Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Many of Bangladesh's commercial banks, having core income-generating instruments under immense pressures, now focused on fee-based incomes under a changed strategy to navigate the crunch time.

The change in the income-making approach to make their balance sheet sustainable comes in the wake of looming liquidity crunch in the banking industry because of the existing volatility in the country's macroeconomic situation, bankers have said.

According to them, the demand for formal credits by the private sector keeps shrinking while the commercial lenders are reluctant to give credits in this critical period of time to avoid anticipated election-related instability.

On the other hand, the volume of imports dropped remarkably in recent months because of the central bank's belt-tightening measures amid persisting forex dearth, and it badly impacted income of the banks.

Bangladesh Bank (BB) very recently took some money-controlling measures like increasing the policy rate by 75 basis points to 7.25 per cent, stopping injections of high-powered money into the economy and curtailing liquidity support to the banks that have started putting more pressures on the liquidity in the banking sector.

Simultaneously, the banks need to spend a significant portion of their liquidity to buy the US dollar from the country's foreign- currency reserves managed by the BB to meet their foreign- currency obligations amid prevailing forex dearth that puts extreme pressure on the banks' liquidity, according to them.

Managing Director and CEO of Dhaka Bank Emranul Huq says as the central bank raised the upper limit of lending rate by 50 basis points after the revision of policy rate, they have now been concentrating on maintaining sustainable NIM (net interest margin) keeping the deposit rate at a tolerable level.

Besides, the bank's top executive says, they have intensified their attention on fee-based income-earning products like digital banking, card services while work-order financing, SME financing and consumer loans are also being prioritised under the current context of banking operations when liquidity is becoming a major issue.

Also, they have are now making additional efforts for recovery of unpaid loans, especially the written-off ones, to reduce the volume of non-performing assets. "And the progress is satisfactory," Mr Huq says.

Managing Director and CEO of Social Islami Bank Limited (SIBL) Zafar Alam has said they have also intensified their focus on fee-based products alongside more deposit collection with good offers to the investors.

He feels that the NPL buildup in the industry becomes a matter of serious concern as the volume of bad loans had increased to Tk 1.56 trillion until June 2023.

"If we can bring it down to even Tk 1.0 trillion, the existing stress in the banking system will be lessened to a great extend. We need to give utmost priority to the areas but cooperation of other agencies is also required simultaneously," the SIBL managing director says about the bail-in bids.

Managing Director and CEO of Pubali Bank Limited Mohammad Ali has said they are not concentrating on incomes through selling US dollars. "Our focus is simple--to reach more deposits and give advances as many as possible to gain more NIM."

The bank earned deposits worth Tk 80 billion and disbursed advances amounting to Tk 60 billion this year so far, and "it is contributing a handsome income".

At the same time, they have invested Tk 45 billion in the short-term government securities so that the bank does not face any problem in payment-related obligations in case of any big payment.

Seeking anonymity, a top executive of a private commercial bank said many of the banks were passing tough times because of the tightness in liquidity situation.

As the demand for private credit and the volume of imports have fallen drastically in recent months, the income of the bank dropped significantly. On the other hand, institutional investors have already started diverting their funds into the government treasury instruments riding on the higher rates. At the same time, banks have to buy dollars from BB to meet their import liabilities.

"So, liquidity turns to be a serious issue now. We're trying hard to overcome the situation paying serious attention on earnings from non-core areas," the banker said about their tricks of the trade aimed at weathering the bad weather they feel in banking.

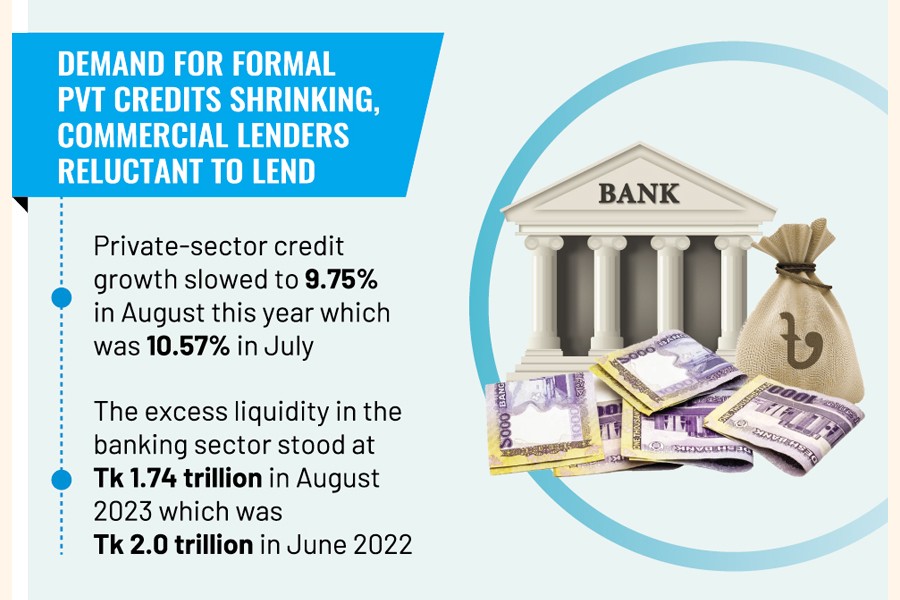

According to the BB, private-sector credit growth slowed to 9.75 per cent in August, down from 10.57 per cent in July and 11.56 per cent a year ago.

The excess liquidity in the banking sector also dropped to Tk 1.74 trillion in August 2023 from Tk 2.0 trillion recorded in June 2022.

jubairfe1980@gmail.com