Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

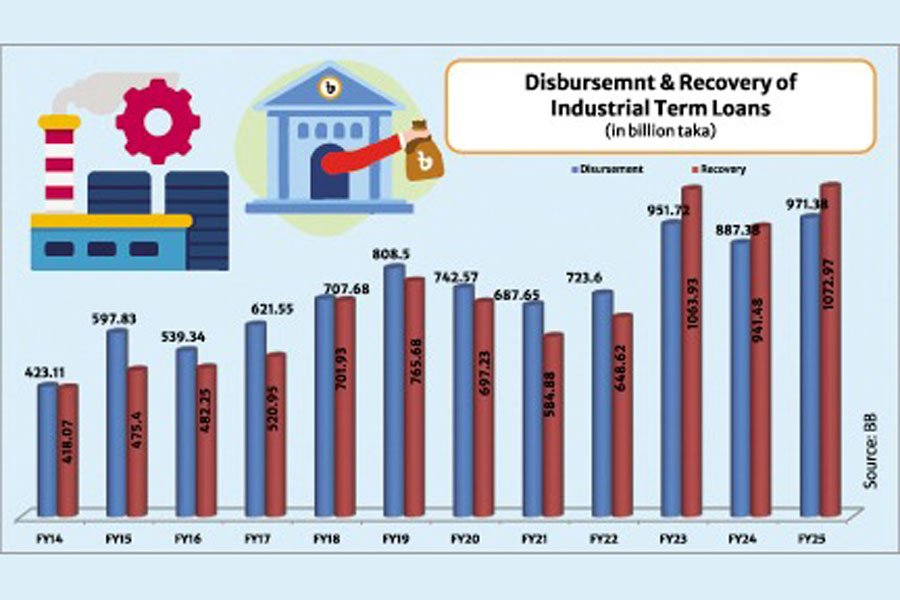

The modest surge in the disbursement of industrial credit in the last fiscal year may be considered as a sign of a rebound in the industrial activities in the country, as well as overall economic growth. Although many other economic indicators are already available, the central bank released the annual figure for industrial term loans only last week. Bangladesh Bank statistics showed that the disbursement of industrial term loan credit increased by around 9.50 per cent in the previous fiscal year (FY25) after a drop of 6.75 per cent in the last fiscal year (FY24). It would be better to tally the credit growth and trend with those indicators to get the big picture. Moreover, focusing on the decade-long trend of the disbursement and recovery of the industrial term loans will also provide some insight into the investment in industrial activities.

Usually, banks and financial institutions provide advances for industrial activities as term loans and working capital financing. At present, shares of these two types of advances are almost equal, with the ratio of term loans slightly higher. In addition to these, financial institutions provide term loans for factoring, though the amount is relatively low. Short, medium, and long-term loans are available for the industry, with more than two-thirds of the total term loans being long-term. Two-fifth or 40 per cent of the total bank advances is disbursed as industrial credit. In other words, 20 per cent of the total bank advances is industrial term loans, and the remaining 20 per cent is working capital financing for the industry. So, the improvement or deterioration of the banking sector's total loan portfolio is significantly dependent on the movement of the industrial credit, underscoring the crucial role of the banking sector in industrial development.

A look at the trend of disbursement and recovery of the industrial term loans for the last decade gives some interesting scenarios. First, the annual average growth of term loan disbursement was 9.0 per cent, whereas the recovery growth rate stood at 10.85 per cent. Second, disbursement of the term loans dropped in four fiscal years between FY15 and FY25. Those were: FY16, FY20, FY21 and FY24. Third, industrial credit disbursement witnessed double-digit growth in five fiscal years during the last decade. Recovery of the term loans declined in three fiscal years, namely FY20, FY21 and FY24. Fifth, recovery of the industrial credit exceeded the disbursement in the last three fiscal years.

