Another fiscal year, 2025-26, to be precise, began on Tuesday with a mix of legacy burdens and achievements in the country's economy. Moving forward and achieving the desired economic growth and inflation targets by the end of the year will not be easy since there are a number of challenges. In the national budget for the new fiscal year (FY26), the finance adviser of the interim government set a modest target of 5.50 per cent growth of gross domestic product (GDP). The government wants to keep the rate of inflation at 6.50 per cent in FY26. How realistic are the targets? One needs to analyse the relevant issues, external as well as domestic, to find the answer. However, there are reasons to be hopeful of a significant growth in the upcoming fiscal year.

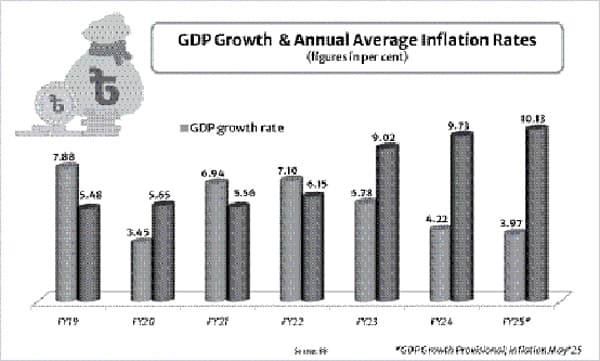

In the just-concluded fiscal year (FY25), the GDP growth rate stood at 3.97 per cent, as per the provisional estimate of the Bangladesh Bureau of Statistics (BBS). The interim government expects the rate to be 5.25 per cent in the final count. It is not unlikely that the final growth rate in the last fiscal year will exceed the five per cent mark, as the country entered a relatively stable period compared to the previous fiscal year (FY24) when the growth rate was recorded at 4.22 per cent.

In FY25, the economy experienced two sluggish phases, which reduced the growth rate. First, it was an election year, and the 12th national parliament election took place in the middle of the fiscal year. On the eve of the election, economic activities slowed down due to uncertainties about the post-election situation. It was widely known that the last national polls was yet another farcical election under the authoritarian regime of Sheikh Hasina. The regime engineered the election to stay in power for another five years.

Historical trends have shown that GDP growth typically declines during election years compared to the previous fiscal year. Since the revival of democracy in 1991, following the fall of Ershad's autocratic regime, the trend was visible until 2008. For instance, GDP growth was 5.10 per cent in FY01, which decreased to 3.80 per cent in FY02, the election year of the eighth national parliament. The trend, however, was reversed during the tenth and eleventh parliament polls held in 2014 and 2018, respectively. The GDP growth rate increased to 7.0 per cent in FY14 from 6.60 per cent in FY13 and to 7.88 per cent in FY19 from 7.32 per cent in FY18. As both polls were held in the middle of the respective fiscal years, the economy overcame the pre-poll sluggishness during the post-poll period, contributing to a rise in growth.

It is, however, essential to note that both the tenth and eleventh national elections were marred by controversy for various reasons. The Hasina government scrapped the constitutional provision for holding elections under a caretaker government in 2011 with the 15th constitutional amendment. The main reason was to make the path of being re-elected again and again without any hindrance. In the absence of a caretaker government, the Hasina-led Awami League took complete control of the administration and marginalised the main opposition, the Bangladesh Nationalist Party (BNP), by forcing it not to take part in the election. Mass rigging was recorded in these two elections. In a similar vein, the national election took place in the middle of FY24, and Hasina was re-elected as the Prime Minister for the fourth time at a stretch.

But things did not go as planned after the election as student-led protests spread gradually across the country. Initially, the protest movement was launched to abolish the quota system in government jobs. Soon, it turned into a mass movement against corruption and intimidation by the Hasian regime. Therefore, the second half of FY24, or the post-poll period, was unstable, and the economy did not recover from the pre-poll sluggishness. Although the mass movement turned into a mass uprising in July, the first month of FY25, the previous months, especially the last quarter of FY24, were volatile, with the GDP growth rate dropping to 2.14 per cent from 4.62 per cent in the third quarter of the fiscal year. The ultimate result is a sharp decline in overall GDP growth in FY24 to 4.22 per cent from 5.78 per cent in FY23.

Now, the economy has weathered the most turbulent period in the first quarter of FY25, following the mass uprising that compelled Hasina to step down and flee the country to seek shelter in India on August 5 last year. The country also sank into chaos and uncertainty for the time being, although people in general were jubilant and hopeful for a better future. The GDP growth rate decreased to 1.96 per cent in the first quarter of FY25 but then significantly rebounded to 4.48 per cent in the second quarter. The Yunus-led interim government has taken several steps to restore the economy over the past few months. Economic activities also started to pickup and the final outcome will depend on socio-political stability in the country.

The core challenges to achieving the modest target of GDP growth in the current fiscal year include higher inflation and uncertainties in global trade. The annual average rate of inflation is still above 9.0 per cent, while the monthly inflation rate has also been above 9.0 per cent (as of May 2025). The annual average inflation rate jumped in FY23 to 9.02 per cent from 6.15 per cent in FY22, reflecting monetary mismanagement and a distorted supply chain due to rent-seeking activities in the market during the Hasina regime. Inflation increased further in FY24 to 9.73 per cent. These challenges are significant and need to be addressed for the economy to thrive.

Bangladesh Bank, under the new leadership after the interim government took charge, has intensified its battle against inflation by implementing persistent rate hikes. The tight monetary stance necessitated a temporary sacrifice of growth to contain inflationary pressures. The step had paid off slowly, as the monthly inflation rate started to decline since November last when it was 11.38 per cent. The rate has dropped below 10 per cent since January this year.

As the central bank prepares to formulate and announce the Monetary Policy Statement (MPS) for the first half of FY26 (July-December), it is already seeking suggestions and opinions from individuals and institutions. The new MPS will likely set the target to keep the inflation ceiling at 6.50 per cent in sync with the FY26 budget target. It means the economy is unlikely to stay in the 'low-growth high-inflation' cycle for the third consecutive year.