Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Well-performing banks offset a year-on-year decline in net interest income in the nine months through September with higher returns from investments in government securities.

Market-based interest rates helped lenders earn more in interest during the period compared to the same period last year, but interest payments to depositors and other lenders also rose for the same reason. As a result, the gap between interest income and interest expenses narrowed.

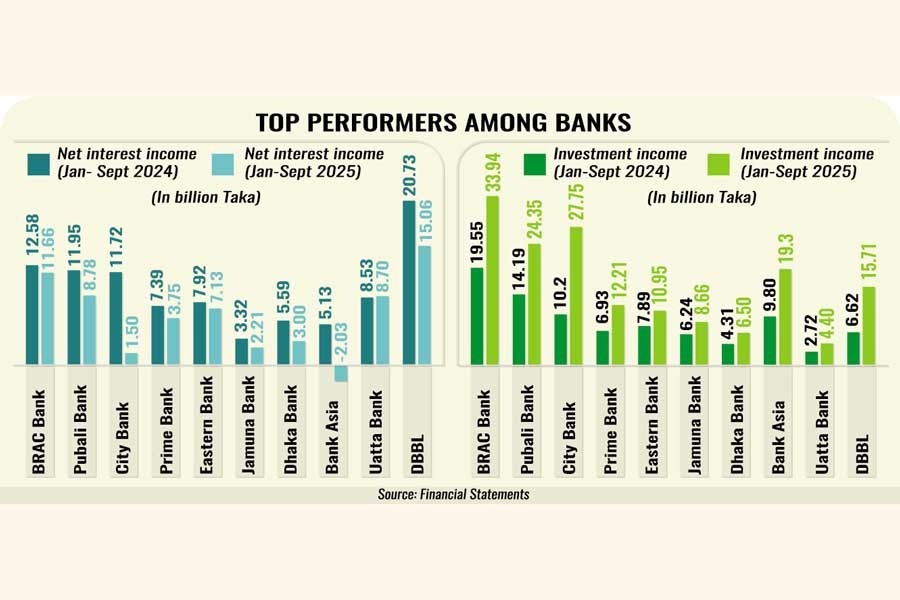

According to financial reports, BRAC Bank, Pubali Bank, City Bank, Prime Bank, Eastern Bank, Jamuna Bank, and Bank Asia earned healthy profits in January-September, supported by their relatively low volumes of bad loans and strong deposits stemming from operating efficiency, good governance, and public trust.

BRAC Bank posted the highest profit of Tk 15.36 billion, followed by Pubali Bank with Tk 9.11 billion, City Bank with Tk 7.22 billion, Prime Bank with Tk 6.14 billion, and Eastern Bank with Tk 5.85 billion for the nine months through September this year.

During the same period, some banks reported huge losses due to poor asset quality and large volumes of bad loans that surfaced after the 2024 political changeover, forcing them to set aside substantial amounts of money for provisions.

Salim Afzal Shawon, head of research at BRAC EPL Stock Brokerage, said that cash-surplus lenders had wisely parked their funds in Treasury bills and bonds, earning handsome returns from those investments.

"As private-sector credit demand remained weak amid persistent economic uncertainties, highly liquid banks preferred to invest their excess funds in risk-free government securities and reaped hefty returns," he said.

Along with interest income from government securities, some lenders also enjoyed capital gains by selling such securities in the secondary market while yields were on the decline.

Investment opportunities have shrunk over the past several months because of the ongoing economic slowdown following the political changeover in August last year.

Private-sector credit growth slowed to 6.35 per cent in August this year from 6.52 per cent a month earlier, reflecting waning business confidence and tighter lending conditions.

"The well-performing banks have always been able to keep operating costs down and mobilize funds at relatively lower costs due to their excellent market reputation, which enabled them to make higher profits," said Akramul Alam, head of research at Royal Capital.

For instance, BRAC Bank reported a record profit of Tk 15.36 billion for the nine months through September this year, supported by substantial investment income.

The earnings surpassed the bank's full-year profit in 2024, as investment income in January-September surged 74 per cent year-on-year, while net interest income dropped 7 per cent during the period.

Bank Asia's net interest income was Tk 2.03 billion in the negative in January-September this year. Still, it secured a profit of Tk 3.51 billion in the same period, as investment income almost doubled to Tk 19.30 billion.

Mr. Alam said trusted banks had also seen a migration of deposits from weaker banks.

"Banks with fewer bad loans could invest more in Treasury bonds. Returns were risk-free, requiring no provisions, which helped secure profit growth," he added.

For example, Eastern Bank's strong focus on asset quality has resulted in one of the lowest non-performing loan ratios - 3.07 per cent at the end of September this year - while the industry average up to June stood at more than 27 per cent.

"Our focus has always been to conduct business prudently within the regulatory framework," said Ali Reza Iftekhar, managing director of Eastern Bank, in a statement on Thursday.

Poor performers

Global Islami Bank, IFIC Bank, and Social Islami Bank recorded substantial losses in January-September this year due to higher provisions and negative net interest margins.

These banks are struggling with poor asset quality, as their real financial picture emerged after the political changeover in 2024.

Due to corrupt lending practices, the banks' huge investments turned toxic, but they could not maintain adequate provisions for the bad loans.

IFIC Bank reported a loss of Tk 18.06 billion in the nine months through September this year, as the bank's net interest income was Tk 16.16 billion in the negative during the period, as opposed to a profit of Tk 700 million in the same period last year.

"If a bank has high bad loans, it cannot earn interest income from those. Moreover, it has to keep provisions for those bad loans from its profit, hurting the bottom line," said Akramul Alam of Royal Capital.

Due to huge bad loans, Global Islami Bank reported a record loss of Tk 22.35 billion for the nine months through September this year, the highest among listed banks, as it had to keep large provisions against bad loans.

The bank had reported a profit of Tk 425 million for the same period last year.

The financial performance of these banks changed so dramatically because the bad loans that the banks had tucked away, taking advantage of the political clout of the previous regime, came to light over the last year.

Global Islami Bank's balance sheet had looked solid, showing no signs of trouble when the bank entered the stock market three years ago by raising Tk 4.25 billion. However, the central bank's tighter non-performing loan policy forced it to reveal its actual position in terms of bad loans, which increased provision requirement.

To discipline the banking sector, politically influenced bank boards - including those of Global Islami Bank and IFIC Bank - were also restructured.

babulfexpress@gmail.com