Maintaining the existing asset quality, now largely helped by generous government support regimes, may emerge as a key challenge in post-pandemic situation for Bangladesh's banking sector.

Such prognosis comes from the central bank as the country begins to gather wits despite the rampage by the covid-19 scourge as the world starts reopening and economies recovering from ruins.

The Bangladesh Bank's latest prediction, incidentally, comes against the backdrop of falling trend in non-performing loans (NPLs) as manifest by the end of 2020 following a loan-moratorium facility handed out by the central bank.

The share of classified loans in the total outstanding credits came down to 8.1 per cent end-December 2020 from 9.3 per cent in the same period of 2019, partly due to temporary relaxation in loan-classification regulations during the period under review, the central bank said in its latest Financial Stability Report (FSR) 2020.

Asset quality improved during the latter part of calendar year (CY) 2020 as gross classified-loan ratio showed a conspicuous drop driven by improvement in NPL position of both public and private banks, the FSR explains.

"….maintaining improved asset quality in post-Covid-19 situation might remain a key challenge for the banking sector," the FSR noted.

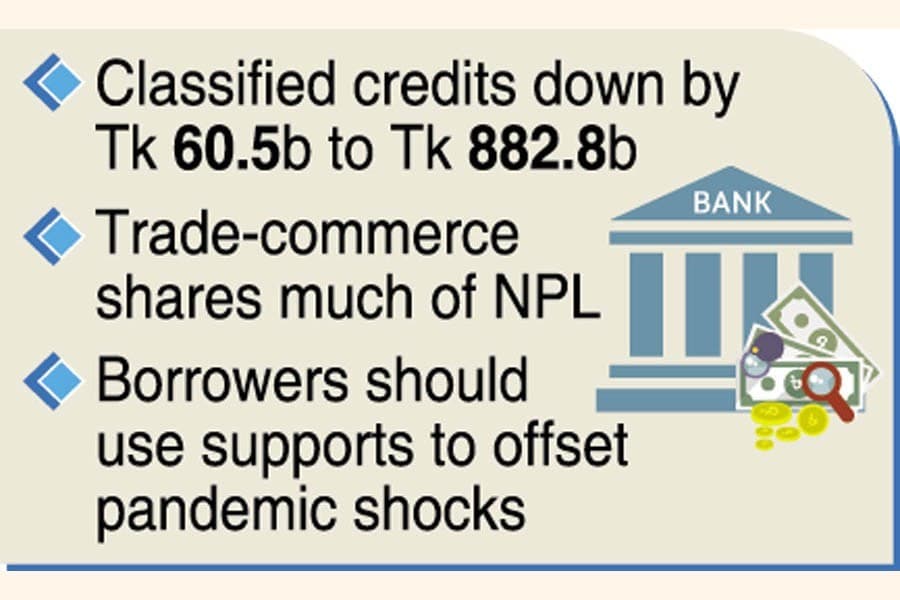

Besides, the amount of classified loans decreased by Tk 60.5 billion to Tk 882.8 billion as of December 31, 2020.

"Despite the recent improvements, proper monitoring of regular loans along with rescheduled loans amid the Covid-19 pandemic may appear to be a critical challenge for the banking industry," it is stated in the FSR.

It also says though the central bank has already extended necessary policy supports to help out the borrowers as well as banks, the success of such policy backup in minimizing the impact of Covid-19 largely depends on how efficiently the borrowers use the policy perks in withstanding the shockwaves from the pandemic.

However, the sector-wise default-loan distribution did not indicate a higher concentration of NPLs in any particular sector except trade and commerce in CY'20, according to the FSR.

The amount of classified loans in trade and commerce-generally known as commercial loans-stood at Tk 247 billion, nearly 28 per cent of entire NPLs in the banking system, in CY'20.

The amount of loans rescheduled in 2020 decreased as compared to the preceding year, which could partly be attributed to BB's policy props during the disruptive pandemic.

The BB data show the volume of rescheduled loans down to Tk 134.7 billion in 2020 from Tk 527.7 billion a year ago. It was Tk 232.1 billion in 2019.

However, rescheduled loans, if not recovered, might have adverse impact on profitability and solvency of banks, necessitating close monitoring and stringent supervision to minimize downside risk to the entire banking system.

Rigorous monitoring and implementation of stringent measures for recovery of loans has utmost importance in minimizing downside risks in banking, according to the FSR.

BB Governor Fazle Kabir in a message said banks and non-banking financial institutions (NBFIs) must ensure proper utilization of loans, including those from the Covid-related refinance schemes.

Alongside, they also need to enhance their loan-recovery initiatives as the economy starts recovering, he added.

"What is more, as the exact extent and trajectory of Covid-19 is still uncertain, the stakeholders of the financial system should devise forward-looking strategies to cope with this new-normal situation," the central bank chief noted.

siddique.islam@gmail.com