Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

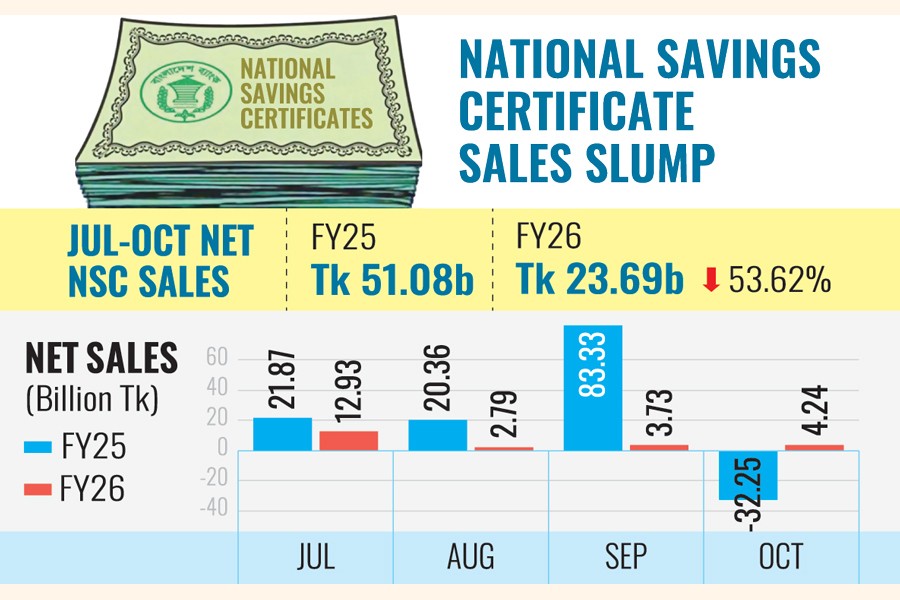

The net sales of National Savings Certificates (NSCs) experienced a staggering 53.62-percent year-on-year decline during the July-October period of the current fiscal year.

The sharp downturn reflects tightening liquidity conditions and a persistent rise in living costs that continue to sap the capacity of small investors to park funds in government instruments.

According to the latest Bangladesh Bank (BB) data, the net NSC sales plummeted to Tk 23.69 billion in the first four months of FY26, down significantly from Tk 51.08 billion recorded during the same period in FY25.

Analysts attribute this dramatic slide to a "perfect storm" of economic pressures, primarily mounting inflationary heat and a squeeze on disposable income.

While the overall four-month trend remains bearish, October 2025 provided a rare glimmer of recovery.

The net sales for the month reached Tk 4.24 billion, a marked improvement from the Tk 32.25 billion deficit (negative growth) recorded in October 2024.

However, the broader quarterly performance underscores the volatility.

In the July-September window of FY26, the total net sales stood at Tk 19.45 billion - a 52.60 per cent drop from the Tk 41.09 billion logged in the corresponding quarter of the previous fiscal year.

The central bank data reveals the slump began in July 2025, with sales falling to Tk 12.93 billion - a 41.0 per cent year-on-year decline from the Tk 21.87 billion recorded in the same month last year.

The situation worsened in August as sales crashed to a mere Tk 2.79 billion, a staggering drop compared to the Tk 20.36 billion parked in the same month of the previous year.

The decline reached its nadir in September, recording a massive 95.5 per cent year-on-year plunge.

The net NSC sales dropped to Tk 3.73 billion in September 2025, down sharply from Tk 83.33 billion registered in the same month a year earlier.

This collapse highlights a deepening liquidity crunch and a shift in investor sentiment, as the once-popular government savings tools struggle to compete with other options.

The central bank data further reveals a contraction in the government's overall debt liability through these instruments.

The total outstanding balance of savings certificates stood at Tk 3.41 trillion in October 2025, representing a 2.85 per cent decline.

Dr Masrur Reaz, chairman of Policy Exchange Bangladesh, says the sharp fall in the NSC sales reflects severe pressure on household finances amid high inflation and tight liquidity.

"With real incomes eroded, small savers are prioritising daily expenses over long-term savings," he says, adding that reduced effective returns and stricter compliance have further weakened the appeal of NSCs.

He notes that unless inflation eases and confidence improves, retail savings instruments will continue to struggle as a reliable source of government borrowing.

The cooling interest in the NSCs is also linked to a revised interest rate structure and stricter regulatory oversight.

Currently, the five-year Bangladesh Savings Certificate offers 11.83 per cent for investments of up to Tk 0.75 million, with rates slightly lower for higher slabs.

Crucially, the effective first-year return has been trimmed from 10.13 per cent to 9.74 per cent.

Furthermore, the National Savings Certificates Online Management System, launched in 2019, continues to act as a deterrent for institutional or high-value speculative buyers.

By making e-TINs and National ID cards mandatory, the government has successfully curbed the misuse of these tools, though it has also resulted in lower aggregate sales volume.

While FY25 showed some resilience - closing with a deficit of Tk 60.63 billion compared to the massive Tk 211.24 billion in FY24 - the early data for FY26 suggests the government may face challenges in meeting its internal borrowing targets through these retail instruments.

sajibur@gmail.com