Development, foreign assistance, foreign loans, FDI, public debt

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

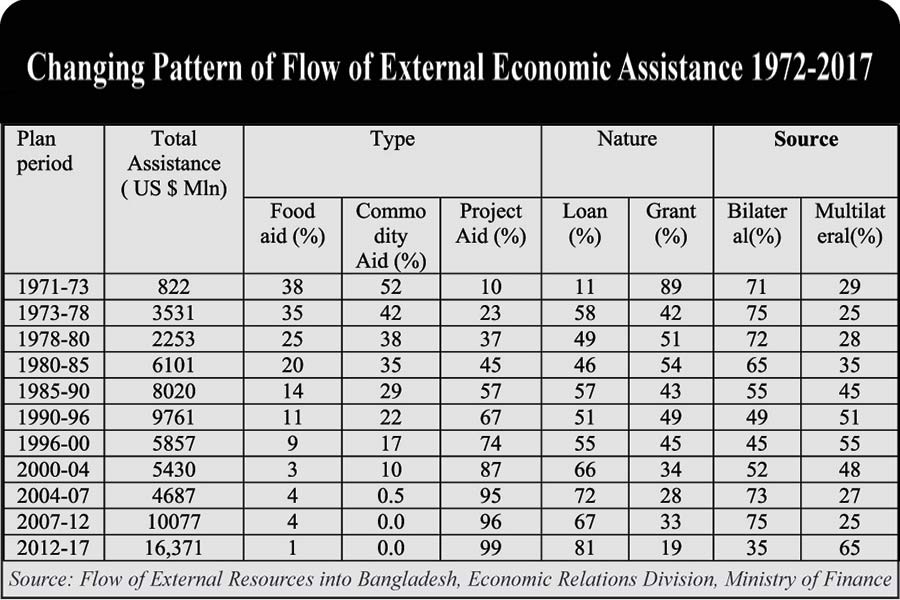

Bangladesh has been regarded from the beginning as a test case for development. In October 1974, the Bangladesh Aid Group was established under the aegis of the World Bank, with 26 participating governments and institutions. Aid to Bangladesh has remained at a high level since the consortium came into existence, although with substantial fluctuations in new commitments from year to year. In the 1980s, the value of food aid declined to around 11 to 18 per cent of new aid commitments, most of which was given on a grant basis. Commodity aid -- about 25 per cent of aid - was preferred by the large donors because their funds are put to work in well-defined ways that can be related to policy objectives. Project assistance accounted for more than 50 per cent of new commitments. Bangladesh has been unable to use project funds at the same rate as they are authorised. As a result, a pipeline of authorised but undisbursed project funds has grown bigger every year.

FLOW OF PRIVATE CAPITAL: A high level of domestic credit expansion in the government sector has resulted in a rising level of government borrowing from both the banking system and the public through the use of savings instruments. The 1974 New Investment Policy restored certain rights to private and foreign investors. In December, 1975, the Revised Investment Policy allowed greater private sector activity and authorised joint ventures with public sector corporations in a number of previously reserved areas, provided that the government retained 51 per cent ownership. The Dhaka Stock Exchange was reactivated in 1976, and the Bangladesh Investment Corporation was established the same year to provide financing for bridge construction and underwriting facilities to the private sector. Investment ceilings for private industry were abolished in 1978. Then, in 1980, the government delineated a more liberal attitude toward foreign direct investment in the Foreign Private Investment (Promotion and Protection) Act. In 1987, an amendment to the Bangladesh Industrial Enterprises (Nationalisation) Ordinance was adopted, providing the legal basis for plans to sell up to 49 per cent of government shares in remaining nationalised enterprises. An export processing zone was established officially at the port city of Chattogram in 1980 which actually began functioning in March 1983 when a programme of inducements was offered to investors opening up enterprises. In addition to the broad policies encouraging foreign investment, Bangladesh has entered into bilateral investment treaties which include such assurances as unrestricted currency transfers, compensation for expropriation, dispute settlement procedures, and taxation treatment. In addition, Bangladesh has signed agreements for the avoidance of double taxation with 32 countries.

Even with a reasonably attractive framework in place, the flow of private capital to Bangladesh has been slow. Foreign direct investment (FDI) from the Organisation for Economic Cooperation and Development (OECD) member countries averaged very insignificant. The largest amounts of FDI are from Asian countries -- Japan the foremost, with smaller amounts from South Korea, Singapore, Taiwan, and Hong Kong -- and from Britain and other countries in Western Europe.

PUBLIC DEBT: Bangladesh has been relying heavily on public debt to meet budget deficit since its independence. The government is borrowing excessively from public sources and thus negatively affecting the economy of the country. So, GDP growth rate, manufacturing sector growth rate, investment as a percentage of GDP and export as a percentage of GDP should be reviewed comprehensively to judge the impact of public debt burden (DB) on these variables.

External debt in Bangladesh increased from US$ 26.31 billion in 2016 to US$28.57 billion in 2017. External debt averaged US$20.88 billion from 2001 until 2017, reaching an all-time high of US$28.57 billion in 2017 and a record low of US$16.17 billion in 2002.

An analysis of the trend in foreign loans availed by the local private companies between 2011 and 2017 reveals that the total number of foreign loans has increased dramatically from 24 in 2011 to 134 in 2017. Similarly, the corresponding monetary value of the foreign loans also increased from a total of US$ 909.3 million to US$1,494.3 million, exhibiting a growth of almost 63 per cent over the aforementioned timeframe. Reliance of the local companies to avail loans from the Off-shore Banking Units (OBUs) of the local banks also evinced a persistent rise between 2011 and 2016, but decreased to some extent in 2017. The share of the number of loans extended by the OBUs, in the total number of foreign loans, has gradually increased from 29.2 per cent in 2011 to 61.5 per cent in 2016. However, the amount has experienced a slight fall in 2017.

FOREIGN LOANS: The readymade garments (RMG) sector dominated the scenario of foreign loans. In terms of the sectoral breakdown, the RMG sector accounted for 60.2 per cent of the total number of foreign loans, followed by the power sector with a share of 11.4 per cent.

Furthermore, hard loans have been identified based on the methodology suggested by the Organisation for Economic Cooperation and Development (OECD, 2013). The number of hard loans from the foreign sources has jumped significantly since 2016. The average maturity period has exhibited a fluctuating trend and increased from 5.2 years to 5.5 years between 2011 and 2017. In contrast, the average interest rate payable on the borrowed funds reveals a generally declining trend -from 4.6 per cent in 2011 to 3.6 per cent in 2017. Increasing number of hard loans in recent years, alongside increasing average interest rates, imply higher payment obligations in foreign currency over the coming years.

Additionally, depreciation of Bangladesh taka (BDT) in the recent past against US dollar (USD) will put further pressure on debt servicing liabilities. In this changing scenario, the current policy of allowing foreign loans, on a case by case basis, should be re-evaluated. This is also justified on account of falling interest rate in the domestic market and the need to bring back good investors within the fold of domestic financial system.

Dr Muhammad Abdul Mazid is a retired Secretary and former Chairman, NBR.