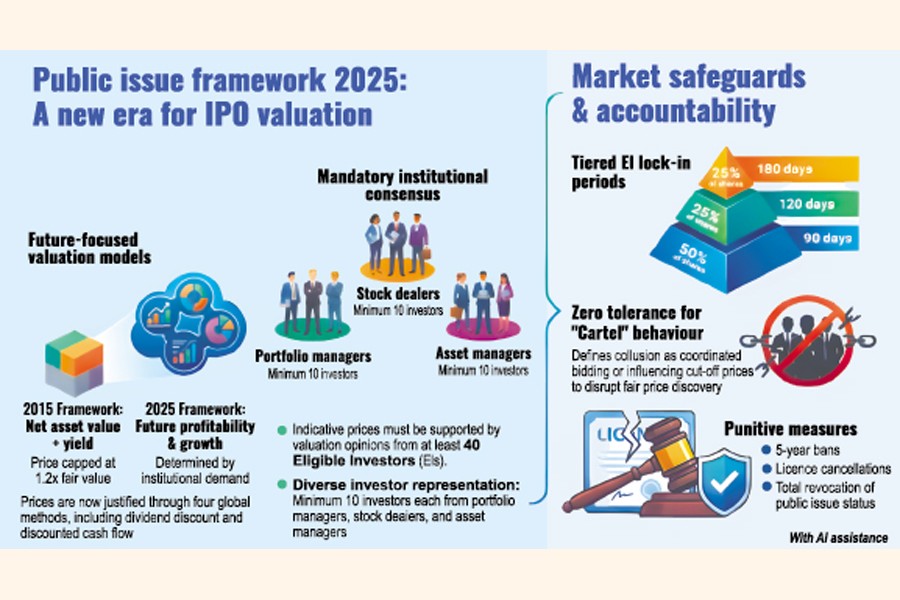

Indicative prices must be supported by valuation opinions from at least 40 eligible investors (EIs), including at least 10 from each of the three categories-portfolio managers, stock dealers, and asset managers.

Indicative prices must be justified through four globally acceptable valuation methods designed to incorporate future earnings into the price determination process. For example, under the dividend discount model (DDM), a company is worth the sum of the present value of all its future dividends, whereas the discounted cash flow model (DCF) states that a company is worth the sum of its discounted future free cash flows (FCFs).

"The current rules have incorporated [valuation] methods widely used around the world. I believe these methods will function well to discover the real price," said Dr. Mahmood Osman Imam, professor of finance and dean of the Faculty of Business Studies at Dhaka University.

The 2015 rules, however, were rigid, formulated after earlier regulations had given rise to manipulation of IPO share prices. Under those rules, companies seeking a premium had to float an IPO under the book-building method, which imposed a ceiling on share prices depending on net asset value and earnings per share.

The fair value of an ordinary share was calculated as the simple average of the values determined by the net asset method and yield method, and bidders were not allowed to bid more than 1.2 times the fair value.

Md Abul Kalam, spokesperson of the Bangladesh Securities and Exchange Commission (BSEC), said that the 2025 rules are market-oriented, with the provision to take opinions from 10 representatives of each group of eligible investors.

Several issue managers, speaking to The FE, said acquiring valuation opinions from 40 EIs would be a difficult task, as many portfolio managers, stock dealers, and asset managers may not have the human resources to produce high-quality valuations for companies planning to list on the bourses.

To prevent price distortion, the rules impose lock-in periods on shares allocated to eligible investors, a provision absent under the 2015 rules. Half of the shares allocated to EIs will be locked in for 90 days. Half of the remaining half will have a lock-in period of 120 days, and the rest will be available for sale in the secondary market 180 days after debut trading.

"The lock-in [periods] will prevent eligible investors from quoting distorted prices," said Dr. Mahmood Osman Imam.

The 2025 rules also include punitive measures against price distortion. They define "cartel or tacit collusion" as coordinated behaviour by issuers, issue managers, underwriters, or investors to disrupt fair price discovery in an IPO. Such behaviour may occur even without formal agreements. Examples include bidders placing similar prices or quantities, submitting bids at the same time, repeatedly influencing cut-off prices across different IPOs, or placing bids inconsistent with reasonable valuation benchmarks.

If the regulator finds that an issuer, issue manager, eligible investor, or bidder has attempted to influence the indicative or cut-off price, it can act on its own or based on a complaint. The regulator may cancel the bids of those involved, bar bidders from participating in the next three IPOs under the book-building method, revoke eligible investor status for up to five years, cancel the public issue if the issuer is involved, or suspend or cancel the licence of the issue manager for up to five years. Individuals responsible may also be banned from capital market activities for five years.

The shift from the 2015 rules to the 2025 rules marks significant progress in how IPO share prices are determined under the book-building method in Bangladesh. The 2025 rules place stronger emphasis on multi-method valuation and broader institutional participation, moving away from simpler auction price discovery and retail pricing concessions that were the hallmark of the 2015 regime.

farhan.fardaus@gmail.com