Bangladesh’s journey toward financial inclusion has become a hallmark of development-driven central banking in South Asia. The first part of the article (published on August 23) outlines the progress: developing the inclusive regulatory frameworks, promoting digital financial innovations, and aligning policies with national priorities and global commitments by over the past decade. Last part focuses on a forward-looking agenda to further bridge gaps in access, usage, and quality of financial services—particularly for underserved populations.

Microfinance, Finance Companies (FCs) and others: Microfinance institutions (MFIs) in Bangladesh have been instrumental in bridging the financial access gap left by the formal banking sector, particularly for low-income, rural, underserved and hard-core poor people. Originating from grassroots poverty alleviation efforts in the 1970s, MFIs have matured into an essential pillar of the country’s financial inclusion ecosystem. They offer microcredit, savings products, and socio-economic support programs to millions excluded from traditional banking. Their core emphasis on empowering marginalised communities—especially women—has contributed not only to social inclusion but also to local economic development and intergenerational poverty reduction.

As of December 2024, 724 licensed MFIs were operating across 26,071 branches nationwide, serving over41.56million account holders, with 90 per cent of these clients being women—a testament to their central role in gender-responsive financial inclusion. These institutions held 32.18 million borrowers. MFIs also support income-generating activities across agriculture, livestock, handicrafts, and small trade, enabling rural households to diversify livelihoods and build economic resilience.

The Microcredit Regulatory Authority (MRA), established in 2006, has provided crucial institutional oversight. It has enhanced transparency and accountability through regulatory mechanisms such as the National Microfinance Database, the Depositors’ Safety Fund, and the piloting of a Credit Information Bureau (CIB) for MFIs. These initiatives help protect vulnerable clients and stabilise the sector during economic shocks.

Bangladesh Bank complements MRA’s efforts through strategic policy alignment and integration of MFIs within the broader national financial infrastructure. The central bank promotes synergies between MFIs, banks, and digital financial service (DFS) providers, particularly through agent banking and mobile financial services. By enabling DFS linkages and advocating for interoperability, Bangladesh Bank ensures that even the most remote populations can access financial services through convenient digital platforms.

Moreover, MFIs play a direct role in poverty alleviation by offering access to credit without collateral, supporting income generation, and facilitating asset-building among the poor. Their operations are aligned with the objectives of the National Financial Inclusion Strategy (NFIS) and the Sustainable Development Goals (SDGs), particularly in reducing poverty (SDG 1), reducing inequality (SDG 10) and promoting gender equality (SDG 5). Their ability to respond flexibly to local contexts and provide social intermediation such as financial literacy training, health education, and skill development—further distinguishes their contribution from traditional lenders.

