Inflation erodes money's might-IV

Digital currency mulled for faster, cheaper, transparent transactions

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The government mulls over switching to digital currency -- a move towards rewriting the history of currency -- which is believed faster, cheaper and transparent in dealings.

Many currency experts also believe that problems related to the disappearance of lower-denomination currencies will be no more under the new order of currencies attuned to the cusp of technology-driven global changes.

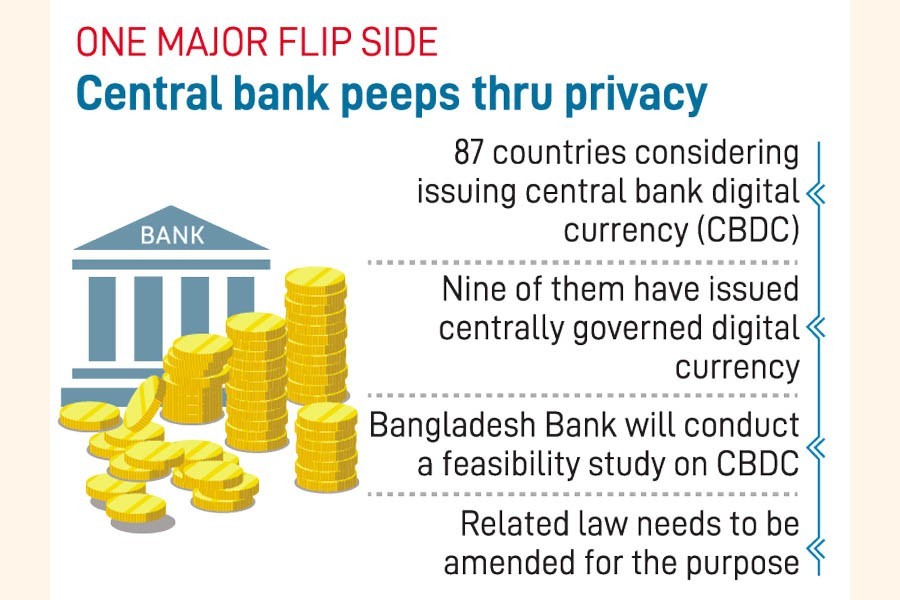

This is just digital version of the existing fiat currency. But it has many disadvantages, including the loss of people's privacy as the central bank will see through how it is earned and how spent and whether the accurate amount of tax paid.

They say the digital version of the money, called central bank digital currency (CBDC), is meant for avoiding some defects associated with the existing fiat money.

Before the fiat money coming into vogue, there were many transitions of the currency, and putting an end to barter trade, gold standards came in. The system ensured conversion of currencies into golds. Now the fiat currency is backed by some metals and reserves along with decree by government declaring it as legal tender. All mentioned above have limitations.

Many countries are now opting for the use of CBDC, which will be under the control of the central bank. In this case, the central bank issues electronic coins or accounts backed by the government.

As of March 2022, 87 countries were considering issuing CDBC, according to the Atlantic Council, an independent organisation based in Washington, D.C. Nine of the countries -- The Bahamas, Nigeria, and seven countries in the Eastern Caribbean Union -- have already launched centrally governed digital currency.

Finance Minister AHM Mustafa Kamal in his budget speech for the current fiscal year (2022-23) said that as the risky use of virtual currencies such as crypto-currencies continued to grow worldwide, many central banks around the world were working to launch digital versions of their currencies as an alternative to crypto.

"The main purpose of launching Central Bank Digital Currency as a result of the time-befitting steps of the present government is that the coverage of the internet and e-commerce in the country has increased tremendously," he said.

Bangladesh Bank will conduct a feasibility study on the possibility of introducing CDBC in Bangladesh, he mentioned.

Dr Habibur Rahman, chief economist of the Bangladesh Bank, told the FE in June that digital currency is the perfect solution to the wiping-off losses that happen on account of shortage of smaller-denomination currencies.

"Our aim is to introduce digital currency as it will resolve this type of problem," said Dr Rahman.

But introduction of such currency in Bangladesh is perceived to have many challenges. Basic one is the limited access to internet. Apart from this, many citizens will try to dodge the newest technology-based currency as evading taxes is hardly possible through systems. Taxmen or tax administration will be able to watch every earning and spending or inflow into and outflow from their accounts.

Habibullah N. Karim, the founder & CEO of Technohaven Company Ltd., told the FE that the finance minister had actually mentioned two issues: conducting study on the cryptocurrency and the central bank digital currency. Both are timely uttered in the budget speech.

"To my mind, digital currency may be the right solution for resolving the fastest disappearance of the smaller coins and notes."

He mentioned that even Poisa-1 may come again.

Mr. Karim, also former chief of the BASIS, an apex body of software and IT-enabled service industry, assures that such digital currency will be very much easy to use.

But, he mentioned some challenges for its launch in Bangladesh. They are (1) The related law in Bangladesh needs to be amended for introducing the currency, (2) creating digital identity, which he believes is time- consuming as Canada took seven years to do it and (3) developing a culture on such currency which is very much important.

Hussain M Elius, former CEO of Pathao, the first major ride-sharing company in Bangladesh, told the FE that CBDC consists of two components -- one is wholesale CBDC and another retail CBDC. The wholesale CBDC is very much popular in many economies, including Singapore and the UK. This is transaction between banks. But in the retail CBDC people need to be connected with the central bank through apps or any other way.

The main advantage is that it is less costly and faster. But he mentioned a painful truth of the currency: there will be no privacy. "What I consume and what I earn and how much I earn -- everything will be visible to the central bank," Mr. Elius says explaining the flip side of such decentralized finance or defi.

"It is somewhat anti-democracy type." China has much achievement on the retail CBDC.

Masud Biswas, director-general at the Bangladesh Financial Intelligence Unit or BFIU, the central agency to fight against money laundering, terrorist financing and the financing of proliferation of weapons of mass destruction, says: "The digitisation is a more transparent solution as the authority can monitor it."

"In my belief, although this is a very initial stage in Bangladesh but it will ensure more transparency in transaction and accurate accounting," he told the FE about the merit of the switch.

He, however, makes it clear that CBDC is not cryptocurrency. Crypto, actually digital assets-based on blockchain technology, has even generated divisions in Europe and is not law of the land.

jasimharoon@yahoo.com