Payment Initiation Services: the future of payments in Bangladesh

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The global financial system is undergoing a major transformation due to emerging technology. FinTech 4.0 or the FinTech revolution are popular terms used to describe this transformation. The era of dominant digital finance has begun with the advent of FinTech 4.0. Open banking is the term for the present financial revolution. The vision of Open Banking aligns with the vision of FinTech 4.0, such as real-time payments, cost-effective processing and seamless digital transactions. In addition to removing the obstacles of the traditional financial sector, the concept of open banking has the potential to create a plethora of new options for both businesses and consumers. But how? Basically, open banking is a regulatory framework that allows banks to securely share customer financial data with third-party providers (TPPs) through APIs (Application Programming Interfaces), but only with customer consent. Open banking is popular because it allows customers greater control over their financial data. This results in more financial inclusion, improved competitiveness, and a wider range of cutting-edge services.

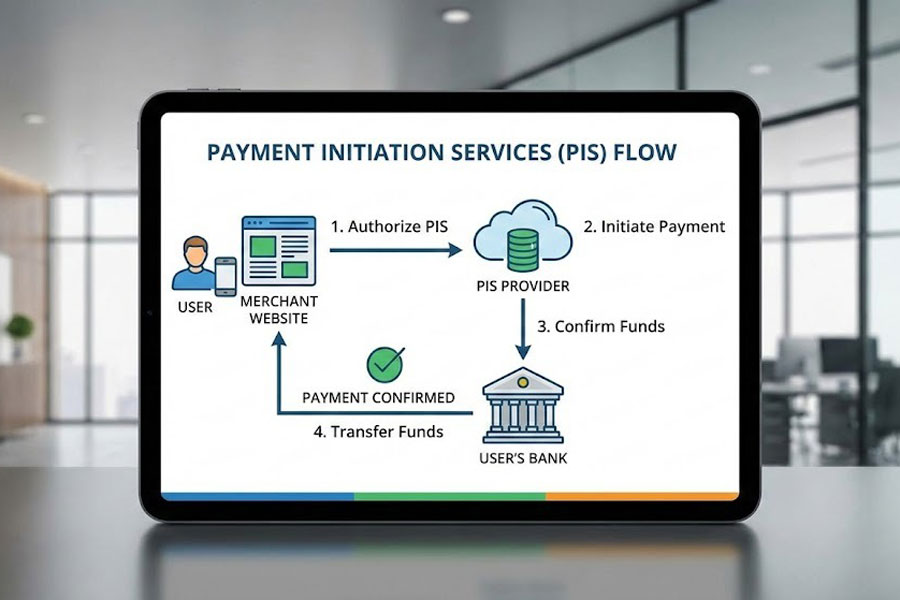

Payment Initiation Services (PIS) are a type of Open Banking service under the European Union’s Revised Payment Services Directive (PSD2) that allow a third-party provider to initiate a payment on a customer’s behalf, directly from their bank account to a merchant. PSD2, the directive behind PIS, also introduced Strong Customer Authentication (SCA) to increase online payment security. Customers can pay companies/businesses simply from their bank accounts via a service called payment initiation, which eliminates the need for credit cards or physical transfers. It operates by PISPs (Payment Initiation Service Providers), who are regulated third parties that securely link to a customer’s bank to start the payment process on their behalf. Traditional payments are largely dependent on card networks and multiple intermediaries. But payment initiation services don’t have to rely on any of those. Payment initiation uses Open Banking APIs to transfer money directly from a customer’s account to a business through PISPs, eliminating the need for multiple intermediaries. As a result, paying is quicker, safer, and more economical.

Advantages of PIS for Customers

Reduced Fees

Open banking payments generally come with lower or no extra expenses for customers. Customers have a more equitable and transparent payment experience when there are no intermediaries or card networks to impose additional fees.

Quicker Settlement

Customers can watch the money leave their account right away because payments are handled in real time. There is no waiting for unresolved charges or ambiguous payment statuses.

Lesser Risk of Fraud

Strong customer authentication (SCA) adds another level of security when customer authorises payments through his own bank. Since there is no need to divulge card information, there is less chance of fraud and scams.

Enhanced Client Experience

Higher conversion rates and fewer abandoned carts result from a quicker and more seamless checkout process. Consumers value the ease of making payments straight from their bank accounts without having to input credit card information.

Advantages of PIS for Businesses

Reduced Transaction Charges

Compared to card networks, fewer middlemen result in cheaper processing costs, saving money on each transaction. These savings can be put back into price plans, customer rewards programmes, or expansion.

Better Cash Flow

Faster access to funds is ensured by real-time bank transfers, which also improve liquidity and decrease settlement times. Improved financial planning and more efficient daily operations are supported by quicker access to revenue.

Higher Rates of Conversion

Customers are more likely to finish their purchases when the checkout process is quicker and more seamless. Customers are kept interested throughout the payment process with fewer clicks and distractions at the checkout.

Reaching Out to New Markets

International clients can make safe payments with open banking without using card infrastructure. It makes direct bank payments more accessible to new markets and clientele.

Bangladesh Bank has already published the draft of PSO Regulation, 2025. Some of the important activities for PISP mentioned in the draft are as follows:

• The PSO providing payment initiation services shall be a member of the Interoperable Platform(s).

• Facilitate e-commerce transactions and merchant payments by starting account-to-account transfers on the user’s behalf without ever keeping their money.

• Start periodic or recurrent credit transfers with the user’s explicit and ongoing consent.

• A PISP is not permitted to operate as an escrow or settlement intermediary or to keep, manage, or otherwise take custody of user funds.

Bangladesh Bank has already initiated payment initiation services which are an important service of the open banking system. Bangladesh Bank is also planning to introduce an open banking system by June 2026. If implemented, it will create new opportunities for payments in Bangladesh, driven by continued growth in digitalisation.

The writer is a Banker and Certified Digital Finance Practitioner (CDFP).

ahabib46@gmail.com