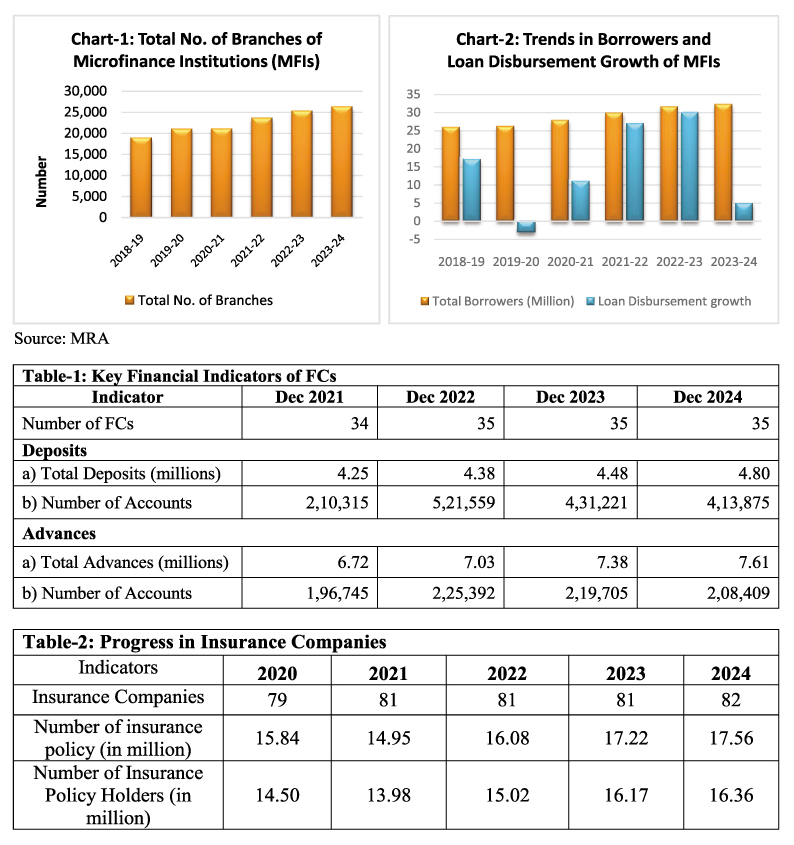

The total number of MFI branches grew from 18,825 in FY2018–19 to 26,071 in FY2023–24, reflecting a 38.5 per cent increase in outreach infrastructure over six years. This upward trend reflects the expanding footprint of Microfinance Institutions (MFIs) in reaching low-income and underserved populations across the country (Chart-1). From FY2019 to FY2024, the total number of microfinance borrowers increased steadily from 25.76 million to 32.17 million, reflecting expanding outreach by Microfinance Institutions (MFIs). Loan disbursement trends, however, show notable year-on-year fluctuations. After a contraction in FY2020 due to the COVID-19 pandemic (-3.16 per cent), the sector rebounded strongly with double-digit growth in FY2021 (10.96 per cent) and FY2022 (26.90 per cent), peaking at 29.92 per cent in FY2023 (Chart-2).This surge highlights the sector’s resilience and its growing importance in supporting livelihoods and microenterprises during recovery periods. However, growth moderated to 4.90 per cent in FY2024, suggesting a possible stabilisation or tighter credit environment.

Financial Companies

Between December 2021 and December 2024, the number of Financial Companies (FCs) increased slightly from 34 to 35. Total deposits grew from Tk 4.25 million in 2021 to Tk 4.80 million in 2024. However, the number of deposit accounts increased significantly from over 2,10,315 to around 413,875. Similarly, total advances increased from Tk 6.72million to Tk 7.61 million over the same period and the number of loan accounts increased from 1,96,745 to 208,409 by 2024.

Insurance Companies

Insurance plays a vital role in financial inclusion by providing a safety net that helps individuals and households manage risks such as illness, accidents, and natural disasters. While often overlooked compared to banking services, insurance enhances financial resilience and enables long-term stability, especially for low-income and vulnerable groups. As part of a broader inclusive financial system, access to insurance complements savings and credit by protecting against shocks that can undermine economic progress.

The data provided covers two key financial sector indicators from 2020 to 2024: Number of insurance companies and Number of Insurance Policy Holders (in millions). Between 2020 and 2024, Bangladesh’s insurance sector experienced modest yet steady growth. The number of insurance companies increased from 79 in 2020 to 82 in 2024, reflecting regulatory stability and gradual market expansion. Over the same period, the number of Insurance Policy Holders under insurance institutions rose from 14.50 million in2020 to 16.36 million in 2024, indicating a renewed interest in insurance-linked financial products. The number of insurance policies in Bangladesh increased from 15.84 million in 2020 to 17.56 million in 2024, reflecting gradual progress in insurance penetration (Table:1). This upward trend in policy numbers, despite slight fluctuations in 2021 due to covid-19 effect signals growing public trust in the insurance sector as a component of the broader financial inclusion framework. The introduction of ‘Bancassurance’ in 2023 gave the sector some momentum which is expected to be continued in coming days.

Financial Literacy

Nationwide Financial Literacy Campaigns To provide tailored financial literacy to target population, especially those who are marginalised and underserved, Bangladesh Bank has issued Financial Literacy Guidelines in 2022. Banks and Finance companies are conducting financial literacy programs country-wide under this guideline. From January 2023 to December 2024 total 461,948 people received financial literacy physically through 6243 programs of which 169,554 were female. Under the guideline, financial institutions are using social media, website extensively to spread financial literacy in the digital sphere especially targeted for young generation and rural people.

Curriculum integration in schools. In collaboration with the Ministry of Education, Ministry of Primary and Mass Education, and the National Curriculum and Textbook Board (NCTB), Bangladesh Bank is embedding financial education into the national curriculum. This strategic move aims to nurture responsible financial behaviour from an early age. Textbooks now include dedicated chapters on financial topics such as money management, financial saving, planning and basic financial decision-making.

Celebrating Financial Literacy Week. Bangladesh Bank has been working with OECD/INFE to spread financial literacy to the youngsters. In line with ‘Global Money Week’ of OECD/ INFE, banks and financial companies in Bangladesh also celebrates ‘Financial Literacy Week’ in March every year.

Promoting Interoperable, Inclusive Payments through Bangla QR. To accelerate digital financial inclusion, Bangladesh Bank introduced the Bangla QR—a universal quick response (QR) code standard that enables interoperable payments across banks, MFS, and PSPs. It simplifies small merchant transactions, supports low-cost acceptance infrastructure, and allows customers to pay using any mobile wallet or banking app.

