A complex economic situation - at both national and global levels- is now prevailing. Bangladesh is now going through one of the most difficult macroeconomic situations in recent decades. The country is facing a number of transitional challenges: graduation from the Least Developed Country (LDC) category, delivery of Sustainable Development Goals (SDGs), completion of the Eighth Five-Year Plan (8FYP) and Perspective Plan (2021-2041), and emerging geostrategic issues. Against the backdrop, the upcoming national budget and expectations of the disadvantaged citizens and community deserve some serious attention.

At this testing time, three major manifestations of current challenges that need to be addressed may be highlighted. These are: (a) Unabated Inflation; (b) Snowballing Debt Risk; and (c) Slowdown of Economic Growth.

UNABATED INFLATION: As of March this year, inflation remains over 9 per cent for the 13th consecutive month. There is an actual erosion of the purchasing power of low- and fixed-income class, which may be much higher than average official statistics.

Underlying factors of unabated inflation include monetary expansions in terms of high growth of credit; sharp depreciation of local currency against US Dollar; government borrowing from the central bank to finance the budget deficit; irregularities within the banking sector; non-competitive market (or oligopolistic behaviour) coupled with market manipulations by vested interest groups; and high cost of production due to upward adjustments of administered prices of fuel and electricity.

There are a number of implications of high inflation for the left-behind communities. These are: disproportionate impact on middle- and low-income households; erosion of purchasing power or real wage; dissaving and depletion of assets; increased indebtedness; reduced non-food expenditures such as clothing, health, education, utility services, and recreation; and heightened food insecurity and changed food habits. Moreover, working overtime, taking up secondary occupations coupled with discontinuing children's education and involving them in paid work, and early marriages of girl childrenare also some of the coping mechanisms for left-behind communities to fight inflation.

The government has announced a number of measures to rein in inflation. These include increasing policy rates by the central bank, replacing interest rate caps with "SMART" rates, containing private sector credit growth, injecting US dollar absorbing liquidity from the local market, and ceasing government lending via money creation. The government also goes for import restrictions to avoid accelerated depreciation, downward adjustment of tariff rates for selected commodities, broadening of social protection schemes including Open Market Sales (OMS) and introduction of Family Card; episodic commodity market monitoring by the consumer rights authority.

Now, the key question is what to do to contain the inflation. This paper recommends the following: implementing the market-determined interest rates; allowing the exchange rate flexibility; limiting the government borrowings; ensuring the sufficient supply of essential items in the market - exploring alternative import sources; and preventing irregularities and manipulations in domestic market, including anti-competitive practices, introducing Agricultural Price Commission; incentivising the farmers and continuing subsidy for agricultural input and irrigation, controlling the interest rates spike specifically to LNOB loans; expanding social protection schemes to all districts, including OMS and public works programmes, as well as expanding income-tax-free limit for low and low-middle income people to protect their disposable income.

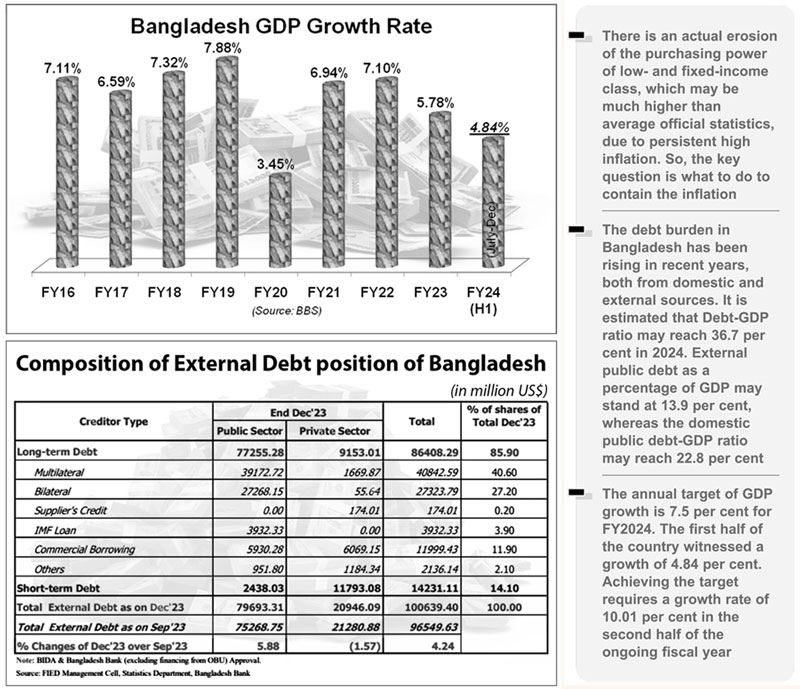

SNOWBALLING DEBT RISK: The debt burden in Bangladesh has been rising in recent years, both from domestic and external sources. It is estimated that Debt-GDP ratio may reach 36.7 per cent in 2024. External public debt as a percentage of GDP may stand at 13.9 per cent, whereas the domestic public debt-GDP ratio may reach 22.8 per cent. External private debt is also estimated at 5.13 per cent of GDP.

