Given the current global pandemic, we are witnessing a digital transformation across the world which will only accelerate the forecasted growth of the IT industry significantly as acknowledged by the industry leaders.

The government of Bangladesh is also promoting the local IT industry especially for the banking sector and has signed an MoU with Bangladesh Bank facilitating software sale of Tk 3.0 billion in this sector for the year 2020-2022 as stated by Mr. Zunaid Ahmed Palak , the state minister for ICT division.

With the global economic slowdown and widespread budget cuts, our local banks can protect drainage of foreign currency (FC) enormously, if they go for our locally developed core banking system (CBS) and other banking / fintech solutions.

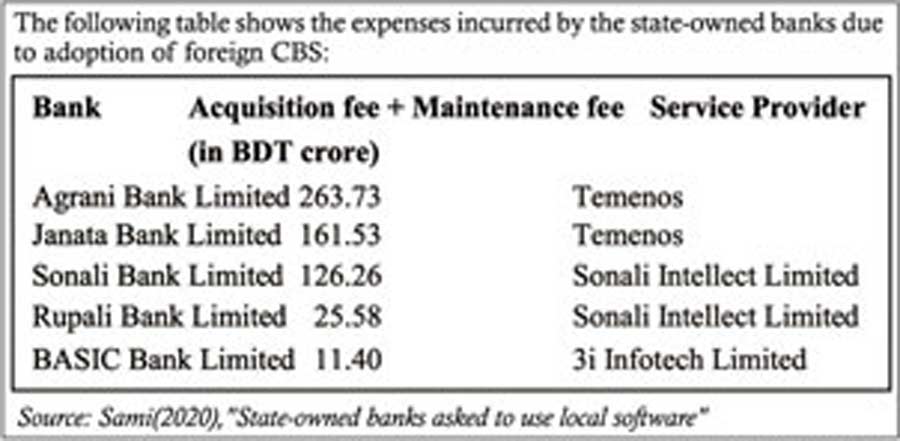

The figures in the table above excluded version upgrading and customisation fees. Every year the banks have been paying exorbitant amount as maintenance fee in foreign currency.

Besides the data in the table, there are a total of 28 banks, both public and private, that have been using foreign CBS but the private banks are yet to make their related expenses public. This might add to a big amount of foreign currency transfer every year.

On the contrary, neighbouring Indian banks are using nearly 100 per cent domestic CBS without letting their foreign currency draining away from the country. Rather, the Indian software companies are selling their home-grown products to international market or they are implementing and supporting foreign products to countries like us through becoming dealers/distributors/value added partners to those foreign CBS vendors. Many international vendors have their support and production centre in Bangalore and Chennai. The same is the case with the Philippines.

Although there could be sporadic exceptions, so far, it is observed by the industry professionals that there is not a single feature or functionality of a CBS that is in real use in Bangladesh and that can't be performed by a well-built local CBS. We certainly have a scarcity of well-built local CBS, but these are available now in limited numbers. Moreover, patronisation, support and long-term investment are required by institutions or conglomerates like in our neighbouring country to develop more such organisations and to nurture them.

Moreover, the country may see a decent growth of white collar jobs where our talented youths could have been engaged. Some 65,000 young professionals get training on ICT-related subjects every year in the country. We are producing sufficient number of engineers and IT professionals, and also high quality business graduates (required for business domain of banking application) from good universities. However, since the local solutions are not adopted or recognised by the banks and financial institutions, these resources could not be absorbed or utilised by the good software solution companies.

A relevant question is whether there is a lack of availability of local quality CBS?

It requires deep pocket, long-term investment and enormous patience to design, develop and to take a new CBS to a maturity level. Most of the entrepreneurs/ technocrats are reluctant to take such a challenge. The ROI has to be on long term basis here compared to any other enterprise software solution.

However, in India, all the local CBS gained maturity through the patronisation and collaboration of their client banks like ICICI Bank, or large visionary conglomerate like the Tata group etc.

There is a saying "by local, for locals". Local CBS has been designed with the local banks in mind. They are agile for any changes abiding by the central bank regulations. The local pool of talents understand better the needs and nature of changes required in the software suitable for the country rather than the expensive foreign consultants of outsourced foreign software companies.

On top of contributing to the country's Gross Domestic Product (GDP) by choosing local products from many perspectives, it's about knowing and understanding the origin of the product and maintaining positive relationships between the suppliers and the users. Locally sourced products usually come with the added benefit of faster delivery, often with a fraction of support and customisation cost than the foreign ones.

Core banking solution or system (CBS) is not the complete solution for a bank, it is rather the core data management system. Bank typically requires several other sub-systems that integrate with the core banking system, for example: alternative delivery channels, regulatory compliance, risk management, statutory reporting, integration with local/global FinTech eco-system, local exchange connectivity (BFTN, NPSB, Clearing etc), Agent banking, Offshore banking etc. Opting for a local solution hence offers efficiency in terms of service delivery.

For the smooth and secured financial operation prudent investment in digital transformation is extremely essential. Here investment in people, process and technology all are important, but a well-built but extensible and scalable CBS is the fundamental area to consider for the commercial banks.

A couple of banks have built their own CBS and are maintaining them with huge number of IT resource personnel, but that cannot be answer to this problem. It will not be cost-effective in the long run. Moreover, latest study suggests the business should concentrate on its own core competency. Building and maintaining software cannot be part of the core area of financial institutions. A financial institution cannot provide the environment required for a quality software company within their management framework, where fostering and nurturing talents, promoting innovation through R&D and exploration are the key success factors. Moreover, optimisation of resources in this field only could be done by a software company itself rather than a financial institution.

Identifying the existing visionary companies with robust product and having a long-term and win-win arrangement with them could be a good answer to this puzzle. Moreover, more and more such companies should be built and patronised by the financial institutions and large conglomerates.

The writer is CEO & Co-Founder, Millennium Information Solution Limited