Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Subjecting willful loan defaulters to rigorous actions for loan recovery is fully justifiable from bankers' viewpoint. The central bank issued a circular ( BRPD circular no.:6 dated 12.03.2024) instructing all scheduled banks to identify willful loan defaulters, and report their list as well as take actions against finally identified willful defaulters. The pivotal question is: who are willful defaulters of bank loans in spite of having financial ability? Present discussion aims to shed light upon the fuzzy facets of identifying that type of willful defaulters. The issue merits serious consideration as it is concerned with the legal battles against the loan defaulters.

Quoting the clause 5KAKAKAKA of The Bank-Company (Amended upto 2023) Act,1991, the said circular defined 'willful loan defaulter'. A willful loan defaulter is here defined briefly as a borrowing person or an institution or a company that (i) does not repay bank's loan dues despite financial ability; or (ii) takes any financial benefit from any bank, company or financial institution in own name or in others' name by resorting to fraud, forgery, or misrepresentation; or (iii) takes any financial benefit from any bank, company, or financial institution and engages in fund diversion ; or (iv) transfers to others any collateral without prior written permission of the lending institution. The serial numbers i to iv used here for categorisation of willful defaulters may also be referred to later in this article.

IDENTIFYING WILLFUL DEFAULTERS: As defined in the Bank-Company Act, it is very easy to identify the willful defaulters (serials ii to iv) since documentary evidence can be available or it is possible to obtain proof, and examining diversion of fund is also possible through investigation. Bank personnel's sincere and inquisitive efforts are enough to detect the said categories of willful defaulters. But it is very difficult to identify the willful defaulters as described in serial (i). In this case , the fact is that a borrower is financially able to repay but reluctant to repayment of bank dues. Bangladesh Bank's circular provides the same procedures to be followed in identifying willful defaulters, and finalising their list regardless of the categories of willful defaulters as per the Bank-Company Act (amended),1991. It is most likely that the defaulters identified as being financially able but unwilling to repay would try to prove their inability to repay bank dues on account of incurring losses in business, or poor business yielding no profit or meagre profit, or any other adverse business condition.

Would the lending bank unconditionally take it for granted that the borrowers are financially able but not willing to repay? If so , the lending bank should neither say anything about repayment ability nor describe these defaulters as being financially able but unwilling to repay because the onus would be on the lender to prove borrowers' financial ability (which is really difficult and a great dilemma). Defaulters in serial (i) may rather be classified as habitual defaulters.

PROBLEMS IN PROVING REPAYMENT ABILITY: While appraising loan proposal, it is easy to analyse and judge a borrower' financial ability to repay on the basis of submitted loan proposal, supporting documents and information. It is virtually a theoretical finding . Actual position is determined by borrower's loan utilisation performance and ethical responsibility as well as behaviour. At the time of loan recovery, repayment ability cannot be judged easily owing to lack of obtaining reliable data from the borrower. There is greater possibility that the borrowers would provide the data and information which are more favourable to them. Then how would the lending bank react ? The bank may disagree with the borrowers' data and information or views. What would be the basis of the bank's disagreement ? Since effective supervision and monitoring of borrowers' loan utilisation and operational performance are not carried out comprehensively and regularly, the banks are not in a position to respond irrefutably. So, not to raise borrowers' ability during recovery efforts is wise for the lender as it is the repayers' own issue, almost in all cases.

WHAT APPROACH CAN A LENDING BANK PURSUE: One approach is that the bank would give loans and wait for repayment as per schedule. If borrowers fail to repay as stipulated or do not communicate with the bank, or the borrowers express their financial inability to repay on schedule, or some of the borrowers request for rescheduling, or remain unresponsive, the bank would take necessary actions as per law and regulations. But in that case, laws are still weak for the bank. Rescheduling should be highly selective, and based on hard criteria and real business condition.