There are several underlying factors behind rising debt. These include persistently low revenue generation that has kept it around 9 per cent of GDP, sharp depreciation of Bangladesh Taka leading to a higher debt servicing liability, high cost of public investment projects (inflated pricing), project time and cost overruns risking debt repayment beginning earlier than expected in the project cycle, rising cost of borrowing from both domestic and external sources, and growing underutilised loans adding pressure on balance of payments (BOP).

The rising debt has some serious implications for the economy. It leads to growing reliance on borrowing for debt servicing liability (principal and interest). Debt servicing as a percentage of revenue and grants was below 70 per cent and is now projected to exceed 100 per cent in 2024, according to the International Monetary Fund (IMF). The government had no revenue surplus and had to borrow to repay foreign loans. The government borrowed Tk 57.55 billion in FY2022 for the amortisation of foreign loans as the revenue could not cover the entire payment requirement, which was programmed to increase to Tk 154.99 billion in the budget for FY2024. The entire Annual Development Programme (ADP) is now financed by borrowed resources.

Moreover, fiscal space is shrinking as debt servicing (as a percentage of revenue) is estimated to jump in 2024, leading to lower available resources for public service delivery and support to disadvantaged citizens in a difficult time. Lower available budgetary resources may lead to insufficient resources for public service delivery and public investment. This may result in dampened prospects for medium-term development outcomes (e.g., SDGs, particularly for disadvantaged groups). Dampened employment opportunities, risking increased income and food insecurity disproportionately impacting disadvantaged households.

Again, there is an increase in borrowing from costlier sources with stringent loan terms and conditions. The government relied heavily on borrowing from commercial banks, risking crowding out the private sector when liquidity space is quite low. The risk of downgraded credit ratings can discourage foreign direct investment (FDI) and result in limited financing access. Indeed, there is also a multifaceted pressure on BOP.

To address the growing pressure from rising debt, the government has reduced or withdrawn subsidies in various sectors, including power and energy. Measures are taken to keep power and energy supply below the capacity level and delay payments against foreign exchange liabilities for both public and private sectors, including about US$5 billion in unpaid foreign dues for energy purchase. The government also requested delays for two years to repay foreign loans for the Rooppur Nuclear Power Project.

The government also sought more budgetary support from the development partners, who agreed to implement policy reforms. Import restrictions have also been imposed, so import payments dropped by 15.36 per cent in the first eight months of the current fiscal year. Bangladesh Bank declared a "crawling peg" exchange rate fixing system (following IMF prescription) and removed the interest cap on bank deposits, introducing SMART interest rate. Steps were taken to inject funds by the central bank into commercial banks amid the volatility call money market. The government is also trying to increase non-concessional borrowing and has adopted a restrained approach to releasing funds for public investment projects.

To reduce the debt-related risks, this paper proposes a set of recommendations. These include prioritising the enhancement of domestic resource mobilisation through taxation, accurately estimating debt service obligations by taking note of possible depreciation in the coming months, strengthening the good governance of public investment projects, and improving the capacity for loan negotiation.

Close monitoring of foreign borrowing by the private sector is also necessary, along with exploring alternative sources of funds and diversifying sources of development finance. It is critical to consider the revenue and foreign exchange generation capacities of the foreign loan-financed public investment projects while taking up a project. The concerns regarding the risks of currency mismatch and time-period mismatch should also be taken into cognisance. The government also needs to take advantage of opportunities to use currency swap facilities wherever possible.

SLOWDOWN OF ECONOMIC GROWTH: The annual target of GDP growth is 7.5 per cent for FY2024. The first half of the country witnessed a growth of 4.84 per cent. Achieving the target requires a growth rate of 10.01 per cent in the second half of the ongoing fiscal year. It may be recalled that the IMF cut the projection for economic growth rate to 5.7 per cent for the current fiscal year.

Factors behind the slowdown in economic growth need to be reviewed. As contractionary monetary policy has been followed to contain inflation, it has also slowed the pace of the economy. Power and energy supply has also been disrupted due to foreign exchange and fiscal space constraints. Restrictions on imports were applied, and a restrained approach was pursued for public expenditure, which also contributed to this slowdown. It may be noted that manufacturing sector growth slowed down and went into negative terrain in the second quarter of the fiscal year.

The gross export earnings growth is also slowing down- declined from 6.7 per cent in FY2023 to 3.9 per cent in FY2024 (during the July-April period) against the annual target of 11.6 per cent. During the July-February period of the current fiscal year, import payments experienced a notable decline of 15.17 per cent. Investment as a percentage of GDP decreased to 30.95 per cent in FY2023 from 32.05 per cent in the previous year. Private investment remained stagnant at around 23-24 per cent of GDP, however, it slightly decreased in FY2023 compared to the previous year. FDI in FY2023 was 9.74 per cent lower than the previous year, which has remained stagnant at 0.4 per cent of GDP.

