Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

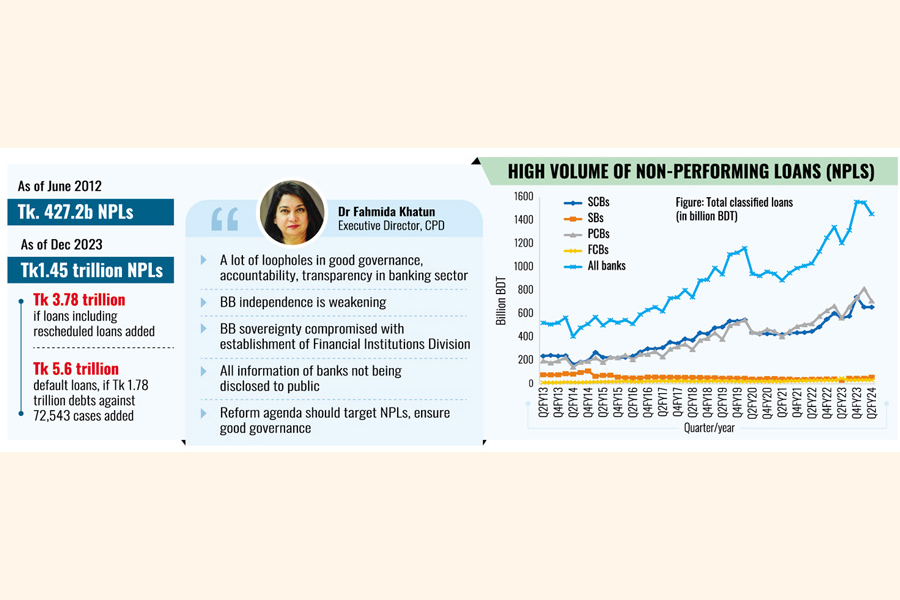

In ten years' time till last December, the volume of non-performing loans or NPLs more than tripled to Tk1.45 trillion in Bangladesh and exacerbated the cash crunch in banks.

In ten years' time till last December, the volume of non-performing loans or NPLs more than tripled to Tk1.45 trillion in Bangladesh and exacerbated the cash crunch in banks.

If another chunk of banks' liquid asset stuck up as rescheduled loans is added up, the amount of dud money banks are bearing will come to Tk 3.78 trillion, a CPD survey report says.

Also, there is Tk 1.78 trillion of unpaid debts against 72,543 cases pending with the loan courts. Altogether, the total amount of default loans will be Tk 5.6 trillion.

Such portrayal of state of the country's banking industry came in a presentation made by Dr Fahmida Khatun, executive director of the Centre for Policy Dialogue, at a cutting-edge meet Thursday on the sector situation fraught with numerous problems.

The seminar, titled 'What lies ahead for the banking sector of Bangladesh', was held at a hotel in the city that gathered well-conversant persons.

A bank-by-bank calculation she presented shows that since June 2012 till December 2023, default loans had increased from Tk 427.2 billion to over Tk 1.5 trillion.

A bank-by-bank calculation she presented shows that since June 2012 till December 2023, default loans had increased from Tk 427.2 billion to over Tk 1.5 trillion.

It notes that the size of the economy of Bangladesh is increasing, and so the role of the financial sector is vital for investment and common people.

"We only discuss the banking industry--the non-banking sector is also beset with multiple problems," the economist told the audience.

She notes that a key determinant of the banking sector's health is non-performing loans. "Its (NPL) amount is gradually increasing. There has been a lot of lack of good governance, accountability, and transparency in this sector. The banking sector is still unable to recover for that erosion."

Regarding good governance in the industry, the policy think-tank thinks independence of Bangladesh Bank, the banking sector regulator, is gradually weakening.

The central bank's "sovereignty has been compromised" through the establishment of the Financial Institutions Division or FID.

"We see many times FID of in the Ministry of Finance as regulator. But the central bank is supposed to work independently, but it is not able to do that," the ED said in the presentation.

As recent press restrictions on access to the central bank stand out as talk of the town nowadays, she said, "All information of the banks is not being disclosed to the public."

Another issue is a gradual closing of the doors on information. "We used to depend on the media for information--that too is going away. There remains a risk of wrong policies being adopted for a lack of information."

The CPD presentation on findings says a higher concentration of NPLs is not only in state-owned commercial banks or SCBs but also the private commercial banks or PCBs.

Its findings show average expenditure-income ratio was 0.81 in SCBs and 0.74in PCBs. Such ratio between 0.5 and 1 indicates that a bank is poorly managed, but not making a loss. If the ratios are below 0.5, that indicate better-managed banks.

The think-tank has found excess liquidity in the industry having declined from Tk 2.32 trillion in June 2021 to Tk 1.62 trillion in February 2024.

And the real deposit rate, calculated as the weighted average of the monthly deposit rate of all scheduled banks adjusted with the monthly inflation, fell from 0.03 per cent in March 2020 to minus 4.7 per cent in February 2024.

"The negative real interest rate on bank deposit means that a depositor becomes a net loser by keeping money in the banks," it is stated in the paper as a major cause of liquidity crunch.

Spotlight also fell on forced bank mergers and acquisitions, showing that strong banks are burdened with the liability of weak banks.

The weak-bank directors potentially return to top-leadership positions after a gap of five years. There are concerns about the accuracy of financial assessments of weak banks and the overall process.

The CPD has identified some challenges of the forced mergers: job losses and integration, customer confusion, and concern.

As such, the think-tank advocates for a comprehensive reform agendum and implementation of such reform to overcome the banking sector's ongoing problems.

"The reform agenda should aim to reduce the NPL and establish good governance in the industry," the function was told.

jasimharoon@yahoo.com