Realistic assumptions and sound hypotheses are critical for devising policies and setting targets, as they form the basis for subsequent actions and interventions. But the growth targets for GDP and private sector credit incorporated in the recently declared monetary policy of Bangladesh Bank appears to be based on unrealistic assumptions, especially in the backdrop of a surging pandemic that has hit the country's economy severely. The GDP growth rate has been projected to be 7.2 per cent during 2021-22 against an estimated growth rate of only about 5 per cent during the previous year; while the targeted growth rate of private sector credit has been set at 14.8 per cent when this growth rate was only 8.4 per cent during 2019-20. The revised estimate for GDP growth during 2019-20 was 5.24 per cent, but the latest figures released by Bangladesh Bureau of Statistics show it to be only 3.51 per cent. The overall credit growth target in the monetary policy has been set at 17.80 per cent, including 32.60 per cent in the public sector. But many experts have broadly termed these targets as devoid of realism and a blind attempt at continuity.

Let us look at the theoretical context of monetary policy for the sake of general readers. Broadly speaking, it aims to adjust the money supply in an economy for achieving a combination of inflation cum output stabilisation. Usually measured by the gross domestic product (GDP), output remains fixed. Consequently, any variations in money supply cause prices to change. But as prices and wages usually do not adjust immediately in the short run, changes in money supply can influence the actual production of goods and services. It is for this reason that monetary policy is meaningfully applied to achieve both inflation and growth objectives, and the central banks attempt to bring a balance between price and output objectives through this tool. However, it is not the only tool for addressing or managing aggregate output demand. Fiscal policy is another that relies on taxation and government spending for achieving the same objective. However, legislating taxes and making spending changes is a time-consuming affair. Consequently, monetary policy is usually viewed as the first line of defence by governments for stabilising the economy during a downturn like the one we are witnessing in the wake of Covid-19.

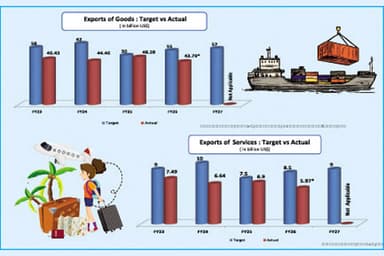

As revealed by an online policy briefing of the think-tank Centre for Policy Dialogue (CPD), the monetary policy targets for GDP growth rate in Bangladesh has come true only once during the previous six years, and that too in normal times free from pandemic. Similarly, the credit growth rate target was achieved only twice during the previous eight years. The supply of credit has to be doubled to reach the target for current fiscal year, but this would be almost impossible during the corona-infected times. Besides, private investment cannot be enhanced merely through credit growth; the investment climate also plays a critical role but that has not seen any improvement in the recent past. The GDP growth rate could have been achieved if there was no pandemic, but recent trends suggest that the situation is unlikely to improve before December. The predictions of low GDP growth made by the World Bank and IMF have consistently supported this view. Besides, the recent declining trend in exports, investments and remittances as well as the worsening balance of payments situation also indicate tough times ahead for Bangladesh economy.

The CPD webinar also pointed out that it is mainly the large entrepreneurs that have benefited from the low-interest rate incentive packages offered by the government, with the small entrepreneurs mostly left high and dry. Almost 80 per cent of the incentives were provided through bank-loans, but the banks are now worried about the timely repayment of that money because of widespread default culture in the country. Besides, questions have also been raised about proper utilisation of the incentive loans. Many opportunistic people can take advantage of the pandemic situation for dodging repayments, and there is nothing in the monetary policy on tackling this issue.

Latest statistics show that there is now excess liquidity in the banking sector. The monetary policy has also acknowledged this reality along with contingency plans for mopping up some surplus from the banks. However, there is need for vigilance and monitoring on whether this excess money is being channelled to the stock market, thereby causing an artificial bubble that can subsequently prove disastrous as seen in the past. There have been credible reports in the media that some of the incentive money is being diverted to the share market, as otherwise no justifiable grounds exist for the recent spike in stock market indices despite a fragile economy upended by the pandemic. The relevant authorities should therefore undertake rigorous investigations to ascertain whether there has been any foul play in the securities market in recent days, and whether a bull's run in share prices is being manipulated for making quick money and windfall gains by schemers and scammers in the market.

As pointed out by CPD, an expansionary monetary policy may also create pressure on the prices of essentials and thereby cause the inflation rate to shoot up. This in turn may cause further distress to the common people who are already bogged down by the pandemic. The pandemic has severely squeezed economic activities in the country, especially in the services sector, leading to losses in employment and income, decline in purchasing power and consumer demand, as well as exacerbated poverty cum inequality situation. Due to expansionary policy and excess liquidity in the banking sector, the assets and property market may also witness a jump in prices leading to price distortions. Overall, the monetary policy appears to be a mere continuation of previous year's policy based on performances during that particular year. There is nothing new about it, nor are there any fresh or novel measures for tackling the current crisis.

Dr Helal Uddin Ahmed is a retired Additional Secretary and former Editor of Bangladesh Quarterly.