Again, public investment decreased to 6.77 per cent of GDP in FY2023, down from 7.53 per cent in the previous year. During the July-March period of the ongoing fiscal year, the ADP implementation rate stands at 42.30 per cent. So, the remaining three months require a 57.7 per cent implementation rate to meet the target. In recent years, domestic savings as a percentage of GDP have hovered around 25 per cent, while national savings have been around 30 per cent without much improvement.

There are multiple implications of economic slowdown. Opportunities for decent jobs have declined, though the government has set a target to employ an average of around two million people annually throughout 2030, as outlined in their Election Manifesto (2024). In 2023, only 0.5 million jobs were created, although about 1.3 million people went for overseas jobs. In addition, Bangladesh's recent BBS Census and Household Census Report-2022 paints a concerning picture of youth inactivity. It says among approximately 31.6 million young people (aged 15-24), 40.67% are classified as inactive, meaning they are NEET.

Economic slowdown may affect poverty alleviation. The government has set a target to reduce the poverty rate to 11 per cent by 2028, as outlined in their 2024 Election Manifesto, requiring a per capita real GDP growth of around 7.50 per cent each year (assuming income inequality remains constant), which is now a formidable task.

The vulnerability of the non-poor people in the face of the high rise in commodity prices has also increased. Domestic revenue mobilisation target is likely to be missed by a large margin. Foreign investment prospects are facing challenges. Structural transformation of the economy, in terms of production and employment, is inhibited.

As the government pursued a contractionary monetary policy, restrained fiscal stance and restrictions on imports with a view to establishing the macroeconomic discipline, it had a limited arsenal to counter the slowdown of the economic growth. But it has made some efforts. Subsidies for agricultural inputs, tax incentives for export-oriented sectors, and fiscal incentives for remittance inflow continued.

Evidently, the government has to embrace subdued economic growth to achieve macroeconomic stability. Hence, ensuring more equitable economic growth favouring disadvantaged population groups and creating decent jobs is critical. To enhance economic growth, the government needs to expand incentives to the agriculture sector to ensure food security and protect the purchasing power of the low- and middle-income population groups. Ensuring energy security for the utilisation of production capacities is necessary. Extended concessional loans to the CMSMEs and continued public investments for enhancing productivity and skill development are also important.

END NOTE: The government needs to restore macroeconomic stability, promote economic diversification by revisiting the incentive structure, protect small businesses and low-income people while revising tax incentives, curb corruption to reduce the cost of doing business, make efforts to find new markets for exports and avoid the influence of vested groups in policy adjustments are some of the key tasks the government needs to accomplish.

While preparing the national budget, the government should pursue the following to ensure the delivery of the budget for attaining the policy objectives:

- Take a cautious and sensitive approach to avoid any negative policy spillover and protect the interest of disadvantaged communities and smaller businesses while making macroeconomic adjustments.

- Safeguard policy adjustments and reforms from influences of the oligarchs and maintain zero tolerance against corruption and illicit financial outflow.

- Protect the purchasing power of low and fixed-income groups by giving them income tax reliefs, expanding social protection (including public works programmes) coverage and allowances and ensuring stringent market monitoring.

- Prioritise domestic resource mobilisation to expand fiscal space by curbing tax evasion and ensure value for public money in taking new investment projects as well as implementing the existing ones.

- Strengthen transparency, participation and oversight in the budget delivery process.

- Make scope for the local level citizens to be involved in budget delivery and monitoring process, including selecting participants of social protection programmes and implementing public investment projects to reduce leakages and corruption.

- Ensure disaggregated budget reporting using real-time data at the national parliament under the Public Money and Budget Management Act 2009.

- Use the built-in safety measures at the administrative level to keep fiscal discipline.

- Ensure strong leadership and coordination among the government agencies while devising and implementing policy decisions.

- Ensure regular monthly meetings of the critical parliamentary committees related to public finance management, such as Standing Committees on Ministry of Finance, and Ministry of Planning, Public Accounts Committee, Committee on Estimates and Committee on Public Undertakings, with opportunities for public hearings involving relevant stakeholders and citizens groups as well as briefings by amici curiae.

Dr Debapriya Bhattacharya is Distinguished Fellow, Centre for Policy Dialogue (CPD) and Convenor, Citizen's Platform for SDGs, Bangladesh. deb.bhattacharya@cpd.org.bd. Mr Towfiqul Islam Khan is Senior Research Fellow, CPD. towfiq@cpd.org.bd

Research support has been provided by Najeeba Mohammed Altaf, Mamtajul Jannat, and Shourza Talukder, research associates of CPD; Naima Jahan Trisha, Rushabun Nazrul Yaanamu, and Arman Shaid, programme associates of CPD.