Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

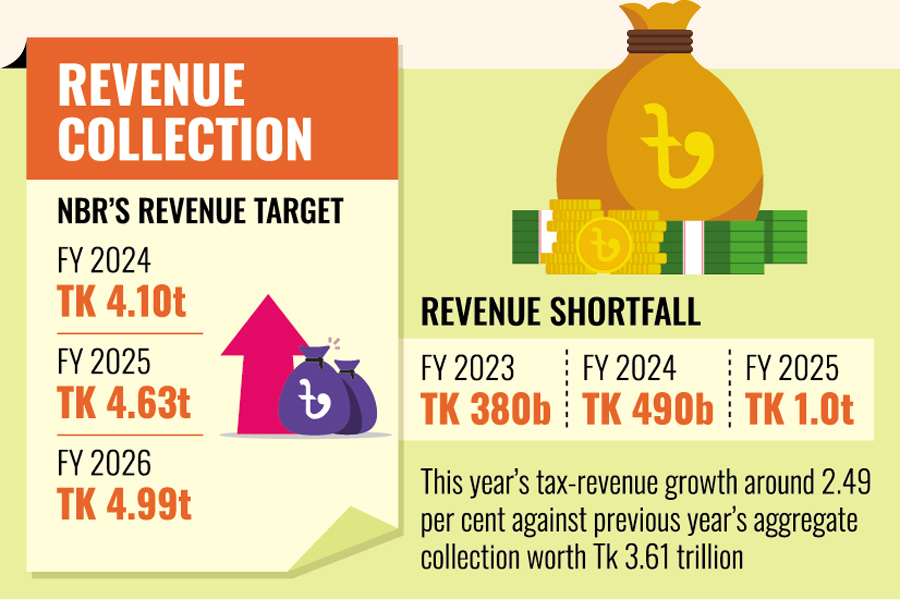

Albert Einstein once remarked that insanity is doing the same thing over and over again but expecting different results. That very cycle of repetition is playing out in the way revenue is being collected to finance the national budget. In the proposed budget for the 2025-26 fiscal year, the government has set an ambitious revenue target of Tk 5.64 trillion, with Tk 4.99 trillion expected to come from the National Board of Revenue (NBR). Few believe the NBR will be able to meet this target given its track record. Economists have said so. Observers have said so. Even NBR officials themselves have admitted as much. How could the outcome be any different when the same institution collected only Tk 3.82 trillion in FY 2023-24 and Tk 3.25 trillion the year before using the same old and exhausted methods! Even in the current fiscal year, projections suggest the deficit may exceed Tk 1 trillion.

If this were a time of political and economic stability, the target set for the NBR in the proposed budget would still have been difficult to achieve due to the existing tax structure and outdated collection mechanisms. But the current situation is far from stable. The country is in the midst of a transitional phase. Economic activity has slowed following the fall of the previous authoritarian regime, the investment climate remains subdued and law and order have yet to be fully restored. Worsening matters further is the internal turmoil within the tax administration itself. A section of customs and tax officials who had earlier protested the government's ordinance to restructure the NBR continues to demand the removal of the NBR chairman. This persistent internal discontent has created a tense and unproductive environment within the tax machinery. In such a volatile environment, it becomes even more difficult to imagine how the government can come close to meeting its ambitious revenue target.

Part of the rationale behind setting such a high target lies in Bangladesh's tax-to-GDP ratio, which, according to the finance adviser's budget speech, stands at a modest 09 per cent. By international standards, this figure is indeed low. India's tax-GDP ratio, for example, hovers around 20 per cent. Nepal's exceeds 25 per cent. These comparisons are often invoked to justify ambitious tax targets. However, the case of Bangladesh is complicated by serious doubts surrounding the accuracy of its GDP figures. According to many experts, key economic indicators including GDP have been significantly overstated. The previous fascist government for various political and economic motives routinely disseminated inflated data. For instance, a 2022 World Bank report estimated Bangladesh's average growth rate between 2009 and 2019 to be 4.2 per cent, whereas official government figures claimed it was 07 per cent. These inflated numbers including the uncorrected GDP estimates continue to distort the real picture. Such exaggerations may be one reason why revenue collection appears to fall short, because the denominator itself is artificially high. Consequently, while the official target appears 9 per cent, the actual effective rate may be 11 or 12 per cent, placing undue strain on businesses and individuals.

Faced with persistent revenue shortfalls, the government has opted to increase the tax burden rather than expanding the tax base as a way to boost income tax revenues. One such measure is the hike in the turnover tax. Under the new budget, companies and firms with an annual turnover of Tk 50 lakh or more, and individuals with a turnover of Tk 04 crore or more, will be required to pay a minimum turnover tax of one percent. Last year, this rate stood at 0.6 percent. This policy is deeply problematic. By its nature, turnover tax does not distinguish between profitable businesses and those operating at a loss. Even companies incurring losses must pay this tax, which is non-refundable as a minimum tax. In effect, this penalises struggling businesses. If a business generates no income, how can it be justified to impose an income tax? This tactic of taxing what is easy rather than what is equitable is fast becoming the norm for the government policymakers. Their response to revenue shortfalls is to mechanically raise the turnover tax, with little regard for fairness or the adverse impact on businesses and the broader economy. This method may yield immediate results but obviously does not serve the long-term objective of building a sustainable and just tax regime.

Slow progress in tax collection in Bangladesh stems from widespread tax evasion, not from insufficient turnover tax rates. There are individuals and businesses who, despite substantial earnings, continue to avoid taxes either by not disclosing their assets or by underreporting income. Detecting such evasions is challenging but possible. Digitalisation and systematic data-sharing are essential prerequisites for success in this regard. Currently, the Bangladesh Road Transport Authority (BRTA) and the Dhaka Power Distribution Company (DPDC) share their data with the NBR. This collaboration needs to expand. The more such collaboration and integration occur between NBR and other public and private institutions, the more effectively tax authorities can identify evaders.

A number of institutions and companies hold valuable client and consumer data that could significantly enhance tax intelligence. For example, access to utility service databases could help the NBR estimate property ownership, rental income and living standards. Similarly, access to regular banking data would be a game-changer. Banks serve as repositories of information on deposits, loans, foreign transactions and expenditures, all of which can help provide an accurate picture of an individual's or a company's financial situation. There is no doubt that establishing such a data-sharing system might have been difficult under a partisan government. But with an interim government now in power, one that is better positioned to withstand political pressures that typically obstruct such reforms, this is an opportune moment to push for its implementation.

There can be no doubt that absence of solid information provides cover for tax evasion. Until NBR closes this information gap, tax dodgers will continue to slip through the cracks and revenue collection targets would continue to remain unmet.

shoeb434@gmail.com