Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

In the backdrop of the ongoing Covid-19 pandemic and its short-term impacts and medium to long-term implications for the recovery phase, the key policy concern emerging from the current public finance discourse relates to the creation and utilisation of 'fiscal space'.

Indeed, the concept of 'fiscal space' needs to be well-understood for all practical purposes as the government prepares the national budget for FY21. According to the International Monetary Fund (IMF), fiscal space is defined as the room for pursuing discretionary fiscal policy compared to a pre-existing baseline, without compromising market access and debt sustainability. Kose et al. (2017) understands fiscal space as the availability of budgetary resources at government's disposal to meet its financial obligations. Bhattacharya (2020) defined fiscal space as the room or extra money available within the budget which allows a government to allocate resources for a designated purpose, in view of the current scenario, to address the challenges emanating from Covid-19, without endangering macroeconomic stability.

As the national budget for FY2021 will be placed before the parliament on 11 June 2020, it has become critically important to identify the sources of fiscal space to underpin the government's intended fiscal policy stance.

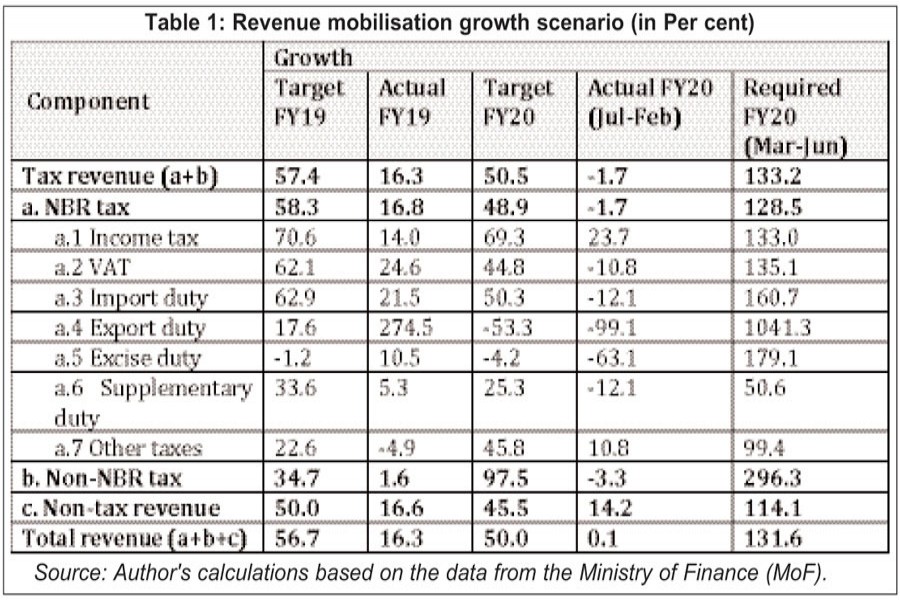

REVENUE MOBILISATION IN FY2020: The most obvious scope for creating and expanding the fiscal space originated from within the domestic resource mobilisation space. Regrettably, as can be evinced from data available in the public domain, the ongoing trends as regards revenue mobilisation do not appear to be promising by any account. During July-February of FY20, growth in terms of total revenue mobilisation was a paltry 0.1 per cent over the corresponding period of FY19 (Table 1). As the growth target for the full fiscal year was set at 50.0 per cent (over actual realisation in FY19), total revenue collection would have to increase by an astounding 131.6 per cent during the March-June period of FY20, which obviously is not going to happen. As can be discerned from Table-1, not a single component of the revenue mobilisation framework is set to attain the respective annual targets.

Indeed, the economic slowdown originating from the nationwide lockdown and the adverse impacts of the ongoing pandemic on international trade are expected to further exacerbate the situation during the rest of the period. While the extent of the consequent drawdown will be known only when the data for relevant months become available, it is not difficult to assume that fourth quarter performance will pull down the July-February trends.

National Board of Revenue (NBR) tax, which constitutes 86.2 per cent of the total targeted revenue, recorded a negative growth of (-) 1.7 per cent during the July-February period of FY20 according to the MoF data. The NBR data itself, available for up to April FY2020, however, shows a growth of 0.6 per cent compared to the corresponding period of FY19. This implies that NBR tax collection will need to grow by 196.5 per cent during the remainder of FY2020 to meet the annual target. Within the components of the NBR tax, duties at import and export stage, VAT at local level and income tax will need to increase by 303.5 per cent, 150.9 per cent and 186.8 per cent respectively during the May-June period of FY2020 to reach respective individual annual targets. Not only are such targets unattainable, given the Covid-19-induced economic slowdown, the annual growth rates will come down further.

REVENUE SHORTFALL TO SHOOT UP: CPD had earlier projected that the total revenue shortfall in FY20 may reach to Tk. 1.0 trillion. However, this projection did not fully capture the impacts of the Covid-19 pandemic given that the data was available only for the July-December period of FY2020. Based on the latest available data from MoF (i.e. July-February of FY20) and other relevant sources, the revenue shortfall figure for FY20, against the original target has been re-estimated to be around Tk. 125,000 crore. This implies, the revenue earnings in FY2020 is likely to record a minuscule growth of 0.4 percent; hence, revenue-GDP ratio may see a decline.

