Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The Bangladesh Bank (BB) has announced plans to implement the Expected Credit Loss (ECL) methodology-based provisioning system for banks by 2027, aligning with the International Financial Reporting Standards (IFRS 9).

Currently, the banking sector follows a rules-based loan classification and provisioning system.

The adoption of ECL methodology represents a shift towards a forward-looking, risk-based approach, as recommended by the International Monetary Fund (IMF).

This new system will assess future risks of default, as opposed to the existing backward-looking method.

The ECL framework, widely practiced in advanced and many developing economies, evaluates potential risks by considering macroeconomic variables and other relevant financial factors. Such risk-based assessments typically involve actuary professionals.

However, the central bank emphasised its commitment to strengthening banks' risk management capabilities and enhancing the transparency of financial reporting through the adoption of IFRS 9, according to a circular issued by it on Thursday.

In December 2015, the Basel Committee on Banking Supervision (BCBS) provided guidance on credit risk and expected credit losses, setting out supervisory expectations for sound credit risk practices.

IFRS 9, which replaces IAS 39, mandates the use of an ECL-based accounting model for impairment loss allowances, addressing procyclicality and emphasising forward-looking assessments.

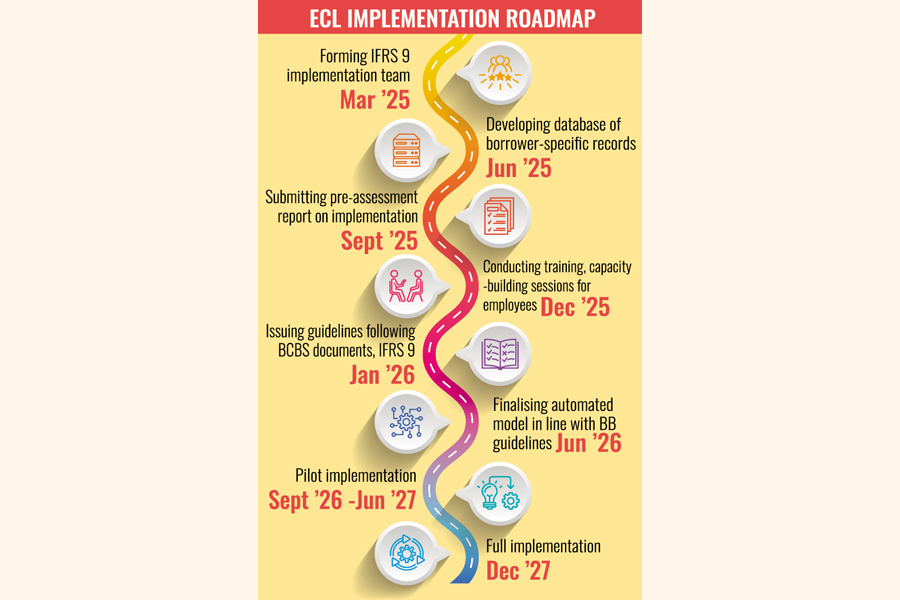

To facilitate the transition, the central bank has outlined a detailed roadmap.

Banks must establish an IFRS 9 implementation team led by the managing director or chief executive officer and prepare a time-bound action plan approved by the board of directors by March 2025.

Banks are required to develop by June 2025 a database containing borrower-specific data - for example, sector-wise, borrower-wise, and loan-nature-wise classification percentages; default rates; loan recovery rates; and macroeconomic factors - on a monthly basis from January 2022 onwards.

Banks must submit by September 2025 a pre-assessment report on ECL implementation to the central bank's Banking Regulation and Policy Department. The report should detail the transition plan, potential challenges, and necessary actions for IFRS 9 adoption.

Banks by December 2025 will have to conduct training and capacity-building sessions for employees involved in ECL-based loan classification and provisioning.

The Bangladesh Bank will issue comprehensive guidelines on ECL-based provisioning, following BCBS documents and IFRS 9, by January 2026.

Banks by June 2026 will finalise automated ECL-based loan classification and provisioning models in line with the central bank guidelines.

By September 2026, pilot implementation will cover branches representing at least 25 per cent of the total loan portfolio. By December that year, this coverage will increase to 50 per cent.

IFRS 9 will be implemented on a pilot basis by June 2027 in branches, which cover at least 75 per cent of the total loan portfolio of banks.

By December 2027, there will be full Implementation of ECL-based loan classification and provisioning under IFRS 9 on a pilot basis.

jasimharoon@yahoo.com