Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

Although banks and financial institutions are the late embracers of Artificial Intelligence (AI), the banking industry has seen a massive change in the past decade due to the revolutions of AI. Banks are axing the number of physical branches while investing highly in innovations. Spanish-owned bank Santander announced on January 23 that it would close down more than 140 branches across the UK putting 1270 jobs at risk. [The first banks will close on April 25 with the latest shutting shop on December 12.] AI is completely reshaping the way people expect banks to give them full freedom and peace of mind. AI can take care of the repetitive tasks that most of the bankers do at work every day and give them the scope to focus on something more creative. AI and Machine Learning (ML) can provide the following services to the bank consumers:

1. PERSONALISED PRODUCTS: Live personnel sitting behind a counter for providing banking services will soon become a thing of the past; advanced AI help banks create a more human-like customer experience. AI can efficiently analyse big data and customer insights, which help banks to create a more personalised customer experience. AI and ML can track the customers' spending habit, it can also help budget efficiently and alert the consumers if they spend too much.

A matured AI tool can wisely measure the credit worthiness of a consumer based on the customer's spending and earning behaviours. If the machine is fed with data points including historical data, credit policies, risk appetite, various rules, regulations, eligibility criteria and complex scenarios, it can then make autonomous credit decision in a matter of seconds analysing the vast volume of the data.

Also, the same tool can compare the types of credit plans and present the customer with the most suited credit plan for the customers, in short, AI outcomes can be more customer oriented than product/service oriented. Furthermore, the AI tool can also alert the consumer on the upcoming direct debits, standing orders or when the account balance is below a certain amount so that the consumer can plan his/ her financial future wisely.

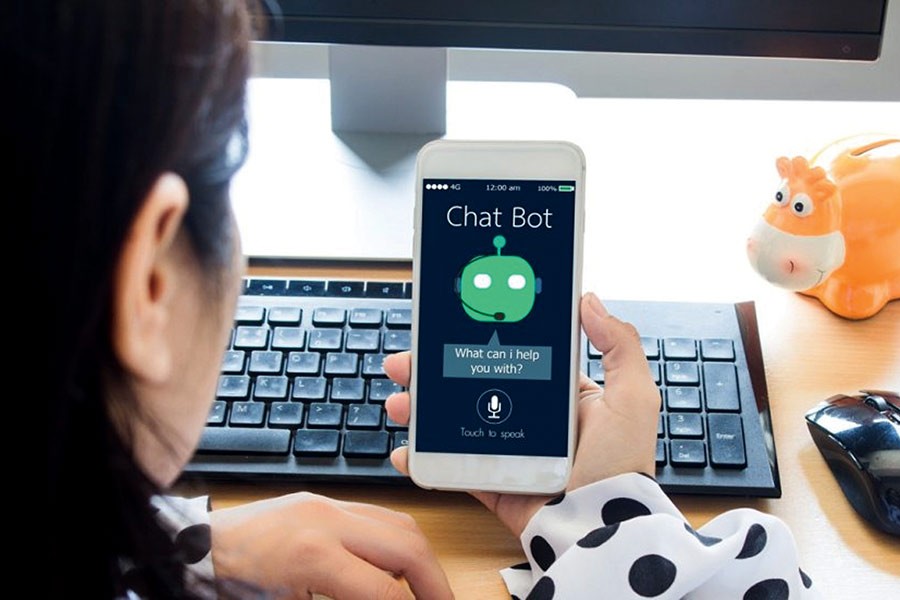

2. CHATBOTS: People often go to bank branches or phone the banks for different queries. If they are lucky they get the chance to talk to a customer service representative instantly, otherwise they are to wait for long to talk to them. Such waiting is boring as well as time wasting. Now machines are smart enough to interact like human customer service representative and customers can have access to them instantly. These artificial intelligence-based communication tools are known as chatbots, which can interact in natural language. These tools can give information or can perform a task ordered by the user -- like Apple's Siri, Amazon's Alexa or Google Assistant. The beauty of AI-based chatbots is that by artificially mimicking the patterns of human interactions, these can learn by themselves without programming natural language process. Every new experience is a learning point for them.

