Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

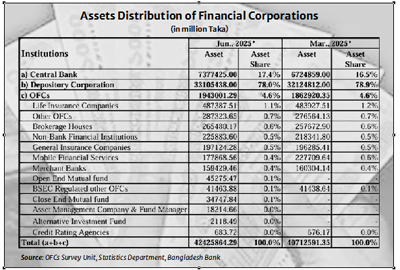

To improve the quality of financial statistics, Bangladesh Bank has started conducting quarterly surveys on Other Financial Corporations (OFCs). The first report has been released, presenting the sector’s status by the end of fiscal year 2024-25 (FY25). The findings show that the sector remains small, accounting for less than 5 per cent of financial corporations’ total assets in Bangladesh. Depository corporations hold the largest share at 78 per cent, followed by the central bank with 17.50 per cent.

“The OFCs survey is a key initiative aimed at strengthening institutional coverage for the preparation of robust monetary and financial statistics (MFS),” said the report. It is also necessary to comply with the International Monetary Fund (IMF)’s standards set out in the Monetary and Financial Statistics Manual and Compilation Guide (MFSMCG) 2016.

It is to be noted that, as per the definition of the Bank for International Settlements (BIS), a financial corporation is an ‘entity that is principally engaged in providing financial services, such as financial intermediation, financial risk management, or liquidity transformation.’ Financial corporations broadly include three entities: central banks, banks, and non-bank financial corporations. According to the United Nations Statistics Division (UNSD), the nine core subsectors of financial corporations are: the central bank, deposit-taking corporations except the central bank, money market funds (MMF), non-MMF investment funds, other financial intermediaries except insurance corporations and pension funds, financial auxiliaries, captive financial institutions and moneylenders, insurance corporations, and pension funds.

In Bangladesh, OFCs are broadly divided into three categories: Insurance Institutions, Securities Market Institutions, and Specialised Financial Institutions and Mobile Financial Services (MFS) providers.

The first type of institutions, general and life insurance companies, are supervised by the Insurance Development and Regulatory Authority (IDRA). Currently, 45 general and 33 life insurance companies operate in the country.

The second type of institutions is regulated by the Bangladesh Securities and Exchange Commission (BSEC). These include merchant banks, open end mutual funds, close end mutual funds, asset management companies and fund managers, alternative investment funds, credit rating agencies, brokerage houses, and other BSEC-regulated OFCs such as Central Depository Bangladesh Limited (CDBL), Chittagong Stock Exchange (CSE), and Dhaka Stock Exchange (DSE).

The third type of institutions, such as non-bank financial institutions (NBFIs), mobile financial services (MFS), and other OFCs, are supervised by Bangladesh Bank. Other OFCs include Bangladesh House Building Finance Corporation (BHFC), BB Equity & Entrepreneurship Fund (EEF), BB Grihayan Tahbil & Fund Management, Palli Karma-Sahayak Foundation (PKSF), and Small & Medium Enterprise Foundation (SMEF). However, the last two entities are not supervised by the central bank. The Ministry of Finance and the Ministry of Industry regulate these entities, respectively.

Almost all OFCs are non-deposit-taking financial institutions, meaning they are not allowed to collect deposits from the public, unlike commercial banks. Only NBFIs can mobilise medium or long-term fixed deposits.

The central bank surveyed 768 OFCs by sending questionnaires to collect data on assets and liabilities. Of these, 549 responded within the deadline. It means the status of about 30 per cent of the country’s OFCs is not captured in the initial report.

Bangladesh Bank began collecting and compiling statistics on OFCs a few years ago. At the end of FY18, the central bank compiled data on the assets of 151 OFCs out of 771 financial institutions. For the first two and a half years, the statistics were compiled on a half-yearly basis; since December 2020, they have been compiled quarterly.

Nevertheless, poor responses from existing OFCs make it difficult to present a broad picture of the sector. At one point, the number of regular respondents fell below 100, reflecting the indifference of other financial institutions to provide timely data. The situation began to improve in June 2023 when more than 200 institutions submitted the required data on time. In June last year, over 450 institutions provided their data, prompting the central bank to release the survey report to the public.

The central bank itself acknowledges that the report provides a partial yet meaningful picture of the sector. “Once the full-scale data of all OFCs are incorporated, a comprehensive view of the financial corporation landscape will emerge. Such a complete picture will deepen researchers’ understanding of the sector and support policymakers in identifying risks and formulating more effective policies,” it continued.

According to the survey, the total assets (adjusted) of OFCs stood at Tk 1.94 trillion at the end of June 2025 which was Tk 1.86 trillion at the end of March 2025. Thus, total assets of the OFCs increased by around 4.30 per cent during the quarter under review.

Assets of the depositary corporations, commercial banks to be precise, stood at Tk 33.10 trillion at the end of FY25 against Tk 32.12 trillion at March-end last year. Accumulated assets of the central bank reached Tk 7.38 trillion at the end of June last year.

Life insurance companies hold one-fourth of the total assets of the OFCs in the country, whereas general insurance companies held 10.10 per cent at the end of June last year. The share of brokerage houses stood at 13.70 per cent during the period under review, followed by NBFIs (11.60 per cent), MFS (9.20 per cent), and merchant banks (8.20 per cent).

Though the overall share of OFCs in the country’s financial sector is small, the variety of these institutions shows the sector is diverse and has the potential to grow. As the economy grows, demand for diverse financial services is increasing. Instead of relying solely on the banking sector, it is necessary to provide services through specialised financial institutions. This will reduce the risk of non-performing loans (NPLs) in the future and enhance competition. Continuing the survey is also necessary to develop a repository of all these financial institutions with proper classifications. Government and other regulators should push the OFCs to provide data and information as needed by the central bank to make the repository comprehensive.

asjadulk@gmail.com