There is a fluctuating trend in industrial credit disbursement, which is not abnormal. Due to the COVID-19 pandemic, industrial and manufacturing activities were heavily disrupted. So, the demand for credit also declined during the period, which is widely reflected in the decline in term loans disbursement in FY20 and FY21 by 8.15 per cent and 7.40 per cent, respectively. Recovery of the loans also dropped simultaneously in the same fiscal years, as it was difficult for the manufacturers to repay the loans on time. The pandemic forced many of them to cut down or even shut down their industrial operations. Gross Domestic Product (GDP) of the industry sector posted a moderate 3.61 per cent growth in FY20 after reaching 11.63 per cent in FY19. It, however, rebounded in FY21 by recording 10.30 per cent growth.

Both the disbursement and recovery dropped in FY24 when the controversial 12th parliamentary election took place in the country under the autocratic regime of Sheikh Hasina. Election-centric uncertainty, coupled with post-election dissatisfaction among the masses due to their inability to exercise voting rights, created an unfavourable environment for investment. Though the autocratic regime continued to suppress people's anger by brutal force, it was unable to boost economic activities. Overall GDP growth declined to 4.22 per cent in FY24, whereas the growth of industry GDP also dropped to 6.66 per cent from 8.37 per cent in FY23.

While the double-digit growth in industrial term loan disbursement over the last decade may be interpreted as a sign of robust manufacturing activities and increased investment demand, caution is advised. It's crucial to note that some of these loans were not directed towards productive activities and were misappropriated. Cronies of the Hasina regime reportedly influenced banks to disburse a significant amount of money, a portion of which was neither utilized properly nor returned to the banks. This caution is necessary to ensure a clear understanding of the sector's dynamics.

The decade-long trend also showed that, though the average growth rate of loan recovery is slightly higher than disbursement, actual double-digit growth of recovery was recorded in five fiscal years.

It's intriguing to note that the recovery of industrial term loans exceeded the disbursement in the last three consecutive fiscal years. The recovery crossed the Tk 1 trillion mark in FY23, reaching Tk 1064 billion (or Tk 1.06 trillion) and then dropped to Tk 941.48 billion in FY24. It increased by around 14 per cent to Tk 1073 billion in FY24. This trend raises questions about what drives the higher recovery of term loans, inviting further investigation and analysis.

As mentioned at the beginning of the article, a rise in disbursement and recovery of industrial credit in the FY25 is a development for obvious reasons. Bangladesh Bank statistics showed that the disbursement of industrial term loan credit increased by around 9.50 per cent in the last fiscal year (FY25) after a drop of 6.75 per cent in the previous fiscal year (FY24). The first quarter of the last fiscal year was marked by the student-led mass uprising that finally compelled autocratic Sheikh Hasina to step down and flee to India for shelter on August 5. Industrial activities, along with overall economic activities, were limited in the first quarter of the last fiscal year, but regained slightly in the second quarter and gained moderate momentum in the third and fourth quarters. Thus, demand for credit also increased, which is reflected in the higher disbursement of the term loans.

Nevertheless, when compared with FY23, the disbursed amount of term loans was only 2 per cent higher in the last fiscal year. It means the rise in the industrial credit in the last fiscal year was not as robust as it appeared. Moreover, if adjusted for the inflation rate, the growth of term loan disbursement would be estimated to be negative. The average rate of inflation stood at 10 per cent in the last fiscal year.

Quarterly disaggregation of the term loan disbursement also showed significant fluctuations, as it increased by 40 per cent in the second quarter of FY25, declined by 37 per cent in the third quarter, and finally jumped by 24 per cent in the last quarter. Tight monetary stance kept the interest rate high and increased the borrowing cost in the last fiscal year. Weak law and order discouraged manufacturers from making significant investments and production. International trade uncertainty due to Trump's tariff blitz made things worse. So, under the influence of all the negative internal and external factors, there has been little room for strong growth of industrial activities and, consequently, of credit in the economy.

asjadulk@gmail.com