BB’s Major Policy Interventions: Bangladesh Bank (BB) has implemented a comprehensive suite of policies aimed at enhancing financial inclusion across the country. These policy interventions are aimed to achieve three primary objectives: ensuring access to financial services, promoting their usage, and improving the quality of financial facilities. Below is a detailed narrative of these initiatives, supported by references from BB’s official publications and circulars.

Ensuring Access to Financial Services

Bangladesh Bank has prioritised expanding the reach of financial services to underserved and unbanked populations, particularly in rural and remote areas. Key initiatives include:

(i) Branch and Sub-Branch Expansion; (ii) Agent Banking Guidelines; (iii) Introduction of the electronic Know Your Customer (e-KYC) system; (iv) Mobile Financial Services (MFS); and (v) Digital Banking Initiatives.

Promoting Usage of Financial Services

Beyond access, BB focuses on encouraging the active use of financial services through various programs:

(i) No-Frill Accounts: BB has mandated the provision of basic bank accounts with minimal requirements, known as no-frill accounts, to facilitate banking for low-income individuals. These accounts often require a nominal initial deposit and have no minimum balance requirements, making them accessible to the economically disadvantaged.

(ii) School Banking Accounts: Initiated in 2010 and formalised in 2013, the School Banking program encourages students to open bank accounts, fostering early financial literacy and savings habits. As of March 2025, there are over 4.4 million schools banking accounts, with a significant portion from rural areas.

(iii) Subsidised Credit Programs/Refinance Scheme: BB has introduced subsidized credit schemes or refinances facilities targeting various sectors, including agriculture, SMEs, and women entrepreneurs. These programs offer loans at reduced interest rates, encouraging borrowing for productive purposes.

(iv) Financial Literacy Programs: Recognising the importance of informed financial decision making, BB has implemented various financial literacy initiatives. These include integrating financial education into school curricula and conducting awareness campaigns to educate the public about financial products and services using physical and digital means.

(v) Customer Service and Complaint Management: To protect customer rights and strengthen public trust in the financial sector, Bangladesh Bank introduced a structured Customer Service and Complaint Management framework. The system was formed to promote ethical service standards, enhance transparency, and ensure fair treatment across all banks and financial institutions.

(vi) Dedicated hotline: To enhance consumer protection and expand financial access, especially in rural and underserved areas, Bangladesh Bank launched a dedicated hotline (16236) for inquiries, complaints, and information on financial products and rights. Alongside this, the Bangladesh Financial Intelligence Unit (BFIU) operates hotlines for reporting fraud. Banks and MFS providers also offer 24/7 call centres, with BB encouraging them to include financial literacy and complaint resolution services.

Improving the Quality of Financial Facilities

To ensure that financial services are not only accessible and utilised but also of high quality and of low/no barriers, BB has undertaken several measures:

(i) Financial Literacy Guidelines (FLGs), Issued in March 2022; (ii) Consumer Protection Measures;

(iii) Digital Transformation that includes the adoption of technologies like AI and block-chain to streamline operations and improve customer experiences; (iv) Open Banking Initiatives for secure data sharing among financial institutions and and enhance competition in the financial sector; and (v) Monitoring and Supervision Enhancements ensuring regular monitoring of financial institutions to ensure compliance with regulations and the adoption of best practices.

National Financial Inclusion Strategy (NFIS): Bangladesh’s National Financial Inclusion Strategy (NFIS), launched for the period 2021–2026, serves as the country’s comprehensive roadmap to expand inclusive access to financial services. It outlines 12 strategic goals and 69 measurable targets, covering areas such as digital finance, gender inclusion, rural access, and consumer protection. To ensure effective implementation, the

NFIS Administrative Unit (NAU) was established in 2021 under Bangladesh Bank. As of now, 97 per cent of the NFIS goals have been either fully or partially implemented.

Digital tools like the NFIS Tracker website and the Women’s Financial Inclusion Data (WFID) Dashboard have improved transparency and monitoring, enabling data-driven policymaking.

Overall, the NFIS has significantly accelerated outreach to underserved populations, reduced gender and geographic gaps, and strengthened the foundation for a more inclusive and resilient financial system.

