Can S.S. Steel justify its historically low dividends?

Investors are unlikely to get a better return from investments when the business seems to be on the decline

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

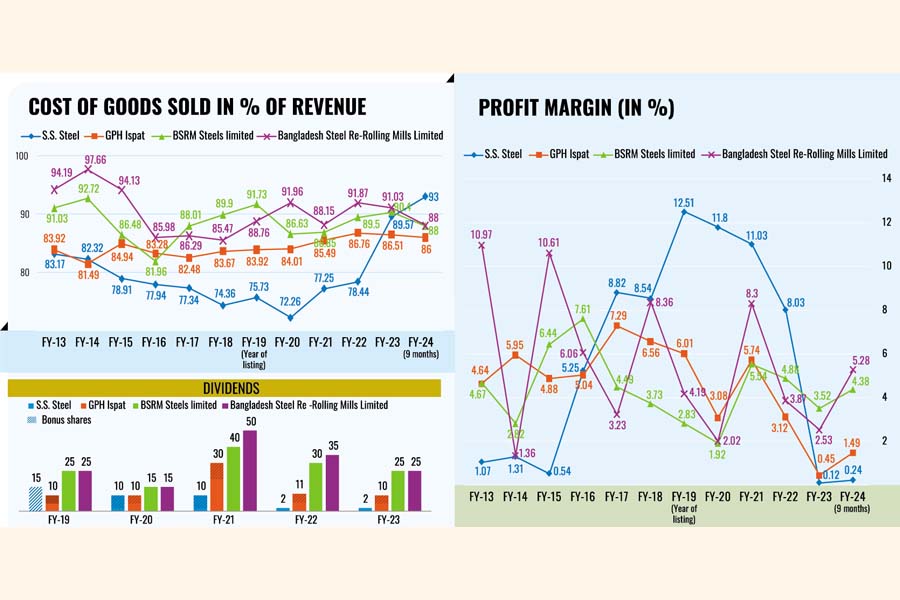

S.S. Steel has been paying insignificant amounts of dividends to its shareholders, compared to its listed peers in the industry, but earnings that it supposedly kept with itself have not been translated into business growth.

In fact, the company's profit margin, meaning the profit it has earned in relation to its revenue, has kept shrinking at a faster pace every year since its 2019 listing than the growth rate in the years before going public.

In FY19, S.S. Steel had a 12.51 per cent profit margin; while GPH Ispat had 6 per cent, BSRM Steels Limited only 3 per cent and Bangladesh Steel Re-Rolling Mills Limited 4 per cent.

In the four years to FY23, S.S. Steel's profit margin plunged to a mere 0.12 per cent, whereas GPH Ispat's to 0.45 per cent, BSRM Limited's to 4.38 per cent and Bangladesh Steel Re-Rolling Mills Limited's to 5.28 per cent.

One explanation might be S.S. Steel's loss of efficiency, as found in an analysis by the FE of the company's financial statements.

In FY22, S.S. Steel's cost of goods sold was equivalent to more than 78 per cent of its revenue, still lower than others, but it jumped by nearly 11 percentage points to 90 per cent the next fiscal year. In the nine months to March FY24, the cost of goods sold rose by another 3 percentage points to 93 per cent of the company's revenue, leaving other listed steelmakers behind.

The cost efficiency that S.S. Steel could take pride in before it entered the stock market has withered since the year after it floated shares to the public.

Md. Mostafizur Rahamn, company secretary of S.S. Steel, told the FE that a stronger dollar against the taka and higher utility prices had driven up expenditures and reduced profit margin.

Regarding the rise in the cost of goods sold, he said S.S. Steel, smaller in size compared to others, was unable to hike product prices.

"Our competitors are big. They have contracts with the government [for product supply to development projects]. They can charge higher than before for their products.

"Our customers are small customers. Hence, we cannot increase prices."

S.S. Steel's cost of goods sold jumped at a time when raw material prices went down in the international market. That means the company could not take advantage of the changing global scenario.

Meanwhile, investors are being deprived of a good return on investments.

Even when S.S. Steel secured an enviable profit margin (between FY19 and FY22), it paid marginal dividends to shareholders. Therefore, shareholders will not be able to expect more from what they have injected into the company when the business is on the decline.

A company may pay less or no dividends to shareholders when it invests all its income back into business for expansion and growth.

That has not happened in the case of S.S. Steel though as a small company it is likely to have more room for growth.

The steelmaker maintained a revenue growth of 26 per cent on an average annually between FY13 and FY23 whereas GPH Ispat gained a growth of 37 per cent and Bangladesh Steel Re-Rolling Mills Limited 34 per cent during the same period.

Only BSRM Steels Limited had a lower annual average revenue growth of 17 per cent than S.S. Steel.

Last November, S.S. Steel declared that it acquired the fixed assets of both Super Steel Limited and Peninsula Steel Mills Limited, located at Shitakund of Kadamrasul, Chattogram. The fixed assets include 164 decimals of land, steel structure shed, building, capital machinery, and utility connections, having an estimated value of Tk 1.3 billion.

According to the company, this acquisition would increase its production capacity.

"I hope S.S. Steel Limited will recover soon from this [present] situation, will regain its cost efficiency and will do well in future," said the company secretary, adding that revenue would grow further in future as "we have purchased two companies".

Investors have to wait to see that.

Meanwhile, the stock of S.S. Steel closed at Tk 10.80 per share on Wednesday on the Dhaka Stock exchange (DSE).

Its price-to earnings (P/E) ration, which indicates how much investors have paid for every one taka income of the company, stood at 67.5 on Wednesday, with the latest nine-month's unaudited earnings taken into consideration.

That paints a grim picture; the stock seems to be overvalued only at Tk 10.80 per share, a little over the face value.

On the other hand, GPH Ispat's P/E ratio is 15.17, BSRM Steels Limited's 5.49 and Bangladesh Steel Re-Rolling Mills Limited's 6.04 based on the latest un-audited financial statements.

farhan.fardaus@gmail.com