Expanding & diversifying exports to the UK

Mohammad A Razzaque, Deen Islam, Jillur Rahman and Abu Eusuf

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

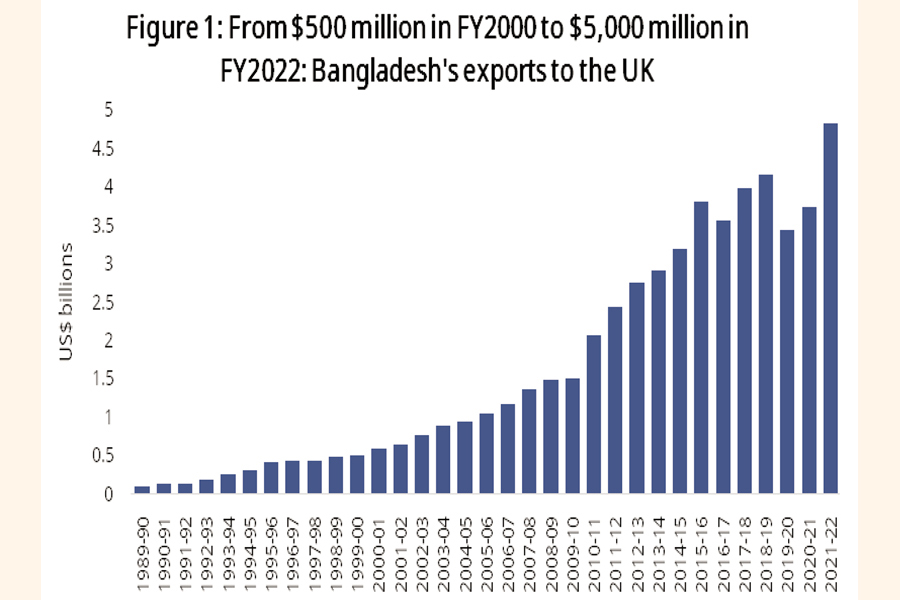

Bangladesh and the United Kingdom (UK) have a longstanding and multifaceted relationship with a strong focus on trade and economic cooperation. Utilising duty-free market access and relaxed rules of origin (RoO), Bangladesh's UK-bound exports expanded from US$500 million in FY2000 to about $5 billion in FY2022. As the third largest export destination, the UK accounts for more than 9 per cent of Bangladesh's total merchandise exports. More than 90 per cent of these exports comprise apparel products, reflecting Bangladesh's heavy reliance on a single product for export.

There are tremendous opportunities for expanding exports to the UK further-not only of garment items but also other products. The recently announced Developing Countries Trading Scheme (DCTS) of the UK can be a catalyst in boosting exports of non-garment items, while the continued duty-free access under DCTS is set to help Bangladesh's clothing exports to the UK grow even after its Least Developed Country (LDC) graduation.

UK DCTS AND BANGLADESH: The UK has introduced its preferential trading scheme for developing countries, called the Developing Countries Trading Scheme (DCTS), marking its departure from the EU's Generalized System of Preference (GSP). The DCTS could be a game changer for maintaining export competitiveness in apparel items and promoting non-apparel items for export diversification. The DCTS offers significant improvements over those offered under the previous UK system and the EU GSP scheme that can benefit Bangladesh. These include:

• Under the new scheme, Bangladesh as an LDC enjoys duty-free market access through the DCTS Comprehensive Preferences. After its LDC graduation in November 2026, Bangladesh will continue to enjoy the same LDC benefit for another three years (until November 2029).

• As an LDC, Bangladesh also stands to benefit from more generous UK Rules of Origin (RoO) requirements. The minimum value-added requirement for LDC non-garment products has been reduced to 25 per cent from 30 per cent under the previous GSP.

• LDC textile and clothing exports to the UK will continue to benefit from the single-stage transformation.

• The UK DCTS offers relaxed and liberal product-specific rules and extended cumulation facilities, allowing inputs to be imported from 95 countries and yet the LDC manufacturers of final products being eligible for duty-free exports.

• The DCTS removes the requirement for countries to ratify and implement certain international conventions as a precondition for trade preference. It also abolishes the safeguard measures on certain sectors under the previous regime and has scrapped the provision of product graduation events if some products of beneficiary countries enjoy a high market share.

• After LDC graduation and an additional three-year transition period, Bangladesh will get duty-free benefits in more than 85 per cent of its UK-bound product lines under DCTS Enhanced Preferences.

• However, RoO requirements for Enhanced Preferences will be similar to the previous GSP regime (i.e., 50 per cent value addition for most non-textile products and a double-stage transformation for apparel items).

• The UK has specified more liberal product-specific rules (PSRs) only for LDCs. Almost all chapters have alternative PSRs.