Recent intervention by BB in 2025

(i) CMSME Loan Quota for Women Entrepreneurs: All scheduled banks and financial institutions in Bangladesh must ensure that at least 15 per cent of their total CMSME (Cottage, Micro, Small & Medium Enterprises) loan portfolio is allocated to women entrepreneurs in every year. This quota is part of Bangladesh Bank’s broader strategy to promote inclusive access to finance and to empower women in the CMSME sector. Institutions are required to incorporate this target in their annual business plans and ensure progressive implementation through proper monitoring and reporting mechanisms (BB circular, 17/03/25).

(ii) Mandatory School Engagement through School Banking: As per the circular issued on 16 March 2025, Bangladesh Bank instructed all scheduled banks to ensure that each branch actively engages with at least one nearby educational institution.

(iii) Agent Banking Expansion for Women: Bangladesh Bank instructed scheduled banks to ensure that at least 50 per cent of newly appointed agents under agent banking are women as per circular dated 08 May 2025.

(iv) Revised Refinance Scheme for Marginalized Groups: Banks are required to allocate 25 per cent of total loans under this scheme to women borrowers. The interest rates have been reduced, and the fund size expanded to BDT 7.5 billion. (BB circular: 01/2021, updated in 2025).

Gender-Inclusive Financial Inclusion: Bangladesh Bank has prioritided gender-inclusive financial inclusion as a core component of its national strategy. To close the gender gap in access and usage of financial services, the Bank has implemented several institutional, financial, and policy-based interventions. One major step is the establishment of Women Entrepreneurs Development Units (WEDUs) and Women Entrepreneurs Dedicated Desks (WEDDs) in all banks and financial institutions. These units are designed to support women entrepreneurs through guidance, loan facilitation, and financial literacy.

Bangladesh Bank has also introduced and operationalized the Women’s Financial Inclusion Data (WFID) Dashboard, which provides real-time, sex-disaggregated data to track progress, identify gaps, and guide gender-responsive policy. This dashboard, developed in collaboration with Consumer CentriX and supported by international partners, is the first of its kind in South Asia.

To enhance women’s access to credit, BB mandated that 15 per cent of CMSME loans be allocated to women entrepreneurs by 2029. Additionally, several dedicated refinance schemes have been introduced, including the Tk 30 billion Small Enterprise Refinance Scheme (SERS) for women. Women are also prioritised in COVID-19 recovery refinance schemes, no-frills account initiatives, and credit guarantee facilities. Beyond credit, Bangladesh Bank promotes collateralfree lending of up to Tk 2.5 million for women entrepreneurs and offers incentives for timely loan repayment.

Bangladesh has witnessed steady progress in women’s financial inclusion over the past six years, reflected in both deposit and credit account ownership among female clients in the commercial banking sector. The number of female-owned deposit accounts grew significantly from 33.45 million in 2019 to 55.32 million by 2024. As a share of total deposit accounts in commercial banks, women’s participation rose from 30 per cent in 2019 to 35 per cent by 2024. The growth in female-owned loan accounts was even more pronounced. Between 2019 and 2024, the number of such accounts more than doubled—from 918,480 to over 2.15 million. The share of female-owned loan accounts in total commercial bank loan accounts rose from 8.31 per cent in 2019 to 16.49 per cent by 2024. This nearly twofold increase reflects focused policy efforts to expand women’s access to credit, including collateral-free lending, dedicated refinance schemes, and SME loan quotas mandated by Bangladesh Bank.

Policy Recommendations and Way Forward: To sustain and accelerate progress in financial inclusion, Bangladesh must address persistent barriers related to access, gender gaps, consumer protection, and rural outreach. The following policy recommendations offer a strategic roadmap to build a more inclusive, interoperable, and resilient financial ecosystem. These measures focus on expanding access, reducing digital transaction costs, strengthening regulatory frameworks, and ensuring that underserved groups—particularly women, youth, and rural populations—can fully participate in the formal financial system.

Reduce Cost Barriers to Digital Financial Services (DFS)

(i)Lower internet charges for DFS users through government-regulated pricing tiers or zero-rated financial applications.

(ii) Partner with mobile operators to offer subsidized data bundles for verified financial transactions.

(ii) Promote affordable smartphone schemes (e.g., micro-leasing, smart feature phones) through PPP models to bridge device affordability gaps.

Expand and Modernise Consumer Protection Mechanisms

(i) Fully enforce and revise Bangladesh Bank’s Guidelines on Customer Services and Complaint Management, ensuring uniform complaint cells at all service levels.

(ii) Promote transparent fee structures, fraud alerts, and secure digital authentication practices in collaboration with DFS providers.

Scale Up National Bangla QR for Inclusive Payments

(i) Expand Bangla QR (e.g., KTM) acceptance among small and informal merchants by simplifying registration and offering incentive schemes for QR-based transactions.

