Lack of protection against loan defaults is the main reason as to why investors have evinced disinterest in corporate bonds, leading to many debt securities being undersubscribed or unsubscribed.

The kind of investment instrument is usually offered to banks, financial institutions, insurers, corporate entities, and high net worth individuals.

Talking to The FE, several institutional investors said they had refrained from investing in corporate bonds without the guarantee that they would get back the principal and interest and that the repayment would be done within the stipulated time.

The security concern is prevalent for the absence of any bankruptcy rules relevant for corporate bonds, no provision of declaring a bond issuer as defaulter by the central bank in case of defaults on repayment, and non-existence of third-party guarantee.

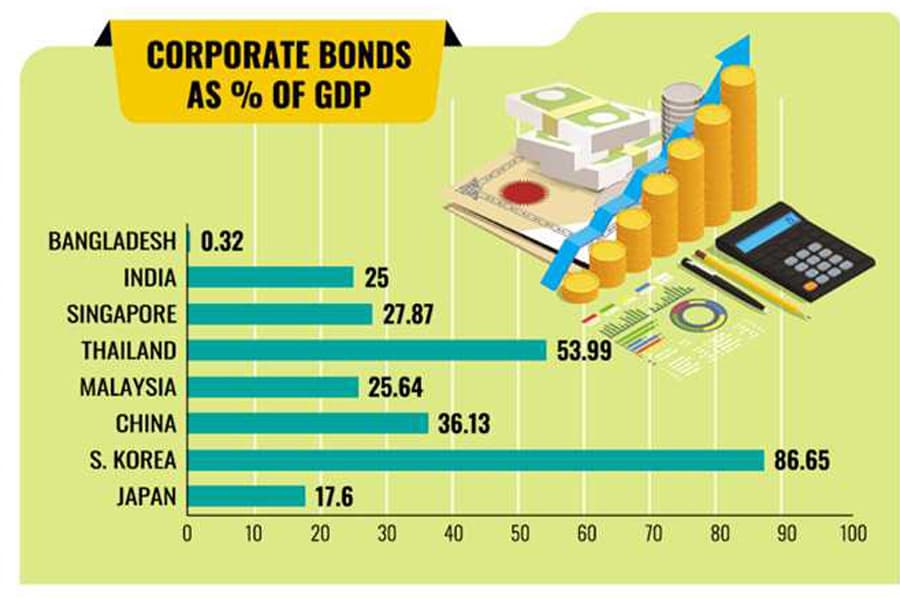

This is the backdrop to an insignificant corporate bond market in Bangladesh. Its size is equivalent to a mere 0.32 per cent of the nation's gross domestic product (GDP).

Globally, the bond market is considered as economic lifeline. India's corporate bond market, which is more than 25 per cent of its GDP, is expected to double by 2030.

Discrepancies

Corporate bonds are a debt instrument issued by a private company to raise money. In return, the issuer pays annual or periodical payments at a fixed or variable interest rate.

If a bank disburses a loan to a business enterprise or an individual, say, for constructing a building, it will do so against collateral. The lender will put up a signboard that the organisation or the individual "is liable to the bank".

The bank also receives cheques from its clients against personal loans so that it can file a case against the debtor in case of any payment default. The individual debtor will be labelled as CIB (Credit Information Bureau) defaulter for not paying back the bank loan.

Such protection mechanisms are not applicable to bond investments.

However, when banks and other financial institutions are bondholders, they get some sort of protection.

Three years back, the Bangladesh Bank introduced a provision allowing banks and non-bank financial institutions (NBFIs) to report bonds as non-performing loans to the BB's Credit Information Bureau.

In that case, bond issuers, except for banks and NBFIs, will be declared as CIB defaulter.

Banks and NBFIs also issue bonds but there is no scope of labelling them as defaulter by other companies and individuals.

"All investors, including individuals, should have means to report default cases to the central bank," said Asif Khan, chairman of EDGE Asset Management.

There are specific bankruptcy rules in other countries, he said, which is why investors feel confident that they would get back money with returns with the help of state-run agencies in case of any default.

Little progress so far

Since investors in Bangladesh cannot keep faith in corporate bonds, they have turned away from the investment tool.

In 2022, Alif Industries received regulatory approval for issuing six-year convertible bonds worth Tk 3 billion but failed to collect a penny owing to investors' apathy.

Gathering fund through corporate bonds has become more difficult for a jump in yields from risk-free Treasury bonds.

Prof. Prashanta Kumar Banerjee, a faculty member of the Bangladesh Institute of Bank Management (BIBM), said trustees had been empowered to ensure bondholders' safety. "But the problem is that they [trustees] haven't set any example restoring investors' confidence in the debt securities."

Md. Moniruzzaman, managing director of Prime Bank Securities, blame nominal fees of trustees for their insincerity in executing tasks with integrity.

Companies' credit rating and a guarantee against corporate bonds are important to rejuvenate the corporate bond market, he said.

On third-party guarantee, Asif Khan, of EDGE Asset Management, said many bond issuers avoid giving third-party guarantee considering cost burden.

But the guarantee draws investors.

For example, GuarnantCo, a private infrastructure development group of the European Union, has guaranteed investors repayment against bonds issued by PRAN Agro. Multinational company MetLife Bangladesh subscribed the debt securities.

When a company provides security against bond investment, it means it will be liable for any default of payments by the issuer.

There are examples of non-settlement of investors' dues against some debentures after maturity.

Eight debentures had been listed on the Dhaka Stock Exchange, which attained maturity between 2002 and 2008.

But the debt securities remained listed until early 2023 for claims of non-settlement of payments to investors.

The regulatory bodies blamed the non-cooperation of the issuers while the issuers said bondholders had not made claims.

The claims were settled years after the maturity of the schemes, according to the Dhaka bourse.

Mohammad Rezaul Karim, an executive director of the Bangladesh Securities and Exchange Commission, acknowledged that investors feel shaky about corporate bonds for previous default cases.

But he disagreed that corporate bond investments lack protection.

Collaterals offered against a secured bond are handed over to the trustee so that it can settle dues after the issuer has become a defaulter, he said.

In case of unsecured bonds, trustees have been empowered through the 2021 trust deed rules to take measures, including legal actions, against defaulters.

Mr. Moniruzzaman, of Prime Bank Securities, said, "A quick solution is a must if there is a case of non-payment [to bondholders] to restore investors' confidence."

mufazzal.fe@gmail.com