IDENTIFICATION OF POTENTIAL PRODUCTS FOR EXPORT DIVERSIFICATION: DCTS preferences provide predictable and sustained market access benefits, thereby boosting the potential to diversify Bangladesh's export basket in the UK. In-depth research was undertaken by Research and Policy Integration for Development (RAPID) using quantitative methods and highly disaggregated trade data in analysing Bangladesh's current production and export structures, competitive advantage, comparator countries' specialisation, and market shares in the UK vis-à-vis Bangladesh, and product-space proximity to currently exported items seems to suggest leather goods and footwear, light engineering, agro-and food processing and fish and shrimp are prominent non-garment export sectors that should be able to unleash their export potential with the help of right policy support.

Bangladesh's leather goods exports to the UK in FY22 were only US$3 million, which holds a negligible 0.1 per cent share of the UK's total imports of such products (over $3 billion). Similarly, Bangladesh earned $34 million from exporting footwear to the UK, capturing a paltry share of just 0.6 per cent of the $5.2 billion UK market of imported footwear.

In FY22, Bangladesh exported engineering products worth $47.5 million to the UK, which is only 0.02 per cent of the UK's total imports of such products, amounting to over $327 billion. Bicycle is the most important light engineering product. Bangladesh is the fourth-largest exporter of bicycles (HS8712) to the UK, with exports worth $43.2 million in FY22, accounting for 9.9 per cent of the UK's overall imports of such products. While bicycle imports from the UK remained almost stagnant during 2017-21, Bangladesh recorded an export growth rate of 7 per cent.

Bangladesh's agro-food and agro-processed exports to the UK amounted to$52 million in FY22. This is less than 0.1 per cent of the $64 billion processed food imports to the UK. During 2017-21, the UK's imports of processed food increased by 0.7 per cent per year on average, while imports of the same products from Bangladesh increased by 29 per cent.

In FY22, Bangladesh exported fish worth $63 million to the UK, accounting for 2.2 per cent of the $2.9 billion market. Despite the UK's overall fish imports increasing by 1.0 per cent during 2017-21, Bangladesh experienced a decline in average growth of 4 per cent in exports to the UK, with its total fish exports shrinking by 6 per cent. Major suppliers such as India, Sweden, and Denmark also posted negative growth in fish exports to the UK. The duty-free access of Bangladesh under Comprehensive Preferences can help fish exports to expand.

CONSTRAINTS AND CHALLENGES FOR EXPORTING TO THE UK: The opportunities for Bangladesh to expand exports are high due to the large demand and duty-free access to the UK. However, several constraints impede this potential. These constraints can be grouped under three broad areas: export market-specific issues, political economy and policy factors, and supply-side obstacles.

Market-specific issues.

• Consultations with the exporters and manufacturers reveal that a lack of knowledge and information about the UK market impedes expanding exports of non-garment products. Bangladeshi exporters encounter difficulties comprehending the evolving demand, the market size for specific products, potential competitors, and regulatory requirements. Limited resources for conducting market research, exploring sales opportunities, and connecting with buyers are the problems faced by both established exporters to other markets as well as new exporters. Many Bangladeshi exporters remained uninformed about the duty-free market access and the extremely liberal rules of origin provided through the UK's DCTS. For example, some major footwear producers in Bangladesh inform in the consultation meeting that they are not aware of the export potential of their products in the UK market. Similarly, the producers of some light engineering products, such as consumer electronics, bicycles, and batteries, notify that they do not have enough information about market demand and potential competitors in the UK market.

• Bangladeshi non-apparel exporters are not well integrated with the UK supply chain. Most stakeholders report not being connected with the UK's big brands and retailers. This is seriously limiting exports of products, such as footwear and consumer electronics. For marketing most consumer electronics, after-sale service is a prerequisite. However, Bangladeshi exporters cannot afford to establish the necessary facilities to provide after-sale services.

• Bangladesh exporters face difficulties in complying with the UK's standard and certification requirements. Many manufacturers, especially small and medium-sized ones, do not have access to proper testing and certification facilities, and some large establishments need to source these certifications from abroad. Agro-food and processing sector faces critical challenges in obtaining the salmonella test certificate, which requires a lab with gamma-ray, and currently, there is no such facility in Bangladesh. Analogously, light engineering products require a certificate of environment and a certificate of the non-existence of harmful chemicals/materials in the products to gain entry into the UK market. Many exporters, especially small and medium exporters, could not source these certificates locally and spend a large sum of money to obtain them from a foreign lab.

• The perception of Bangladesh as a nation that manufactures low-quality products acts as a considerable obstacle in establishing export relationships. Many exporters in our consultation meeting, especially in agro-food and processing and light engineering sectors, informed us that importers in developed countries like the UK are generally not convinced about the quality of the products, even if the products are of high quality. As a result, Bangladeshi exporters of high-quality products often are offered lower prices, creating disincentives for Bangladeshi producers to export.

