Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Who does not aspire after a discrimination-free economy or society? Restoring rights inevitably requires a movement. Since inception of collective right-consciousness , the victims have fought against rights violation. From time to time, agitations spring up spontaneously as we observed an anti-discrimination student movement as one of the most powerful catalysts of July Uprising 2024 led by students and masses in Bangladesh. Discrimination has numerous types and forms -- political, economic, religious, racial, ethnic, gender, administrative, and so on. Many discriminations remain disguised and generally subtle. New and unimaginable forms of discrimination also emerge. However, we should unveil every possible type of discrimination lying in every stage of society and economy. Present discussion would be concerned with a type of economic discriminations particularly in loans and advances disbursed by the banks in Bangladesh.

Discrimination in the field of economic management leads to a rise in economic inequalities. Banks have a critical role in facilitating economic growth in terms of income and wealth of their borrowers. In the context of increasing emphasis upon corporate social responsibility (CSR) , banks as lenders should prioritise the interest of the majority of borrowing people belonging to cottage, micro, small and medium categories rather than large ones. This approach to lending is ethical and beneficial not only for the economy but also for the lending banks.

Disbursement and recovery of loans and advances constitute one of the most important functions of a bank. The cruel fact is that large firms or borrowers managed to reap most of the facilities offered under government stimulus packages during COVID period whereas the people and firms under CMSME categories were deprived of their due and justified benefits. An unholy nexus of bank owners-directors, government policy-makers and the then ruling politicians forced discriminatory banking .

Discrimination is a man-made injustice. It may be created intentionally, unintentionally and also unconsciously. Whatever be the manner of creating or continuing discrimination, it is always unacceptable and subject to elimination. It is also true that eliminating discrimination hardly occurs without a strong movement. Longstanding discrimination often becomes a custom that is silently accepted as a fate . Resistance to change such fate comes from the beneficiary group. Thus it is an ethical as well a great challenge as to whether and how to end discrimination.

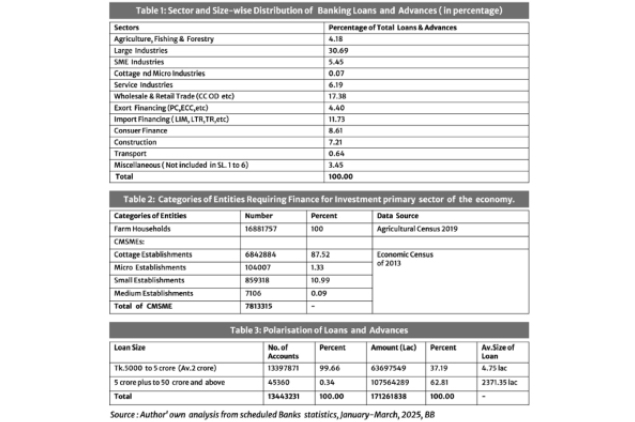

According to information obtained from BB's Scheduled Banks Statistics (January-March 2025), Table 1 reveals that as the primary sector contributing 10.94 per cent of gross domestic product (GDP), agriculture, fishing & forestry receives only 4.18 per cent of total bank loans and advances .This is quite inadequate against the sector's actual requirements. Besides, the share of finance held by farm borrowers of more than Tk 1 crore to 50 crore and above is 1.16 per cent. As a result, the actual percentage for farmers below the loan size of Tk. 5000 to 1 crore reduces to 3.02 (i.e. 4.18 per cent minus 1.16 per cent). Most of the farm households have to depend on informal fund to the extent of more than 90 per cent of their needs at a much higher cost . Borrowers under cottage and SME categories receive only 5.52 per cent of total loans and advances. Available data on banking finance are not well designed. So, the real position of CMSME financing cannot be analysed and justified in specific terms. We are totally unaware of any updated and inclusive statistics on financing CMSMEs along with the number of entrepreneurs/borrowers based on their nature and size. Consequently, categorical financing needs and priorities cannot be ascertained. An attempt has been made to present some past statistics about size-based economic establishments, and farm households which are to be assessed as preferential entities.

This Table furnishes data from which we can guess a rough scenario regarding the number of probable finance-seeking people and organizations that largely belong to CMSME categories. It is seen from the table that more than 78 lac CMSME establishments are recorded. Their actual number might have rather escalated over the time span of 12 years from 2013. Regrettably, we fail to collect the current number of borrowing accounts and other relevant data under CMSME .The number of accounts under agriculture, fishing and forestry are 63.35 lac against 1.69 crore of farm households. Only 37.49 per cent of farm households have been financed with very insignificant amounts.

Table 3 shows that the banking industry has more than 13 million accounts for loans and advances. We cannot directly conclude that the number of borrowers would be exactly equal to the number of accounts. Due to having more than one accounts maintained by many borrowers, the actual number of borrowers may be around 10 million. Whatever be the real number, 99.66 per cent account holders have access to only 37.19 per cent of total loans and advances while only 0.34 per cent account holders share 62.81 per cent of total loans and advances. Economic activities create income and wealth usually to the extent of investment outlay made by the investors. Household Income and Expenditure Surveys 2016 and 2022 reveal that investible surplus of the majority of households is insignificant. That is why, they need debt financing. CMSMEs' inaccessibility to and inadequacy of debt fund is triggered by discriminatory allocation of banks' loans and advances. Awfully it is observed that average size of loans and advances taken by few account holders ( only 45,360) is 499.23 times the average size of borrowing by more than 13.39 million account holders. Are the lending banks liable for such a discrimination ? It is primarily the lack of clear philosophy and principle of good governance at the national level and secondarily the lack of good corporate governance at the level of lending banks.

Hard truth is that we are yet to develop the appropriate framework of good governance to be implemented by the government . Most important at this critical juncture of time is that there must be a broad-based political consensus particularly on the fundamental philosophy and principles that would underpin the foundation of good governance system for our country. As a sub-system, the model of corporate governance in banking will have to be developed. Corporate stakeholder responsibility should be preferred over corporate social responsibility in order to meet expectations of all organic stakeholders of the banking industry. Then, discriminatory banking will end as an in-built component of stakeholders-based banking governance.

Haradhan Sarker, PhD, is ex-Financial Analyst, Sonali Bank & retired Professor of Management.

sarkerh1958@gmail.com