Leading NBFIs benefit little from higher interest rates in fierce fight for deposits

BABUL BARMAN and FARHAN FARDAUS

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Leading non-bank financial institutions' cost of funds rose amid monetary tightening, resulting in a lower profit in the first quarter through March this year, compared to the same quarter last year.

Hence, the hikes in lending rates after the withdrawal of the 9 per cent rate cap could do little to boost their income.

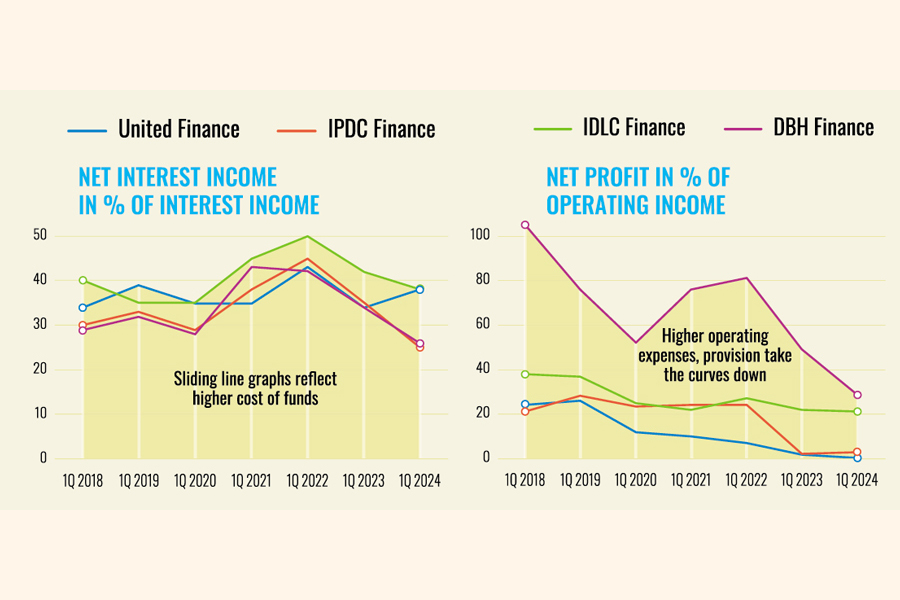

The weighted average cost of funds of NBFIs in January 2023 was 6.65 per cent, which reached 7.50 per cent in January this year, according to the Bangladesh Bank data. At the same time, the adjusted cost of credit rose to 8.79 per cent in January this year from 7.59 per cent in January last year.

The maximum interest rate that NBFIs could charge clients was determined by six-month moving average rate of Treasury bills (SMART) plus a 5 percent margin before the removal of SMART recently.

However, Masud Karim Majumder, chief financial officer (CFO) of IDLC Finance, said, "The real cost of funds went up at a faster pace compared to the ceiling [SMART plus the margin between 1Q 2023 and 1Q 2024] in many cases, which reduced interest spread."

The IDLC Finance's average interest rate spread fell to 2.51 per cent in the January-March quarter this year from 2.72 per cent in the same quarter a year ago.

When SMART rate was 10.50 per cent, many NBFIs collected funds at 11 percent to 11.50 per cent, narrowing their interest spread, which ultimately eroded their net profit, said Mr Majumder.

Moreover, NBFIs could not increase interest rates immediately for old clients even after the central bank had lifted the interest rate cap in July last year. They had to wait for at least six months before applying new rates to old accounts.

"We are yet to benefit from the rising lending rate as costs of funds went up as well."

In the present economic situation, the liabilities (deposit) rate has been rising faster than return from assets (funds lent) due to high inflation.

Interest rates on liabilities are adjusted every three months but asset basket has to be recast every six months, said Mr Majumder.

"We could not push up the lending rate in line with the deposit rate due to high inflationary pressure."

For example, if the interest rate were elevated by 3 per cent, many of the clients would fail to pay monthly installments. And if any client failed to pay installments for more than three months in a row, their accounts were suspended and the lender could not show any income from those accounts in their balance sheets.

Besides, non-performing loans escalated in some areas, home loans and retail loans for example, thanks to runaway inflation.

The average NPL ratio in the overall sector rose to nearly 30 per cent as of March this year, which was 25 per cent a year earlier, according to the BB.

Meanwhile, NBFIs have had to compete with banks while running their operations.

The banking sector has more sources of income than NBFIs. Generally, NBFIs offer higher deposit rates than banks to attract depositors. After the withdrawal of the lending rate cap, banks' interest rate climbed up significantly prompting savers to move funds to banks.

To remain in business in such a scenario, many NBFIs offered a further rise in deposit rates, leading to a higher cost of funds.

At the same time, large NBFIs, which have huge investments in the equity market, earned little from stocks that have remained gloomy all along to this date. On top of that, leasing companies had to keep a higher provision against unrealised losses.

DBH Finance's net profit plunged 34 per cent year-on-year to Tk 172.4 million in January-March this year, owing to higher interest payment against deposits and shrinking income from the stock market.

The largest housing finance institution in the private sector saw a 26 per cent rise in interest income to Tk 1.69 billion, but its interest payment soared 41 per cent to Tk 1.25 billion, slashing its net interest income.

Higher provision against stock market investment due to price erosion of some blue chip stocks also negatively impacted DBH Finance's profit.

NBFIs have to keep 100 per cent provision on unrealized losses in the stock market investments.

"After the floor price was gone, stock prices of some blue chips have fallen significantly. Accordingly, it [DBH Finance] has to keep a provision of Tk 86.4 million against its capital market investments, which is 9.4 per cent of investment in listed securities," the company said in its earnings note.

Major stocks, such as Grameenphone, Robi Axiata, BAT Bangladesh, Renata, United Power, Walton and IPDC Finance lost 21 to 62 per cent market value until Sunday since the removal of the price restriction.

DBH Finance's average interest spread dropped to 2 per cent in January-March this year, from 2.49 per cent in the same quarter a year earlier.

On the other hand, IPDC Finance managed to post a 21 per cent year-on-year growth in profit to Tk 18.37 million for the January-March quarter this year, supported by lower operating expenses.

It witnessed a 14 per cent year-on-year growth in interest income to Tk 1.97 billion in the first quarter this year while the interest payment spiked 31 per cent to Tk 1.47 billion.

Despite a lower net interest income, the company secured a higher profit also because of higher return from government securities.

babulfexpress@gmail.com

farhan.fardaus@gmail.com