Listed mutual funds fail to lure investors despite NAV gains

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Mutual funds are trading at heavy discounts on the bourses but still fail to attract investor enthusiasm.

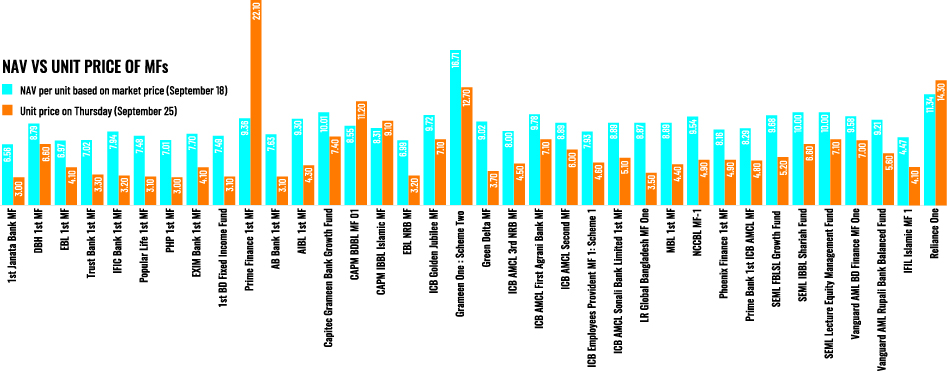

While volatility in the equity market could be a reason that drives away investors, the listed mutual funds have inherent issues that overpower their performance in terms of net asset value. That is why even if NAV has improved in some cases over time, per unit market price of MFs remains remarkably poor.

For example, AIBL 1st Islamic MF has reported NAV of Tk 9.30 per unit on the basis of current market value of assets in its portfolio but its per unit price on the Dhaka bourse was less than half that -- Tk 4.30 -- on Thursday.

The heavily discounted prices are not luring investments into MFs. Instead, the pooled funds have experienced sustained erosion -- between 9 per cent and 23 per cent on the Dhaka Stock Exchange (DSE) during the period of August 3-September 25.

AIBL 1st Islamic MF witnessed a 23 per cent depreciation during the time. Likewise, the market price of Grameen One: Scheme Two declined 12.70 per cent, Phoenix Finance 1st MF fell 10.90 per cent and Vanguard AML BD Finance MF lost 9.69 per cent in market value.

Industry insiders attribute the NAV-market price gap or the disinterest of investors to scams by asset managers, extension of tenures and withdrawal of tax benefits from investments in professionally managed funds.

The extension of tenure is viewed as one of the major reasons behind investors' reluctance to inject funds into closed-end mutual funds. Most listed funds are now scheduled for liquidation between 2030 and 2032, meaning investors have little prospect of realizing their investments with returns in the near future.

Fund managers acknowledge that repeated scams and irregularities in financial reporting have also undermined investor confidence. Investors often cannot gauge the true NAV because of these irregularities, which makes it difficult to assess the value they would eventually receive at liquidation.

The withdrawal of tax benefits on dividends distributed by mutual funds added further pressure. Until 2023, investors enjoyed a tax waiver on dividend income of up to Tk 25,000, a facility that helped attract retail investors. With that advantage gone, mutual funds are struggling to compete with other asset classes.

Market volatility has only compounded the crisis. Since early August, the DSEX index has swung sharply-rising to 5636 points in early September before falling back to 5415 points by September 25. This persistent instability eroded the prices of closed-end funds, which are required to invest at

least 60 per cent of their portfolios in listed equities.

"Volatility in the equity market played a major role behind the erosion in MF prices," said Mahmuda Akhter, chief executive officer of ICB AMCL. She added that funds that maintained proper provisioning still have "breathing space" and could distribute dividends if market conditions stabilize.

At present, 37 mutual funds are listed, and most are trading well below their face value of Tk 10. The failure to distribute dividends in FY24 has further shaken investors' trust, as funds had to keep provisions against losses.

RACE Asset Management, in particular, has drawn criticism for its handling of funds. For instance, First Janata Bank MF reported NAV of Tk 6.56 per unit on September 18, but its market price closed at just Tk 3.0. This fund, along with other RACE-managed funds, is not scheduled for liquidation until at least 2030, leaving investors with limited exit options.

Industry insiders point out that while the scope for offloading units could provide some liquidity, repeated market erosion has already narrowed that option. Instead, the tenure extensions have primarily benefitted fund managers, who continue to collect management fees despite not distributing dividends to unitholders.

mufazzal.fe@gmail.com