Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The tax liability of most businesses would go up, especially in the case of import-dependent companies and suppliers, due to the certain fiscal measures proposed in the new budget.

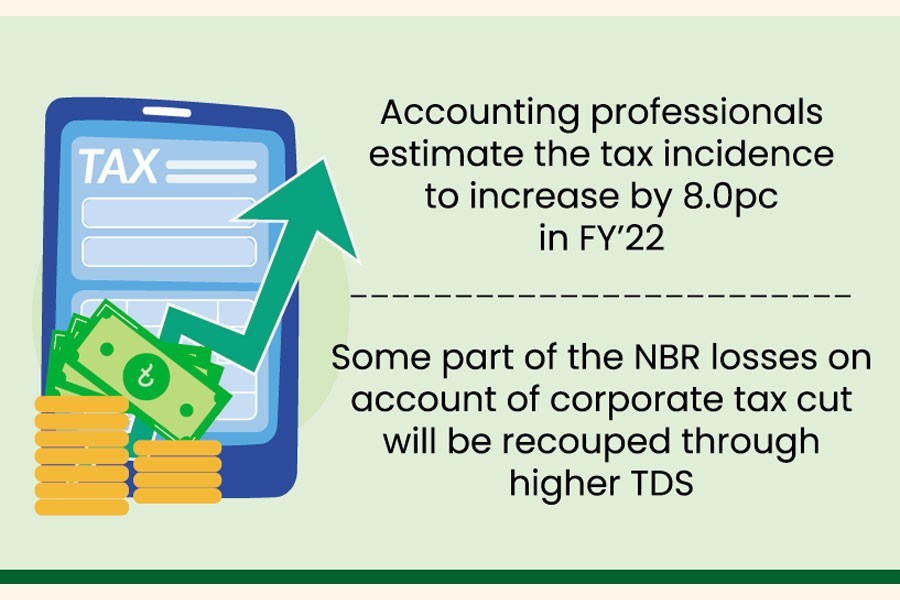

The budget for the fiscal year (FY) 2021-22 proposes to increase the rate of tax deduction at source (TDS) for the contractors and suppliers of goods, accountant professionals have said.

They estimated the tax incidence to go up by 8.0 per cent although it would vary depending on the nature of business.

The proposed increase in TDS rates up to 7.0 per cent on the bills of contractors and suppliers may escalate the effective rate or actual payable amount of income tax even after reduction of the corporate tax by 2.5 per cent for both publicly listed and non-listed companies, they said.

For example, the actual tax liability on businesses would be 58 per cent from the existing 50 per cent, taking the increased rate of TDS into consideration.

According to the Income Tax Ordinance-1984, the TDS on the bills of contractors and suppliers is considered as minimum tax, under section 82 C, and it is not refundable.

The accountant professionals said the reduction of corporate taxes would not benefit most of the companies unless the withholding tax rates are brought down.

In the proposed Finance Bill-2021, the TDS on the bills of contractors and suppliers has been increased to a range between 3.0 per cent and 7.0 per cent from the existing range from 2.0 per cent to 5.0 per cent on the basis of threshold levels of base amount.

The contractors and suppliers realising bills up to Tk5.0 million will have to pay 3.0 per cent TDS while the rate is 5.0 per cent on bills ranging between more than Tk 5.0 million and Tk 20 million and 7.0 per cent on more than Tk 20 million.

Currently, the tax rate is 2.0 per cent for up to Tk 0.2 million, 3.0 per cent for above Tk 1.5 million to Tk 5.0 million, 4.0 per cent for above Tk 5.0 million to Tk 10 million and 5.0 per cent for above Tk 10 million.

Officials at the National Board of Revenue (NBR) expected that the possible loss of revenue due to cut in the corporate tax rates would be offset by the upward adjustment of the TDS on the bills of contractors and suppliers.

The tax authority mobilises a huge amount of direct tax from the contractors and suppliers with minimum efforts as the deducting authorities, including public and private companies, are responsible to collect the tax and deposit it to the public exchequer.

A former member of income tax wing, however, opposed the upward adjustment of TDS on the bills of contractors and suppliers, expressing concern over a surge in development project cost in both public and private sectors.

He said the TDS on the contractors' bills contributes around 50 per cent of the withholding tax collection of NBR.

Every year, a large number of contractors receive the recognition as the top taxpayers for their highest payment of taxes that they pay in terms of TDS.

The former tax official said the NBR should go for effort-based tax collection by expanding the tax-base rather than increasing the tax rates.

Former president of the Institute of Chartered Accountants of Bangladesh (ICAB) Md Humayun Kabir, chairman of the taxation committee of the association, said the businesses have to earn profit at more than 23 per cent to pay the TDS at 7.0 per cent on supply of goods.

The rate should be below 3.0 per cent to help the corporate taxpayers reap the benefit of the corporate tax reduction.

"The cut in corporate tax would help the country improve its position in the doing business index of the World Bank (WB), rather than benefiting the businesses, due to the higher rate of withholding tax," he added.

Snehasish Barua, member of ICAB and partner of Snehasish Mahmud &Company, said the corporate tax cut would help attract investment, but the country's tax collection is predominantly being dependent on the source taxes.

As per law, the tax collected at source represents the minimum tax incurred during transaction and it is not refundable.

He said the AIT at import stage could have been reduced to 3.0 per cent in line with the changes in Advance Tax (AT) of VAT.

On upward adjustment of TDS for suppliers of goods and construction, he said that if a manufacturing (import and supply) company pays Tk 10-12 on every sale of Tk100; it will have to earn a profit of 33.33 per cent or 40 per cent on the sale.

It is very challenging under normal business condition let alone during the Covid-19 pandemic, he said.

The actual tax liability would be higher for a company that imports goods or supplies to the consumers or providing them services, he added.

"Change in the tax rate could be more beneficial to the businesses if the government brings down the TDS," he added.

A senior official of the NBR, however, said that most of the corporate sectors were enjoying concessionary rate of taxes, including the readymade garment sector, where the effective tax rate is only 16 per cent.

"We have offered a vast range of tax holiday facility for businesses. Only a few businesses pay tax at 32.5 per cent currently," he added.

doulot_akter@yahoo.com