New subordinated debt pleas give rise to debate over banks’ capital raising trend

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Six banks have recently sought permission of the securities regulator to raise Tk 35 billion in total through subordinated debts to strengthen their capital base, calling into question again the outcome of such instruments.

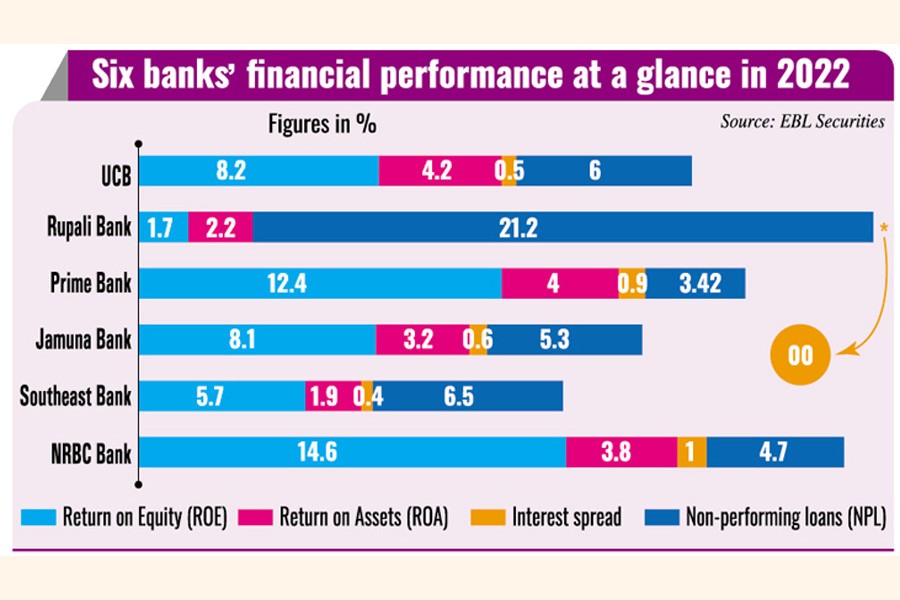

Among the applicants, UCB seeks to raise Tk 3

billion, Rupali Bank Tk 12 billion, Prime Bank Tk 6

billion, Jamuna Bank Tk 5 billion, Southeast Bank

Tk 5 billion and NRB Commercial Bank Tk 3 billion.

For the last few years, banks have preferred issuing subordinated debts to increasing paid-up capital or retaining profits to bolster their financial position, but experts say such debt instruments intensify the cost burden of the issuers instead.

The capital raised to ensure a supplementary layer of a bank's reserves is actually a liability, against which the bank concerned has to pay interest at the rate of 6-10 per cent.

That interest burden slims down the profit margin of the bank as it is allowed to lend money at maximum 10.10 per cent under the recently introduced interest rate regime based on SMART (six-month moving average rate of T-bills) rate of 7.10 per cent.

Nevertheless, banks rely on money gained through subordinated debts to have capital adequacy because without it foreign banks would not show any interest in doing business with them.

The cost of doing business is, however, much higher with such debts since the interest rate is more than the rate of fixed deposit receipts (FDRs).

The financial tool also comes in handy as banks look to boost its capital base to gain depositors' confidence.

Banks' capital reserves are divided into tier-I and tier-II.

Tier-1 capital, the core capital that shows the financial health of a financial institution, can be increased by raising paid-up capital or retaining profits whereas tier-2 capital can be strengthened through general provisions or subordinated debts.

Banks of other countries, including India, have huge retained earnings strengthening their capital base, said an official of the central bank preferring not to be named.

But banks here do not retain profits as owners and general shareholders demand dividends, said Dr Zahid Hussain, former chief economist of the World Bank's Dhaka office.

Another reason is that banks have to pay a super tax on profits retained.

"There is no logic behind imposing such tax," added Mr Hussain.

Non-performing loans accumulated for years and under provisioning are the reasons behind capital inadequacy of banks. Their fundamentals can be stronger if they ensure good corporate governance and retain profits to achieve a strong business position.

Of the six banks that are looking to issue the debt instrument, UCB saw the highest 34 per cent year-on-year growth in profit to Tk 3.30 billion for 2022 while Prime Bank's profit jumped 23 per cent to Tk 3.99 billion for the same year.

On the other hand, Rupali Bank, Jamuna Bank, and Southeast Bank reported a year-on-year decline in profit by 1.8 per cent to 43 per cent for 2022.

Banks issue subordinated debts when they increase loans, said Pubali Bank's Managing Director Mohammad Ali.

The underlying risk is that subscribers may face non-payment of dues by the issuer if it gets into trouble.

In Bangladesh, the worse thing is that "banks subscribe the subordinated debts [issued by other banks] with the depositors' funds. It's a liability, not real capital," said Ahsan H Mansur, executive director of the Policy Research Institute of Bangladesh (PRI).

Owners should strengthen the capital base with their money, he added.

In absence of a debt market, banks are interdependent to raise capital.

"There is a risk of such interdependency as the subscribers may face difficulties if an issuer bank fails to settle debts," Mr Hussain said.

mufazzal.fe@gmail.com