Bangladesh budget reinforces broadly steady fiscal prospects: Fitch Ratings

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The Bangladesh government’s projection that the budget deficit will remain broadly stable in the next fiscal year, 2023-24, could be vulnerable if growth undershoots the authorities’ relatively optimistic target, Fitch Ratings says in a new report.

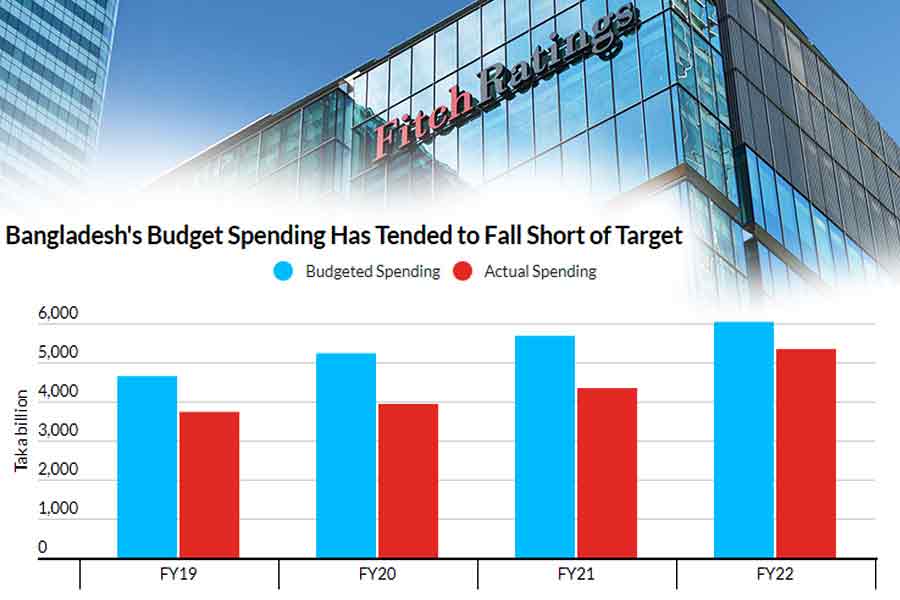

“Bangladesh’s fiscal outcomes have often diverged significantly from budget forecasts, with persistent under-spending against targets. Revised figures for FY23 point to a budget deficit target equivalent to 5.1 per cent of GDP, compared with an original target of 5.5 per cent and Fitch’s most recent projection of 5.7 per cent,” the US-based credit rating agency said in the report published on Tuesday.

“This reflected weaker-than-expected spending on development, but also outperformance on revenue collection. These effects more than offset the impact of additional subsidy spending, which rose to 2.2 per cent of GDP against the original budget target of 1.8 per cent amid high global prices for fertilizer, fuel and natural gas,” the agency said.

“The government’s budget presentation on June 1 forecasts the deficit to widen marginally to 5.2 per cent of GDP in FY24. This is close to Fitch’s current forecast of 5.3 per cent, though our projection was predicated on a significantly wider deficit in FY23.”

“The official forecasts remain broadly consistent with the IMF’s projections under Bangladesh’s Extended Credit Facility (ECF) and the Extended Fund Facility (EFF) arrangements, which see the deficit stabilising at around 5 per cent of GDP over the medium term.”

“Risks to the deficit could increase if real GDP growth falls below the authorities’ projection of 7.5 per cent in FY24, which could dampen the projected nominal growth in revenue of 15.5 per cent. We expect slightly slower economic growth of 6.5 per cent, but consumer price inflation - at 10 per cent yoy in May - is high and still rising, which may point to downside risks.”

“If spending growth falls short of policymakers’ forecasts, as it has done in the past, this could offset potential revenue underperformance or offer enhanced prospects for narrowing of the fiscal deficit if revenue growth meets or exceeds targets.”

“The government’s medium-term policy approach is anchored by the goal of keeping the primary fiscal deficit, including grants, within around 3.3 per cent of GDP to keep public debt below 45 per cent of GDP.”

“The budget projects Bangladesh’s revenue/GDP will rise from 9.8 per cent in FY23 to 10 per cent in FY24. However, the ratio remains very low relative to other sovereigns that we rate, and we continue to view it as a key credit weakness. Based on Fitch’s metric, Bangladesh’s revenue/GDP stood at 9.8 per cent in FY22, against a median of 28.5 per cent for ‘BB’ peers.”

“The budget initiates a medium-term strategy to raise revenue/GDP. As part of this, it establishes compliance risk-management units under the National Board of Revenue, and proposes strengthening compliance and information sharing between the Board’s income tax, VAT and customs wings.”

“It also looks to enhance the automation of tax administration and enhance at-source revenue collection. We view these moves as positive, but it will take time to assess their effect.”

“When we affirmed Bangladesh’s rating at ‘BB-’, with a Stable Outlook, in September 2022, we said increased confidence in the sovereign’s capacity to deliver fiscal consolidation and debt stabilisation over the medium term - for example through a sustained improvement in the structure of public finances in terms of a higher revenue base and lower contingent liabilities - could lead to positive rating action.”

“In the medium-term macroeconomic policy statement presented with the budget, the government indicated that Bangladesh Bank will reverse the temporary margin increases imposed on letters of credit for non-essential imports.”

“This may signal an easing of external pressures, which contributed to a decline in official reserve assets from a peak of USD48.1 billion at end-August 2021 to USD29.9 billion at end-May 2023. In September 2022 we said that a sustained drop in foreign-exchange reserves could lead to negative rating action.”