(ii) Promote merchant on boarding campaigns in rural markets and local businesses with low setup cost solutions.

(iii) Enable interoperable use of Bangla QR across all banks and wallets, reducing friction and building consumer trust.

Address Gender Gaps in Financial Inclusion

(i) Undertake policy measures to reduce gender-gap in account ownership and ensure sufficient financial products in the market to cater the need of this segment.

(ii) Ensure enforcement of the 15 per cent CMSME loan quota for women entrepreneurs.

(iii) Expand collateral-free lending programs, subsidised credit for women and increase female representation in branch-level advisory and outreach desks (WEDD).

(iv) Partner with NGOs and MFIs to deliver financial literacy and digital on boarding programs tailored for women, especially in rural and conservative areas.

Increase Financial and Digital Literacy

(i) Scale up financial education in schools, integrating practical learning with savings tools like school banking accounts.

(ii) Launch nationwide digital financial literacy campaigns through television, radio, and mobile platforms, targeting youth, women, and first-time users.

(iii) Engage community influencers and local government to address social norms that discourage women’s financial participation.

Improve Accessibility for Rural & Marginalised Populations

(i) Expand agent banking, mobile wallet usage, and subsidised ATM deployment in underserved unions and remote areas.

(ii) Leverage postal and union digital centres as last-mile access points for banking and financial awareness services.

Bridging financial inclusion gap in the SAARC region: By sharing country experiences and data through the SAARCFINANCE network, the SAARC region can transform fragmented efforts into a coordinated, evidence-based strategy—enabling targeted actions and accelerating progress toward inclusive financial access for all.

(i) Bangladesh’s gender gap in financial inclusion remains high at about 20 per cent in account ownership, compared to lower gaps in Nepal and Sri Lanka (World Bank Global Findex 2021). Bangladesh can adapt these approaches to better reach women in rural and urban areas, addressing socio-cultural barriers and boosting women’s access to formal finance.

(ii) Bangladesh’s efforts to implement a national QR code system to unify digital payment methods have faced challenges, leading to slower adoption compared to countries like India and Bhutan. Sharing experiences and best practices from these countries can help Bangladesh enhance its digital payment infrastructure and fully leverage digital financial services to advance financial inclusion.

(iii) Advancing financial literacy and preventing cyber security and and fraud risk in the country from the lesson learned by SAARC countries.

(iv) Ensuring access to credit for marginal and underserved people as well as cottage and micro entrepreneurs by developing common policy framework.

(v) The SAARCFINANCE network’s joint research initiatives and harmonised surveys (modeled after the Global Findex by World Bank) can provide critical, high-quality data that is comparable across countries, revealing nuanced barriers that individual nations alone might overlook.

(vi) Through joint peer learning and experience sharing among central banks via SAARCFINANCE, the SAARC region can unite efforts and accelerate inclusive financial access.

Conclusion: This paper has analysed Bangladesh’s financial inclusion progress from a central banking perspective, highlighting substantial advancements driven by Bangladesh Bank’s proactive policies and the National Financial Inclusion Strategy (NFIS) 2021–2026. Through digital innovation, targeted regulation, and inclusive financial infrastructure, access to formal financial services has expanded significantly, particularly via mobile financial services, agent banking, and no-frill accounts.

Notable gains include increased outreach to rural populations, women, and youth, supported by initiatives such as e-KYC, school banking, and gender-focused credit programs. The use of sexdisaggregated data and financial literacy campaigns has further strengthened inclusion outcomes and accountability.

However, challenges persist. Gaps remain in service usage, digital access, financial capability, and consumer protection—especially among low-income and marginalised groups. Addressing these requires a focus on interoperability, affordability, regulatory innovation, and last-mile delivery mechanisms.

Bangladesh’s experience offers a replicable model for other emerging economies, particularly in South Asia. Continued investment in inclusive digital ecosystems, supported by data-driven policies and cross-sector collaboration, will be essential to ensure financial inclusion translates into long-term economic empowerment and sustainable development.

[Concluded]

Md. Iqbal Mohasin, Director, Financial Inclusion Department; Mohammad Mohidul Islam, Additional Director, Statistics Department; Salahuddin Mahmud, Joint Director, Payment Systems Department; and Saila Sarmin Rapti, Joint Director, Research Department; Bangladesh Bank, Head Office, Dhaka.

[This is the slightly abridged last part of the original paper titled Financial Inclusion and central banking: Bridging the gaps in South Asia. It was presented

as country paper of Bangladesh in 47th SAARCFINANCE Governors’ Group Meeting and Symposium, 26 June 2025. ]