Climate change has become a grave concern worldwide as there is no way to prevent or avoid it. The consequences of climate change are the rise in temperature, intense droughts, water scarcity, severe fires, rising sea levels, flooding, melting polar ice, catastrophic storms, and declining biodiversity. The change affects human health, ability to grow food, housing, safety and work. Billions of people are already more vulnerable to climate impacts, and more will be affected in the near future. For instance, conditions like sea-level rise and saltwater intrusion have reached the point where whole communities have had to relocate, and protracted droughts are putting people at risk of famine. Scientists predicted that the number of people displaced by weather-related events will rise soon.

Various global and regional initiatives are underway to mitigate and adopt climate change. Scientists and environmentalists have already conducted several research studies on this topic. They are also exploring new viewpoints to study the impact of climate change. Central banks have joined the move by introducing climate stress tests on banks and financial institutions to address climate-related risks to the financial system.

Stress tests are 'assessments of how well banks can cope with financial and economic shocks'. The tests allow supervisors or regulators to identify banks' vulnerabilities and work with those institutions to address them. Stress testing is one of the measures institutionalised by the Basel Accords after the 2008 global financial crisis to reduce economic damage from banks taking too much risk. The second pillar of the Basel Framework reinforces the first pillar by setting minimum capital requirements to determine whether banks require additional capital buffers to withstand stressed situations.

Climate stress tests are a new tool for assessing banks' resilience to transition risks arising from new policies and technologies and physical risks due to acute and chronic extreme weather events. They are based on 'different predictions of the policies that might be implemented and the ability of those policies to prevent critical temperature thresholds from being breached.'

The use of the new tool is still limited. The European Central Bank conducted an economy-wide stress test in 2021, and launched its first climate risk stress test for individual banks in January 2022. Bank of England (BoE), Federal Reserve, People Bank of China and some other leading central banks also conducted one or more climate stress tests in last three years.

Taking a cue from the global exercise, Bangladesh Bank also conducted the country's first climate stress test last year, assuming that the country's financial system may face significant challenges from climate-induced gross domestic product (GDP) slowdown in the coming years. The central bank also released the outcome of the exercise last month titled 'An Exploratory Report on Climate Stress Testing for the Banking Sector of Bangladesh.'

Before looking into the findings, getting a brief idea of the exercise method is necessary. To conduct the study, Bangladesh Bank first selected five commercial banks as a sample, and these chosen banks hold around 30 per cent of the total assets of the country's banking sector. The report is prepared based on data available as of March 31, 2024 when the banking industry's total assets stood at Tk 1,181.76 billion. Thus, the combined assets of the five sample banks were around Tk 354.60 billion during the period under review. The central bank, however, did not disclose the names of the banks, as doing so may be misleading and negatively impact the financial market.

The theoretical framework of the climate stress test assumes that climate shock would slow GDP growth through physical and transition risks. The first one is defined as domestic physical hazards from extreme natural events like river and coastal floods and cyclones and gradual changes in climate like decline in agricultural yields or water availability, sea-level rise, etc. Physical risks generally hit real estate and infrastructure, business continuity, people, food systems, international trade channels and supply chains. The last one originated from government policies and technological changes like carbon tax and renewable energy.

Due to a decline in GDP growth and the slowdown in economic activities, banks are likely to face increased credit risk as businesses and households are exposed to macroeconomic shock. The ultimate result is that banks incur higher loan losses. So, the study first tries to estimate the link between the GDP growth rate and the credit risk of banks. To do so, the researchers applied econometric-based satellite models. Then, they analyse projected GDP under various climate scenarios and the impacts of multiple risks on banks' balance sheets.

Network for Greening the Financial System (NGFS) outlines various climate scenarios, such as Net Zero 2050 and below 2°C. The first one assumes strict climate policies and innovations that limit global warming to 1.5°C, and by 2050, the global net-zero CO2 emissions will be achieved. The second one assumes a gradual increase in the intensity of climate policies, giving a 67 per cent chance of limiting global warming to below 2°C. The central bank study team has to go through a hectic technical exercise to determine how banks would be affected under various climatic situations as outlined in the scenarios.

The study's core finding is that higher damage scenarios would consistently lead to greater loan loss, indicating significant vulnerability to climate-induced GDP shocks. The study also underscores the urgent need for immediate climate action to minimise any plausible loss. The study projected the outcomes over ten years, from 2025 to 2035.

The study measures the possible loan loss due to negative impact on climate change as a Loan Loss Reserve (LLR). The estimated LLR is calculated by "aggregating loan loss reserves against each bank's non-performing and performing exposures utilising tailored capital engines." LLR is basically an income statement expense set aside as an allowance for uncollected loans and loan payments. It is used to cover various kinds of loan losses such as non-performing loans (NPL), customer bankruptcy, and renegotiated loans that incur lower-than-previously-estimated payments.

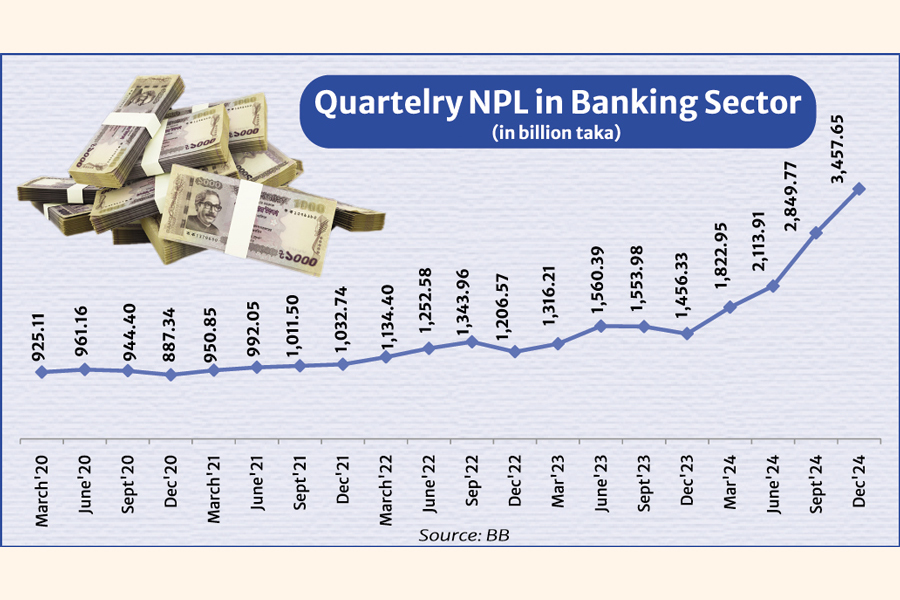

Leaving the technical aspects of the study aside, it can be said that the country's banks are gradually becoming vulnerable to climate change, and the banking sector in its totality may face a significant surge in default loans. Total default loans in the banking sector stood at Tk 3457.65 billion at the end of 2024 from Tk 1,456.33 billion at the end of 2023. In other words, climate-related vulnerability in the banking sector will enhance in the comings days. So, policymakers and different stakeholders need to pay attention in this regard. The central bank should also organise a public dissemination session decoding and explain the findings of the study.

asjadulk@gmail.com