Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

An old controversy was revived of late by some people who argued strongly for the discontinuation of the National Savings Certificate (NSC) scheme run by a department of the Ministry of Finance. There are two aspects to this controversy. The first is whether the NSC should be continued. Economics students will immediately recognise this as a normative issue the answer to which depends on the ethical values, interests and predilections of the individuals. No amount of scientific analysis may resolve any difference of opinions even among rational people. At the collective level this type of questions involving 'should' or 'ought' are often decided by votes in a democratic society. Since the government represents the majority in such a society, the decision is expected to be made by the government. Others are, of course, free to vent their contra views.

The second aspect of the controversy is what the consequences of the NSC in terms of variables of interest are, given that it already exists. This is a positive issue and hence it is amenable to scientific analysis. If the analysis is correct, there will be definite answers to the questions, and rational people should be able to come to an agreement.

The rationale for the NSC and the normative aspect of this controversy are not discussed in this write-up (see 'Why A National Savings Certificate Scheme?', June 02, 2016, The Financial Express, for a discussion). It focuses only on the positive issues to see if the claims made are analytically sustainable. A resolution of the positive issues may help in narrowing the differences of opinions regarding the normative issues.

Recently two op-eds have appeared in local newspapers which have explained in some detail the reasons for the negative views about the NSC. The technical part of their arguments can be summarised as follows: (1) by diverting funds of savers NSC reduces deposits of the commercial banks and (2) its high interest rates force the commercial banks to raise their interest rates. The current liquidity shortage and rising bank interest rates are pointed out as the consequences of NSC.

In order to understand how NSC might impact on bank deposits let us trace the movement of funds through this scheme. Consider a retiree whose pension of Tk4.0 million is deposited in his bank account. He decides to purchase savings certificates from the post office (or any other institution that sells NSC instruments), which offers him a higher interest rate than what he receives from the bank. He writes a cheque/pay order of Tk4.0 million on his bank to pay for the instruments. The post office then deposits this cheque with the account of the government held at Bangladesh Bank. The bank of this NSC subscriber loses Tk4.0 million in deposits when the cheque is settled while the government account gains the same amount. Being a central bank account the latter does not add to any bank deposits, and hence at this point the total bank deposit falls by Tk4.0 million. This is probably what these authors had in mind when they argued that deposits were reduced when people invested in savings certificates.

However, this is only the beginning of the money trail. What happens to the money deposited in the government account? Obviously the government did not borrow the money at this high rate to hold it in a zero interest fund. Since the government runs a large deficit in the budget, it most likely spends the money promptly. It pays for the purchases of goods and services as well as interest on borrowed funds with cheques, which the recipients deposit with their banks. Since the receipts of government revenues and borrowed funds, and the payments for government spending occur continuously throughout the year, we could regard these payments and receipts as more or less instantaneous. That is, the Tk4.0 million that the government had borrowed through savings certificates (and the retiree's bank lost in deposit) is promptly returned to the banking system. Hence, the total deposit of the banking system does not change.

To understand the underlying process more clearly, suppose an individual has a tax liability of Tk4.0 million. He pays the income tax office with a cheque/pay order drawn on his bank. The tax office deposits the cheque in the government account with Bangladesh Bank. At this point the banking system loses Tk4.0 million in deposits and the government account gains the same amount. The government now writes cheques on this deposit to pay for its purchases. These cheques are then deposited with the recipients' banks just as described above. Thus the impact of tax payments on bank deposits is exactly the same as that of the savings certificates. Indeed, all payments to the government will have the same effect. They have no impact on deposits (except conceivably for a very short period), and hence on money supply. The NSC is essentially a fiscal operation with no direct consequences on monetary aggregates.

The second point made by these authors is a bit tricky. Although we speak of the interest rate for ease of exposition, there are actually many interest rates offered by each bank. Deposit interest rates vary from zero on demand deposits to progressively higher rates on time deposits of longer maturities. Loan rates also vary with maturity, purpose of the loan and borrowers' credit ratings. A higher interest rate on one type of deposit or loan does not raise the rates on others to equality because the markets are segregated; although they usually move together. As long as the segregation is feasible the interest differentials can be maintained indefinitely. It may be mentioned that of the 85 million bank accounts in the scheduled banks of the country more than five (5) million are zero interest current accounts and only about four (4) million are high interest fixed accounts (9.0 per cent and 45 per cent of total deposits respectively).

NSC is meant for defined groups of people with ceilings on investment. For example, the Family Savings Certificate scheme is meant for women, disabled and elderly people and the Pension Certificates scheme is for retirees from government, semi-government or autonomous institutions. A Bangladesh Bank study (2013) had found that the elderly and women constituted 47 per cent of the total subscribers of NSS and most of the subscribers of NSC were low and middle-income people. The savings certificates which can be subscribed by any citizen have lower ceilings on investment. In recent years Family and Pensioner Certificates together accounted for about half of the net sale of saving instruments. This reflects the reality that the bulk of the bank deposits cannot be easily converted to NSC deposits.

