Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Customs valuation for the purpose of trade taxation remains a perennial problem, causes clearance delays, and is the “biggest” source of disputes and malfeasance at the ports. The current arbitrary customs valuation practice in Bangladesh must be terminated as soon as possible and move to World Trade Organization (WTO)-compliant customs valuation (WTO, GATT 1994), where” transaction value” is the primary basis for import taxation. This can only have improved revenue consequences, as the current practice gives scope for enormous leakage and has not proven to be an effective business-friendly mechanism. Resolving the valuation problem must be given highest priority.

The Policy Approach: Bangladesh, a signatory to WTO Customs Valuation Agreement, is known to work with exceptions to the standard rules for a significant portion of import transactions. High tariffs create the incentive to under-invoice import cargo to evade or minimize tax burden. ASYCUDA, the UNCTAD customs package, launched in 1994, remains under-utilized while automated clearance of import-export cargo is superseded by manual processing of files for all the 30 years of ASYCUDA operation. Risk-based post-clearance audit (PCA) has not been made effective to this day.

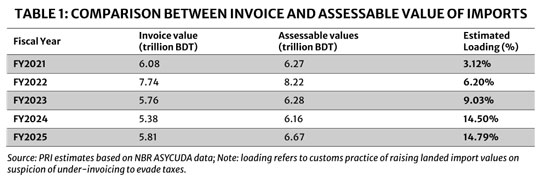

The approach taken by NBR/Customs is to presume that most valuation declarations are under-invoiced. So the only way to ensure proper revenue collection is to “upload” all or most valuation declaration. This practice has, regrettably, become more entrenched in customs processing. As a consequence, assessable import values have been diverging from invoice values over time (Table 1).

What the table reveals is that, overall, import values have been raised by up to 15 per cent particularly in the past two years, implying that all tariffs were also up by 15 per cent, over the fact that since mid-2022, the exchange rate depreciated over 30 per cent (lifting up tariffs as well). There was hardly any impact on revenues despite real increases in tariffs, while imports slowed dramatically undermining export performance. Together, these various factors drove up inflation to over double digits in those years. Such ad hoc measures must be shunned in future.

The way forward: Strategic Objective. Align Bangladesh’s customs valuation regime fully with the WTO Customs Valuation Agreement (CVA) by shifting from discretionary front-end price controls to a modern system built on transaction value, risk intelligence, and post-clearance audit (PCA)—the global best-practice trio used in Vietnam, EU, Morocco, Rwanda, and Chile.

The ASYCUDA Solution. In 1994, Bangladesh Customs launched ASYCUDA, which stands for Automated System of Customs Data. This UNCTAD prepared customs software has been upgraded over time to the latest ASYCUDA World, which Bangladesh currently operates. Whereas this package was introduced with the ultimate objective of making customs clearance of export-import cargo fully automated, to this day (after 32 years), customs clearance is only partially automated. It is the valuation system (the golden goose for customs malfeasance) that remains captive to manual processing. Notice the piles of files on the table of customs officials awaiting clearance. It could be HS code related classification or tariff dispute and so on. At bottom, it is the high and complex tariffs that create enormous incentive to mis declare valuation.

How Bangladesh Customs can use ASYCUDA World and linked intelligence tools—without creating a valuation database.

1. Core Principle: ASYCUDA already provides everything needed for valuation risk analysis; Bangladesh should use it as intelligence, not as reference pricing.

ASYCUDA World integrates three layers of data that make separate valuation databases redundant:

a) National historical declarations (by HS code, importer, supplier, shipment characteristics).

b) Regional and global UNCTAD/World Customs Organization (WCO) commodity intelligence (price ranges, unusual trade patterns, fraud typologies).

c) Risk management modules that assign risk scores automatically based on deviation from norms, transaction patterns, profile history, etc.

None of these tools is meant to replace the transaction value under Article 1 of the WTO Customs Valuation Agreement. All are for risk detection—not duty assessment.

2. Four concrete ways Bangladesh can use ASYCUDA effectively avoiding a valuation database

a) Use ASYCUDA’s built-in “Price Band” Analytics for risk flags, not as minimum values

b) Integrate ASYCUDA’s risk engine with WCO CEN, UNCTAD trade data

c) Use ASYCUDA’s Post-Clearance Audit (PCA) module to enforce valuation through audits

d) Use ASYCUDA’s “Valuation Notes” for internal intelligence—never as fixed values

3. Why Bangladesh does not need a valuation database (and why it is dangerous)

A valuation database creates five systemic risks:

1. Violates Article 1 of WTO CVA by substituting transaction value with arbitrary reference prices.

2. Encourages corruption (“price manipulation” becomes the currency of rent-seeking).

3. Traps Bangladesh in disputes with traders and reduces voluntary compliance.

4. Slows clearance, worsening LDC graduation–era trade competitiveness.

5. Locks Customs into outdated price charts, even though global prices change weekly.

Modern customs administrations do not maintain valuation databases

European Union (EU), United Kingdom (UK), United States (US), Singapore, Morocco, Rwanda, Chile all rely on: (a) Transaction value, (b) Risk profiling. (c) Big-data analytics, and (d) PCA enforcement. They all use risk intelligence lists that are non-binding and cannot replace transaction value.

Bangladesh should move toward this model, but with strategic need for technical assistance in this regard.

ASYCUDA World already provides all required valuation intelligence—global price ranges, transaction histories, abnormal patterns, risk scores—so Customs can target high-risk consignments without violating WTO rules.

The solution is a rules-based valuation system built on three pillars:

1. Accept the invoice price unless there is objective doubt (WTO Customs Valuation Agreement, Article 1).

2. Use ASYCUDA intelligence (price bands, risk flags) only to target risk, not to set prices.

3. Enforce through post-clearance audit, not at the border.

This approach protects revenue, removes discretion, reduces corruption, and accelerates clearance—exactly what Bangladesh needs in the LDC graduation era.

Recommendation and Key Policy Message for Bangladesh:None of South Asia or ASEAN’s major customs administrations maintain a valuation database for duty assessment.

All rely on transaction value + risk intelligence + post-clearance audit.

The choice is clear. Bangladesh should follow the Vietnam model:

• Use ASYCUDA World’s price analytics only to flag risk.

• Avoid fixed price charts (highly vulnerable to corruption).

• Strengthen PCA and intelligence-led risk management.

Dr. Zaidi Sattar is Chairman, Policy Research Institute of Bangladesh (PRI). zaidisattar@gmail.com

[This article is extracted from the author’s contribution to Chapter 4 of the Report of the National Task Force on Tax Reforms (2026), titled “Tax Policy for Development: A Reform Agenda for Restructuring the Tax System. Competent research support was provided by PRI Sr. Research Associates, Karisa Musrat, Hassan Al Banna and Md. Ahad al Azad Munem.]