More and more financial institutions are now introducing chatbots for serving the tech-savvy customers and to reduce the cost of manpower substantially. Many banking organisations even name their chatbots like human representative - Bank of America call their chatbot Erica, HSBC named it Amy and the fintech unicorn Revolut name theirs Rita. These chatbots can smoothly handle the basic queries and orders like balance inquiry, fund transfer etc. Chatbots can help the banking industry in many ways, for instance-

Cost reduction: Chatbots are currently saving $20 million globally every year and it is believed that the banking industry will save over $8 billion annually by 2022. Unlike their human counterparts, Chatbots do not demand monthly salary. While a paid employee can handle one customer at a time, a chatbot can respond to unlimited customers' queries at a time.

Available 24/7: Chatbots never sleep, they are always ready to answer customer questions or perform the necessary task. On an average, a customer waits four minutes on phone to be connected with the call centre but customers can immediately get a response from a chatbot. According to the Business Insider Intelligence research, use of chatbots for customer service can reduce up to 30 per cent costs for communication with customers.

Quicker issue resolution: Consumers don't just want a response, they want action. A bot can help from answering a question to assessing contract data for faster solutions. COIN -- JPMorgan's bot -- is capable of analysing complex legal contract so fast and efficiently in seconds that would take 360,000 hours for the human lawyers.

3. ROBO ADVISORS: Robo advisors are automated, algorithm-based portfolio management tools that require no or minimum human intervention to provide a simple, intelligent investing option for investors from novice to highly experienced. Robo-advice is expected to reach a staggering $1.5 trillion in assets by 2020; the biggest slice of the pie will come from the millennial. This AI tool is very attractive to new investors due to affordability, transparency, and simplicity.

This new trend in portfolio management is forcing traditional players to reshape their front-line services leveraging the benefits that the AI tool offers. This all-in-one nature of Robo poses a threat to the incumbent banks. Banks can take a strategic move to offer their customers automated investments services using robo-advisors along with their other services such as payment, mortgage, and loan advice and so on from the same platform. Consumers often prefer to take investment and banking services from the same provider. A study conducted by Novantas revealed 45 per cent of the customers prefer their primary banks to cater to their investment needs. This demand of the customers can be easily fulfilled by the broad-minded banks that are willing to work together with other start-ups in collaborations with fintech companies. This type of collaboration and partnership is known as 'platformification'. Platformification can help the incumbent banks to get more customers and scale up their operations.

4. FRAUD DETECTION: Fraud is as old as human civilisation; the advancement in technology has made fraud more difficult to tackle. Modern technology is used by both the fraudsters and the regulatory bodies these days. The good news for the good people is that the new neural networks can help identify fraudulent activities and stop them before a fraud takes place.

The cost of compliance for banks is ballooning year by year. Banks are trying hard to make sure they have sufficient safeguard in place to tackle any fraud or money laundering. The model for risk categorisation is changing. Banks typically segment their customers by industry, business type, size etc. In this method banks apply some rules that worked in the past. However, the problem with this approach is that these segments do not consistently represent groups of entities with consistent transaction behaviour. Banks have a large volume of customer data along with the transactional data. By analysing these readily available data, AI can identify customer's behaviour pattern and can flag transactions that fall outside of the customer's usual behaviour pattern. This will substantially reduce the number of false positives banks usually receives every day from their traditional systems. Mastercard has already implemented an AI tool that fits different customers and transactions into the best-suited clusters for an accurate comparison. As the habits of customers change, the AI tool automatically adjusts itself with the spending habit of the customers to find out potential fraudulent transactions.

Analysing the large volume of public and private data, an AI tool can easily identify complex fraud patterns and complex criminal activity occurring across different products, business models and so on. If the tool detects any fraud, it can communicate with the human compliance officer for in-depth check or the tool can automatically submit a Suspicious Activity Report (SAR) to the regulatory body.

Data from Statista shows smartphones had 83 per cent market share in 2018 and according to a survey by the Office for National Statistics, 69 per cent of UK's population used internet banking in the same year. The bitter truth is people now spend more time on their phone screens than their family members; as a result, service providers are focusing more to have a vibrant presence on the mobile platform. In the near future, it will not be surprising to see banks recruiting more data scientists than actual bankers.

Nazmul H Azad Mishu is CEO, Southeast Financial Services UK Ltd

(A subsidiary of Southeast Bank Limited) mishu_bc@yahoo.com