REALISTIC TARGETS FOR OVERALL FISCAL MANAGEMENT: As has been mentioned in several media reports, the total revenue collection target for the upcoming FY21 has been projected to be around Tk. 3.95 trillion. This target is respectively 4.50 per cent and 10.50 per cent higher compared to the original target and revised target for the ongoing fiscal year. However, if the revenue shortfall for the outgoing fiscal year is indeed Tk. 1.25 trillion, the growth target for FY21 mentioned above would be a whopping 56.2 per cent higher than what we estimate to be the case for FY20. Given that the highest annual revenue mobilisation growth during the last 10 years, recorded in FY12, was about 23.3 per cent, it can be safely argued that the target set for FY21 is also unlikely to be achieved. As a matter of fact, similar concern has also been raised by the top brass of the NBR citing the revenue implications of the economic downturn originating from the Covid-19 pandemic (Prothom Alo, 2020; The Business Standard, 2020).

In view of the above, the national budget for FY2021 must provide detailed explanation as to how the programmed revenue mobilisation target will be achieved through the proposed fiscal measures. Indeed, if the revenue mobilisation targets are not set in a realistic manner and does not reflect the reality of the situation, it will put undue pressure on the revenue collection authorities, stress the fiscal framework beyond a tolerable limit and undermine the efficacy of other relevant policy instruments. This will weaken the fiscal framework, result in misinterpretation of fiscal deficit and consequently put into question the veracity of financing of the fiscal deficit.

SUPPORT DOMESTIC DEMAND: A key objective of the government must be to use the fiscal policy to boost domestic demand, and raise disposable income and consumption, particularly of the lower- and middle-income class. In the FY2021 budget, raising the tax-free income threshold levels from Tk. 250,000 to Tk. 350,000 should be considered. Also, the first three slabs of income tax from 10, 15, and 20 per cent may be restructured to 5, 10, and 15 per cent respectively, at least for the next two years. Allowing payment of individual income taxes for FY20, by instalments, by March 2021 may also be considered. With a view to ensure food security of low-income people, reduction of import related tariffs (including AIT and VAT) on essential food items should be considered. Thus, duties on items such as onion, lentil, garlic, ginger and soybean oil etc. (where applicable) should be considered on a dynamic basis based on the evolving market scenario in terms of price, projections about production and the demand situation. Seasonal features of the production cycle should be considered to protect the interest of the farmers in this context.

BALANCING FISCAL INCENTIVES: The planned procurement and installation of the Electronic Fiscal Device (EFD) and Sales Data Controller (SDC) devices by the NBR must be accelerated in order to ensure effective implementation of the VAT and SD Act and augment revenue mobilisation. It is to be anticipated that demands for incentives will be lined up and rise in view of Covid-19.

The primary objective of all tax incentives should be to directly support the marginalised groups. The government must conduct proper cost-benefit analysis before devising any new provisions. Indeed, the government must be cautious and very selective in this regard, and should be restrained from all ad hoc provisions concerning tax incentives. Indeed, fiscal incentives provided should take cognisance the overall fiscal and monetary support measures in place with regard to particular groups of stakeholders and sectors. For example, corporate tax rate should be unchanged in view of the fact that a number of measures have already been taken in support of large entrepreneurs. Ministry of Finance has to release credible estimates of revenue forgone for all tax incentives, in a disaggregated manner.

Also, some of the existing provisions should be reviewed and discontinued if considered as being of low priority. The existing black money whitening facilities create moral hazards, discouraging honest taxpayers. CPD has highlighted this issue and made its stance clear in successive IRBDs. This provision should not be continued in the next fiscal budget.

Indeed, all types of tax evasions and illicit financial flows (IFF) will need to be curbed with a strong hand. In view of the emergent situation, it is hoped that the government will strengthen its enforcement measures in this regard. As is known, Bangladesh loses a sizable amount of resources as a consequence of IFF. Coordinated efforts by several policy actors will be required to implement the National Strategy for Prevention of Money Laundering and Combating Financing of Terrorism (NSPMLCFT) 2019-21 in all areas concerning tax evasion and IFF.

Dr Fahmida Khatun, Executive Director, Centre for Policy Dialogue (CPD);

Professor Mustafizur Rahman, Distinguished Fellow, CPD;

Dr Khondaker Golam Moazzem, Research Director, CPD; and

Mr Towfiqul Islam Khan, Senior Research Fellow, CPD.

avra@cpd.org.bd; www.cpd.org.bd

[The article is based on CPD IRBD 2020 (fifth periodic review of FY20). Research support was received from CPD IRBD team members including Md Zafar Sadique, Mostafa Amir Sabbih, Muntaseer Kamal, Md. Al-Hasan, Syed Yusuf Saadat, Abu Saleh Md. Shamim Alam Shibly, Nawshin Nawar, Tamim Ahmed, Md Jahurul Islam, Iqra Labiba Qamari, Fariha Islam Munia and Taslima Taznur]