Policy and political economy factors

• With significant tariffs and para-tariffs in place to protect the import-competing local manufacturing sector, investment's relative profitability (and thus the incentive structure)is heavily skewed against the export sector (anti-export bias).This discourages investment into export-oriented non-RMG sectors.

• Reliance on import tariffs for government revenue means tariff rationalisation has proven to be a difficult task, sustaining the policy-induced anti-export bias. Like the garment sector, many non-garment industries, such as light engineering, use mostly imported inputs. A high import tariff on inputs used in these sectors makes exporting from these sectors less competitive.

• Requirements for product standards in the export of leather goods, agro-food and processed items, light engineering goods, and fish and fish products are much more stringent than domestic market sales. This problem is accentuated further by the difficulties associated with testing and certification procedures. Differential domestic and export sales standards also contribute to an incentive structure favouring import-competing sectors.

• Additionally, the lack of export incentives for non-RMG sectors is a significant obstacle to export diversification. Bonded warehouse facilities for duty-free import of intermediate input are limited to the garment sector and a few leather exporters. While duty drawback facilities are available, procedural delays make them less attractive.

Supply-side issues

• Bangladesh does not have sufficient supply capacity of non-RMG exports. Most small and medium-scale enterprises need to scale up their capacities to become more competitive. Several factors, including the need for technological upgrading, shortage of skilled workforce, etc., constrict export supply response.

• Lead time for Bangladeshi firms is perceived to be higher than those of their international competitors. Industries that use mostly imported inputs like light engineering face serious trouble shipping their products in time. Footwear exporters also need to import leather, chemicals, and other accessories. Exporters face a long lead time involving raw materials imports and exports of final products. UK buyers are discouraged because of the long delay in receiving the consignments.

• The lack of access to finance has been identified as one of the key constraints faced by the exporters. Small and medium-sized enterprises (SMEs) are particularly affected by it.

• The lack of specialised professionals and skilled workers is a major issue for firms focusing on exports, whether in the RMG or non-RMG sectors. This problem is especially severe for sectors, such as light engineering and leather footwear, where there is a significant mismatch between the skills of the available workforce and the skills required by employers.

• Infrastructural bottlenecks, such as inadequate transportation and logistics systems and energy shortages, add to trading costs and lead times, undermining competitiveness and hindering export growth.

POLICY RECOMMENDATIONS: Some policy recommendations to tap the UK market under the DCTS are as follows:

1. Dissemination of market-specific information (duty-free benefits, rules of origin provisions, required standards etc.) can help expand non-RMG exports to the UK. The ministry of commerce and other relevant stakeholders can play a critical role in disseminating relevant information and building awareness.

2. Promoting high-quality non-RMG products from Bangladesh in UK exhibitions and events and assisting exporters in participating in these events can help increase export orders.

3. Integration into UK supply chains and establishing relationships with big brands and retailers should be one of the most essential ingredients in increasing export sales in the UK.

4. Collaboration among Bangladesh authorities, trade organisations, and UK stakeholders such as private sector associations(with the support of the FCDO) can help establish the connection between exporters and importers. This can also help build awareness about various non-RMG export products of Bangladesh.

5. Improving productivity, upgrading technology, and ensuring compliance with product quality should be considered as priority issues to enhance the market share of non-RMG products of Bangladesh in the UK.

6. Enhancing the capacity of the existing standards authorities and institutions should be one urgent policy priority so that they can provide globally recognised certifications and necessary testing facilities to potential exporters locally at lower costs.

7. Deepening incentives for the identified export sectors can help achieve economies of scale and enhance export competitiveness in destination markets, including the UK.

8. Removing anti-export bias and rationalising tariffs are crucial in ensuring the profitability of exporting activities.

9. Prioritising power supply to export sectors and tackling infrastructural bottlenecks by reducing lead time and improving port efficiency are critical for enhancing the competitiveness of non-RMG exports.

10. Ensuring access to low-cost finances for the export sectors and their backward linkage sectors is essential to increase the scale of operation and expand exports.

11. Improving productive capacity for the non-RMG sector is necessary for export promotion and diversification. Bangladesh should seek additional UK technical and financialassistanceand make the most of all available supportto improve productive capacity and adopt cutting-edge technology and modern business practices.

Dr Mohammad A Razzaque, Chairman of RAPID, m.a.razzaque@gmail.com; Deen Islam, Associate Professor of Economics at Dhaka University and Research Director at RAPID; Jillur Rahman, Assistant Professor of Economics at Jagannath University and Associate Director at RAPID, jillurrahman@econdu.ac.bd; Dr Abu Eusuf, Executive Director of RAPID and Professor of Development Studies at Dhaka University.

[Research support was provided by Rakin Zaman, Sharjita Chowdhury, and Sumaeya Akhter]