According to established monetary theory the interest rate in the money market is determined by the demand for and the supply of money. If the savings certificates do not have any impact on the money supply, (and it cannot conceivably affect the demand for money directly), then the interest rate in the money market cannot be affected by the National Savings Certificate scheme.

There could be an indirect effect. When the government spends the money, it will have a multiplier effect on income. The increased income could raise the demand for money and this could push up the bank interest rates if the money market was tight. But this would be the case with all additional government spending regardless of the source of the fund. The same result would also obtain if the pension deposit in the bank was borrowed by private enterprises and spent fully.

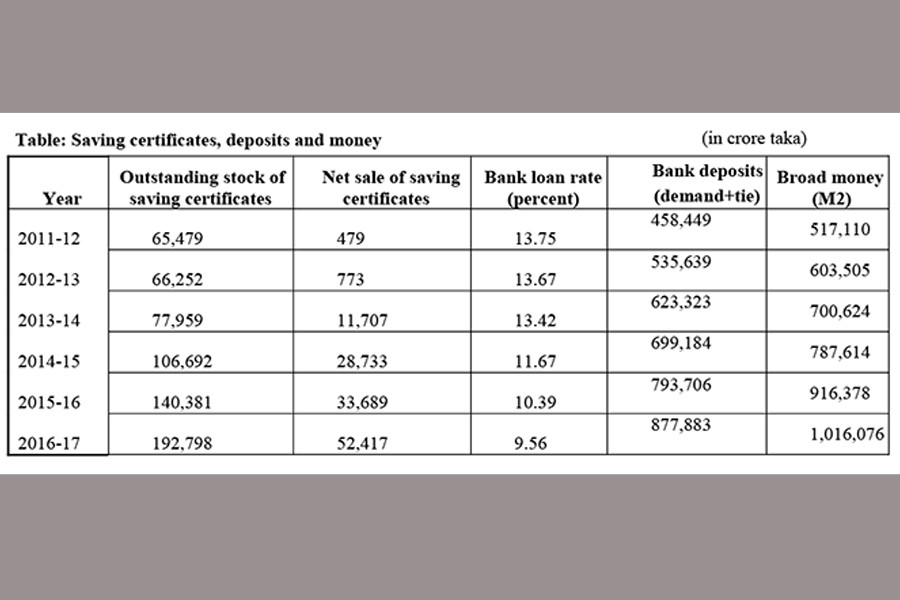

The savings certificates scheme has also been alleged to be responsible for the recent crunch on bank liquidity. This allegation is a bad example of identifying correlation with causation. The net sale of savings certificate instruments massively accelerated since 2012-13 (see Table). Within four years the net sale jumped from a mere 7.73 billion (773 crore) to 524.17 billion (52,417 crore) taka. During the same four-year period the money supply increased by 4,125.71 billion (412,571 crore) taka, a very robust 68 per cent increase. Total bank deposits also increased by 64 per cent during the same time. That the monetary growth was more than adequate is reflected in the nominal interest rate coming down from a high 13.67 per cent to 9.56 per cent. The real interest rate also came down from 5.74 to 4.12 per cent. How were these possible if the massive expansion of the savings certificates had caused an equivalent reduction in monetary (deposit) growth? What does the recent announcement of an increase in the advance-deposit ratio indicate about the assessment of the monetary condition by Bangladesh Bank?

A far more plausible reason for the current liquidity crunch was brought out in a news report (The Financial Express, March 06, 2018). The failure of the infamous Farmers' Bank to honour its deposit commitments and financial scams in several banks unnerved a number of institutions, including public enterprises, sufficiently to prompt them to withdraw their large deposits from private banks, especially those with a reputation. At the same time few of these institutions were keen to deposit the withdrawn or other funds in private banks. This reaction spread the problem to the entire private banking sector. Consequently a number of these banks suffered from liquidity shortages. Loan defaults also compounded their liquidity problem. Aggressive efforts of these private banks to increase deposits in order to meet the loan to deposit ratio led to the increase in the interest rates during the last couple of months. The liquidity problem could be quarantined if the Ministry of Finance and Bangladesh Bank had dealt with it at source.

There are some malpractices in the administration of NSC that allows oversubscription. It also allows ineligible people to take advantage of the scheme. These are often cited as a reason why NSC should be discontinued. This drastic measure solves the proverbial headache problem by cutting off the head. A saner solution would be to take effective measures to reduce or eliminate these malpractices. Such measures are neither difficult to design nor expensive to implement. The most important thing is whether the government is keen to do it.

Since the interest rates on the national savings instruments are higher than the alternative cost of funds, there is a substantial fiscal cost of continuing with this domestic resource mobilisation scheme. The Ministry of Finance has not clearly stated what benefit it gets from this scheme that offsets its considerable cost, or why it prefers it to bank borrowing. But the ministry should not get enmeshed in monetary issues in deciding on what is clearly a fiscal operation. On the Bangladesh Bank side, it has sufficient monetary instruments in its arsenal to increase liquidity if deemed necessary; it does not need to butt into the fiscal space to achieve this end.

M A Taslim is Professor of Department of Economics, University of Dhaka.