The second approach is that the bank would consider repayment capacity and based on that identify willful or other categories of borrowers. If borrowers are given opportunity to explain reasons of, or give arguments against being classified as willful, their replies may or may not satisfy the bank, or they may remain unresponsive despite the passage of a reasonable period of time. How would the bank disregard borrowers' arguments for their financial inability ? Silent behaviour in spite of a few reminders would force the bank to take legal actions. Dealing with borrowers' expression of financial inability is very difficult. Refusing or recognising the borrowers' financial incapacity must be based upon sufficient and reliable information backed by the bank's regular monitoring of loan utilisation performance and operations of the borrowers. In these days of digital technology, it is possible to monitor accounts, transactions, and performance of borrowers' proper use of fund taken from the bank. If the banks are administering their credit programmes in such a manner, then the banks can try following the second approach. In the absence of such regular and continuous monitoring and supervision system, the second approach would not safeguard banks' interest. However, this approach should be used in case of loan recovery from distressed poor borrowers such as landless, small and marginal farmers, cottage, micro and small entrepreneurs, and so on.

In pursuing the first approach , banks can resort to macro data to gauge the business condition to justify borrowers' defensive views based on business depression for which, they argue, loan repayment cannot not be made or is thus delayed.

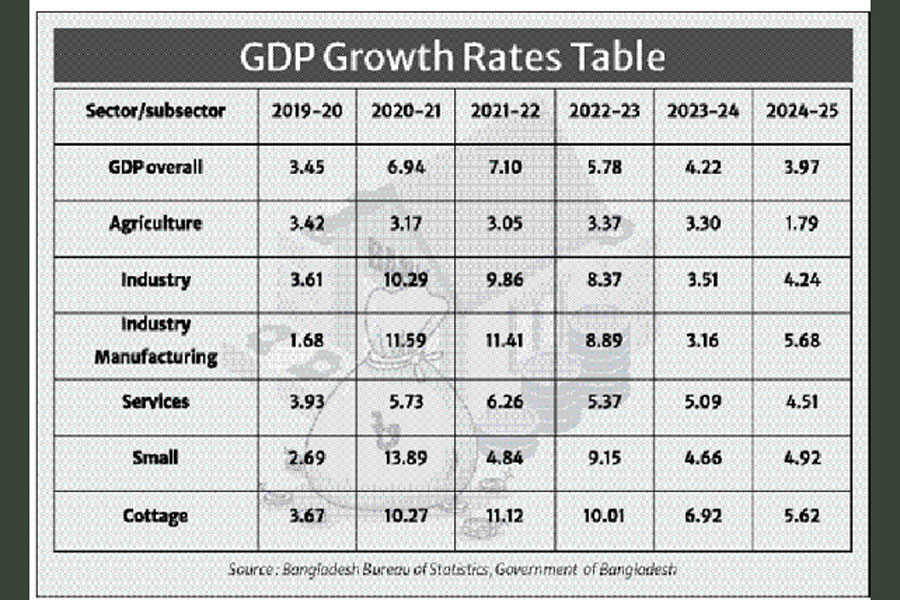

Trends in GDP growth rates may be considered as indicators of fluctuations in business condition. Let us look at GDP growth rates Table.

Regarding GDP data, it may be stated that overall GDP is constantly growing but growth rate is on the decrease. Negative growth rates indicate decrease in production and the data presented here show no negative trends of GDP growth. Sectoral analysis reveals that over the last five years, industry and services grew at a decreasing rate. Borrowers of these sectors cannot argue that they experienced fall in production and income. The same applies to small and cottage industry. This macro scenario hints that borrowers' repayment capacity or ability had not decreased as a whole , rather grew at a deceasing rate. The Non-performing loan ( NPL) ratio of 36 per cent is not compatible with the trends of GDP growth rates . Repayment inability may prevail in a very limited scale but is not applicable to all defaulters.

The path to winning the legal battles against the loan defaulters is thorny and challenging. Every step towards quickening the process of recovering bank loans ought to be taken with utmost caution and competence. Hence, the lending banks must be well equipped with strong instruments (i.e., strong laws free of any loopholes, sound knowledge on related concepts, and commitment etc.)

Haradhan Sarker, PhD, is ex-Financial Analyst, Sonali Bank & retired Professor of Management. sarkerh1958@gmail.com