Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Women's participation in the formal banking system continues to expand, but a persistent gender gap in access to credit remains a key concern, according to the latest Bangladesh Bank (BB) data.

While women are steadily strengthening their presence on the deposit side, their share in lending remains comparatively low, underscoring structural constraints in accessing productive finance.

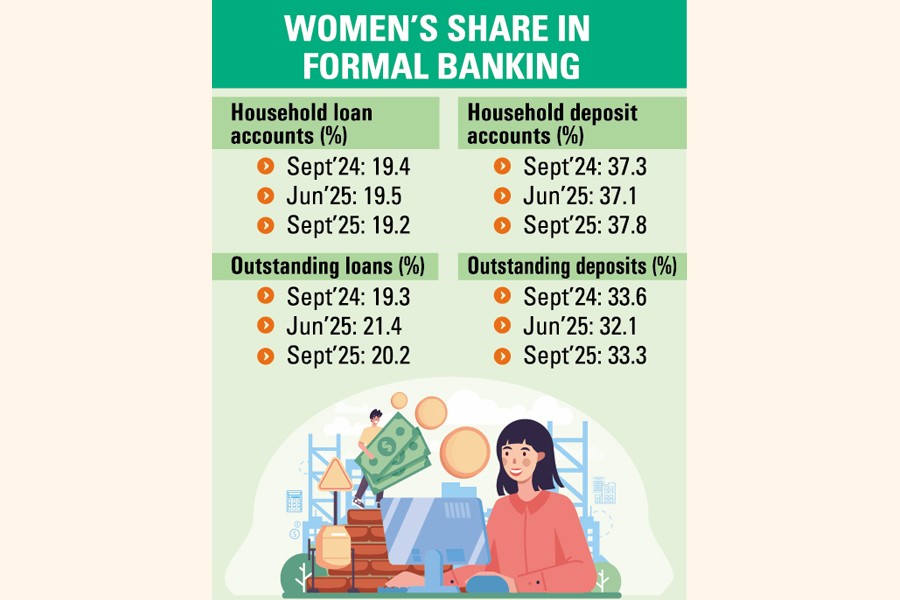

On the lending side, women's presence remains below one-fifth of the total household loan accounts.

The number of household loan accounts increased to 12.612 million in September 2025 from 10.806 million in September 2024.

Household loan accounts stood at 12.033 million in June 2025.

Women held 19.2 per cent of the total household loan accounts in September 2025, almost unchanged from 19.4 per cent a year earlier and slightly down from 19.5 per cent in June 2025.

Outstanding loans and advances rose to Tk 2.46 trillion in September 2025 from Tk 2.34 trillion a year ago.

Such loans and advances stood at Tk 2.69 trillion in June 2025.

Women's share in outstanding loans stood at 20.2 per cent in September 2025 -- higher than 19.3 per cent in September 2024, though lower than 21.4 per cent recorded in June 2025.

The figures suggest that although women's borrowing has increased in absolute terms, their proportional access to formal credit has not kept pace with their growing role in deposit mobilisation.

On the deposit side, women's participation continues to strengthen.

As of September 2025, women accounted for 37.8 per cent of the total household deposit accounts, up from 37.3 per cent in September 2024 and 37.1 per cent in June 2025.

In absolute terms, the total number of household deposit accounts rose to 163.60 million in September 2025 from 144.88 million a year earlier, reflecting steady growth in financial inclusion.

Outstanding deposits also increased during the period, reaching Tk 11.50 trillion in September 2025, compared with Tk 10.02 trillion in September 2024.

It reached Tk 11.09 trillion in June 2025.

Women's share in outstanding deposits stood at 33.3 per cent in September 2025.

Although slightly lower than 33.6 per cent recorded a year earlier, it marked an improvement from 32.1 per cent in June 2025.

The central bank data indicates that while more women are opening and maintaining deposit accounts, their average balances remain lower than those of male depositors -- a reflection of prevailing income and asset disparities.

Commenting on the trend, Dr Masrur Reaz, chairman of Policy Exchange Bangladesh, says the latest data reflects steady gains in women's financial inclusion but also highlights persistent structural gaps in access to credit.

"Women now account for nearly 38 per cent of household deposit accounts, which is a positive signal for savings mobilisation and economic empowerment. However, their share in loan accounts remains around one-fifth, indicating that access to productive credit is still constrained," he says.

He notes that while account ownership has expanded significantly, the real challenge lies in improving the quality and depth of financial inclusion.

"Banks and policymakers must focus on designing gender-responsive lending frameworks, easing collateral requirements where feasible, and expanding SME and entrepreneurship financing for women," he adds.

Dr Reaz also observes that enhancing women's access to formal credit will not only promote equity but also strengthen overall economic growth by unlocking untapped entrepreneurial capacity.

For banks, the data carries a dual message.

Women are emerging as an increasingly important depositor base, suggesting scope for tailored savings products, digital financial services, and targeted financial literacy initiatives to enhance engagement and improve average balances, according to stakeholders and analysts.

At the same time, the relatively low share of women in loan accounts highlights significant untapped credit potential, they say, adding that expanding collateral-free lending, SME financing, and value chain-based products for women entrepreneurs could help narrow the credit gap while supporting inclusive growth.

sajibur@gmail.com