Drug makers' growth hinges on whether they can raise money

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

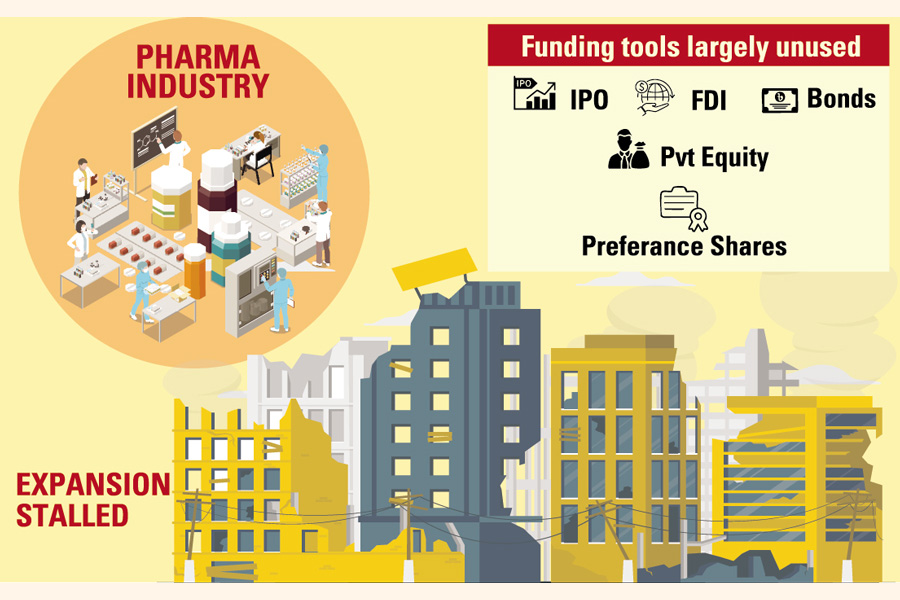

The country's pharmaceutical industry has great potential to grow further, with the rising income and aged population and expansion of export markets, but it has not yet built capacity to explore fund-raising options, including IPO.

Of as many as 200 local companies, only 19 firms of the industry have listed in the equity market. While fund collection by issuing shares to the public has remained insignificant, other instruments for capital, such as corporate bonds, preference shares, private equity, and foreign direct investment (FDI) too have remained largely unused.

The industry, which has already grown to meet almost 98 per cent of the local demand, was projected to be worth $6 billion by this year end, according to the Bangladesh Investment Development Authority. But presently its market size is $3.5 billion, said the Bangladesh Association of Pharmaceutical Industries (BAPI).

In FY24, the pharma & chemical sector attracted FDIs worth $123.8 million, increased from $44 million in FY22, as estimated by Prime Bank Investment.

That shows a remarkable jump in FDIs over the three years to FY24 but industry insiders say foreign investments in local companies were still insignificant in consideration of global FDIs amounting to $1.4 trillion on the manufacturing of drugs and other related components.

Syed M Omar Tayub, managing director of Prime Bank Investment that introduced a programme "Capital Connect" to facilitate financing for pharma companies, said the pharma sector has not been given priority by policymakers to draw FDI.

"Macroeconomic variables are also responsible for the nominal FDI in the pharma sector." For example, the power crisis is one major factor behind sluggish FDI, added Mr Tayub.

The industry's performance is even poorer when it comes to gathering funds through IPOs.

Only four companies raised an aggregate amount of capital worth $2.04 million (Tk 2.55 billion) by issuing primary shares between FY22 and FY24.

Of them, JMI Hospital, Navana Pharmaceuticals and Techno Drugs raised Tk 2.5 billion through IPOs (initial public offerings) while Al-Madina Pharmaceuticals raised Tk 50 million through a QIO (qualified investor offer).

According to industry insiders, only monetary incentives are not enough to inspire listings of pharmaceutical companies; proper valuation of primary shares and flexibility in fulfilling regulatory obligations are also needed.

A listed company enjoys a financial advantage of about 4.5 percentage points, compared to non-listed peers.

Take for example that a non-listed company received a bank loan and has made a profit worth Tk 100. After the payment of tax and interest against the loan, say at a rate of 10 per cent, the company's profit after tax would come to around Tk 63. A listed company also raised a fund equivalent to the amount of bank loan received by the non-listed one and earned a profit of Tk 100. After the payment of tax and distribution of cash dividends at a rate of at least 10 per cent, the company's profit would be Tk 67.50.

So, the listed company's cost of funds is less than the non-listed peer.

However, such a fiscal benefit is not enough, says Muhammad Zahangir Alam, chief financial officer of Square Pharmaceuticals, for a company to choose the equity market instead of banks for financing.

He cited the IPO valuation method and strict regulatory measures as discouraging factors.

Following repeated complaints against the existing IPO valuation process, the securities regulator took steps to make amends and is now at the final stage of executing reforms based on a report submitted by its taskforce.

Lorens Shamol Mallick, company secretary of Navana Pharmaceuticals, said the process to meet regulatory compliance was quite cumbersome before they floated the IPO to raise Tk 750 million.

There are hurdles even after listing. There are investors who intentionally create a chaotic situation at annual general meetings (AGM) or threaten to do so for extorting money from companies, said Mr Mallick.

But there are other options to collect money for business expansion. According to Mr. Tayub, MD of Prime Bank Investment, many companies are not aware of them.

Problems are there on the demand side as well. Since the secondary market for corporate bonds is not vibrant, investors show reluctance to invest in such investment vehicles; money gets stuck in bonds for a long time in the absence of a quick exit.

Also, general investors lack knowledge about corporate bonds.

"A vibrant secondary market is necessary to attract investors towards [corporate] bonds," said S M Galibur Rahman, head of research and strategic planning at Shanta Securities.

At the same time, non-listed companies find it difficult to get equity investments from both local and foreign investors because they do not offer an easy exit.

The secondary market is the place of exit for those who inject funds targeting listing within an expected timeframe. When a company fails to get listed because of improper valuation or any other reason, equity investments get stuck for more than the expected time.

On preference shares, Mr Rahman said that generally the returns from preference shares are lower than fixed-income securities and so investors do not consider them.

ICB Capital Management has been working to inspire the pharmaceutical companies to raise funds by issuing bonds or preference shares.

"Our experience suggests that many companies do not intend to raise funds using those tools. So, while regulatory support is needed, companies will have to change their mindset as well," said Mazeda Khatun, managing director of ICB Capital Management.

The option of private equity (PE) has also remained unexplored by local pharma companies.

Recent deals sealed by some local companies have given rise to hope. For an instance, Prava Health executed a PE deal worth $10.6 million with foreign investors, including the IFC.

Mr Tayub said drug makers can meet their capital requirements through coupon bonds, zero coupon bonds, convertible and green bonds too.

The financing opportunities must be utilized for the sector to expand and boost exports. Despite the rapid growth of the industry over the last decade, revenue from drug exports is negligible and falls behind exports of leather and leather goods, agricultural produce, jute items, and frozen foods.

In FY24, the pharmaceutical sector made exports worth $205 million while the export volume of leather and leather goods was $1.03 billion.

mufazzal.fe@gmail.com