CONCENTRATION OF AUDIT SERVICES IN BANGLADESH

Insights from top firms and global comparisons

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

An article regarding the Bangladesh audit market has indicated that the top 100 audit firms conduct 87 per cent of audits, i.e., the overwhelming majority of statutory audits, with individual partners at leading firms reportedly signing off on as many as 388 audits per year. At the first glance, these figures may appear concerning to those unfamiliar with the operational realities of audit practice. However, a closer and more informed examination, particularly when viewed in light of global audit market norms, suggests that this phenomenon is neither unusual nor indicative of systemic weakness or regulatory failure. Rather, it reflects the concentration of audit engagements within established firms that possess the necessary expertise, resources, and quality control mechanisms to manage large audit portfolios effectively.

It is also important to note that the article focuses specifically on statutory audits, rather than on tax or regulatory audits. Within Bangladesh's current legal framework, tax audits are not conducted by Chartered Accountant firms as part of the statutory audit regime, and there is no formally recognized category referred to as a "regulatory audit." In exceptional or unusual circumstances, a regulator may appoint a specific auditor to examine a particular matter; however, such appointments should not be interpreted as constituting an established or institutionalized framework of regulatory audits.

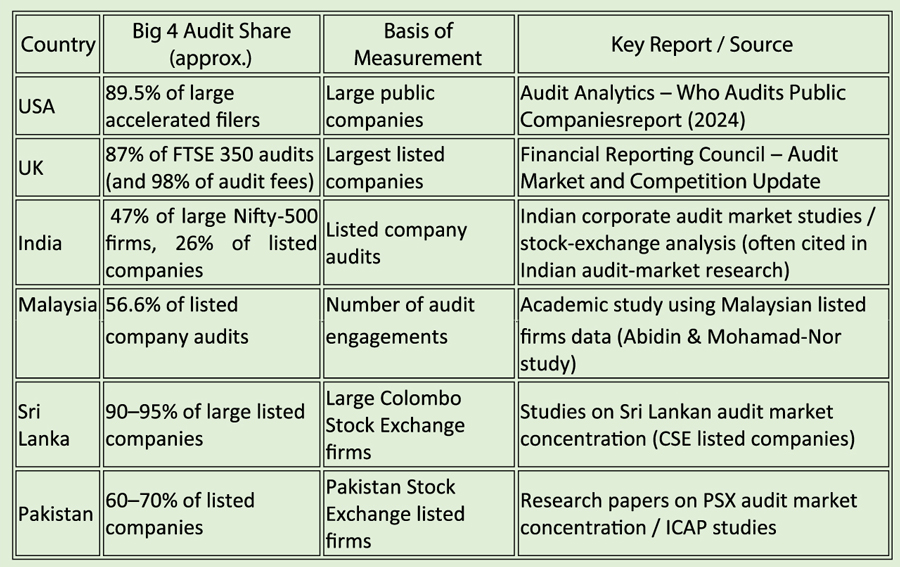

Audit concentration at the top tier is a universal feature of modern audit markets, not a regional anomaly as observed in Bangladesh. In mature markets such as the USA, the UK, and Malaysia, a small cohort of leading audit firms, most notably the Big Four, performs a majority of audits for listed and high-value entities. This concentration reflects a deliberate market alignment: clients with complex financial structures, greater public visibility, or heightened regulatory scrutiny naturally gravitate toward firms with proven capability, deep technical expertise, and established global methodologies. A review of several countries, presented in the table here, further demonstrates the extent to which the Big Four (KPMG, Ernst & Young, PwC, and Deloitte) dominate the audit landscape.

A recent academic study, cited in a PhD thesis in 2020 from the University of Warwick, examined the Bangladeshi audit market and highlighted a significant concentration among the leading firms. Specifically, three of the Big Four--KPMG, Ernst & Young, and Deloitte--maintain offices in Bangladesh, while PwC is absent. Despite their limited presence compared to global presence of them, these three firms account for approximately 16 per cent of audit clients and 33 per cent of total audit fees. Although their share of clients is relatively modest, their proportion of audit fees remains substantial, reflecting the complexity and scale of the clients they serve. In contrast, the remaining 256 firms (out of 258 reported) collectively serve the majority of clients-around 84%-but account for only 67% of total audit fees, as many of these engagements involve smaller organizations with correspondingly lower fees.

Extending the analysis beyond the Big Three to the top 20 local audit firms reveals that these firms also conduct audits of the largest and most complex clients in Bangladesh. This concentration is driven by client demand for quality and expertise, rather than by collusion or anti-competitive behaviour. It reflects a natural, market-based allocation of audit services, where firms with a proven track record and technical capability attract larger clients that require higher levels of assurance.

It is important to note that the audit services in Bangladesh are presently governed strictly by professional ethics and regulatory requirements. Promotional activities to solicit audit clients are prohibited, and auditors are formally appointed at the Annual General Meeting (AGM) of the company under the Companies Act 1994. In practice, listed companies, foreign-invested entities, and large corporations select audit firms based on quality, reputation, and capability, ensuring that the concentration of audits among leading firms is transparent, ethical, and client-driven.

In conclusion, the observed concentration of audits among KPMG, Deloitte, E & Y and the top local firms should not be interpreted as a monopoly or market distortion. Instead, it represents a rational, quality-oriented market structure, consistent with global audit practices, where clients gravitate toward firms that can deliver the highest assurance and technical excellence.

Dipok Kumar Roy FCA is a Fellow Member of ICAB and Partner at Basu Banerjee Nath & Co. CA firm.

dkroy.ca@gmail.com