Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

A cross the world, the most severe impact of the Covid-19 pandemic has been observed on livelihoods. During such economic downturns, historically, migrant workers get disproportionately affected. Migrants, even if not unemployed, face reduced pay, or worsened working conditions. Often xenophobic violence deepens such crisis. Being excluded from the social safety nets create additional miseries. Taking into account all such concerns, the World Bank, IMF and the Asian Development Bank (ADB) predicted that remittance outflows to the low and lower-middle-income countries might fall 20 per cent or more in 2020. According to the ADB, countries from South Asia, such as Bangladesh, Nepal, Pakistan could be the worst affected countries in the world with a fall in remittances by 26 per cent or more.

Remittance inflow to South Asian countries indeed fell during the peak of the global pandemic. For instance, total remittances received in March, April and May in Bangladesh were 12.5 per cent, 23.8 per cent and 13.9 per cent lower than the same periods the previous year (Figure 1). For the same period, the growth rate in remittances for Nepal and Pakistan was: Nepal (March: 2.3 per cent, April: -56.7 per cent, May: -38.2 per cent); and Pakistan (March: 9.9 per cent, April: 0.8 per cent, May -19 per cent). However, in contrast to the projections, such negative trends reversed in June and July 2020 for all these countries. In June, remittance receipt in Bangladesh increased by 34 per cent, while this rate was 9.4 per cent for Nepal, and 51.2 per cent for Pakistan. The trend continued for these countries in July and August: Bangladesh (July: 62.6 per cent; August: 35.9 per cent), Nepal (July: 22.2 per cent), Pakistan (July: 36.5 per cent; August: 24.4 per cent). A similar trend has been observed for other major remittance-receiving countries such as the Philippines.

There are a couple of reasons behind such observed trends. The fall in remittances in the April-May is the direct result of strict measures taken in the destination countries closing businesses and restricting movements. For Bangladesh and Pakistan, the rise in remittances in the months of May-July 2020 could be partly due to the Eid festivities - as it has been the case in the earlier years. Remittance to the country usually peaks up in the Eid month or immediate previous month of the Eid (Figure 2). Also, remittance is usually counter-cyclical: people remit more during economic hardships back at home. However, this might seem puzzling as the COVID-19 pandemic has affected all countries alike, and therefore the workers in the destination countries are also in woes.

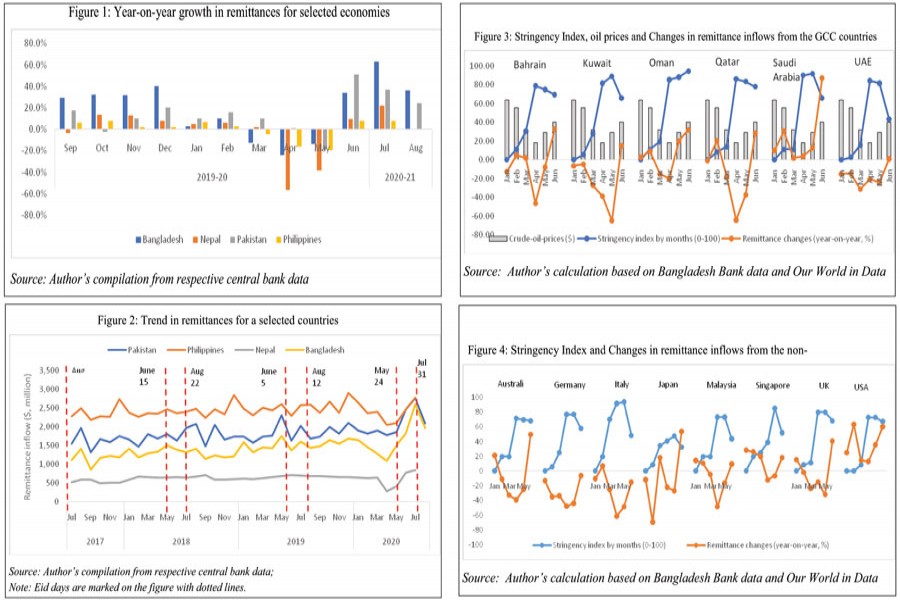

We observe a systematic pattern for Bangladesh (Figure 3 and Figure 4). The remittance inflow to Bangladesh started declining from December 2019 due to the falling oil prices. Between December'19-April'20, the oil price nosedived from $67.2 to $18.4 per barrel. Consequently, remittance growth from GCC countries (except Saudi Arabia) remained negative for the first five months of 2020 on year-on-year basis. For the non-GCC countries, remittance receipt saw a large dip in March-May 2020. The only two countries for which remittance growth remained positive throughout the time are the USA and Saudi Arabia. On year-on-year basis, remittances from the USA to Bangladesh was 35.5 per cent higher in May and 60 per cent higher in June. Similar growth in remittances from the USA is observed for the Philippines, and countries in Central America (Mexico, Nicaragua, Honduras) etc. To some extent, the flow from the US might be a result of the federal unemployment benefits package undertaken by the US government.

However, the case is different for Saudi Arabia (KSA). On year-on-year basis, remittance growth from KSA to Bangladesh in March (1.9 per cent) and April (3.7 per cent) were record low in the recent past. In contrast, remittance growth in June and July were record highest (86.9 per cent and 91.7 per cent higher than the previous year, respectively). Such high remittance flows from the KSA have been observed for Nepal and Pakistan as well. Since the onset of the crisis, an estimated 467 thousand foreign workers have left KSA, and another 1.2 million could be leaving by the end of 2020. Many of the workers in the KSA have already lost their jobs and might be sending off their all remaining savings back to the country.

The situation is similar for the other GCC countries. With continued slump in the global oil market coupled with the pandemic, the employment in the region is expected to decline by 13 per cent. Some estimates show that 3.5 million foreign workers from these countries could face forced return. Moreover, with tapered economic opportunities, resentments towards foreign workers have increased in these countries. The ongoing reform plans in the UAE and Kuwait activating a quota system reducing the number of foreign workers might add an extra blow to it. The situation might worsen further in the coming months if the second wave of the Coronavirus affects the major migrant destinations in addition to the GCC countries, such as Malaysia, Singapore, South Korea etc. Given that majority of the workers at the destination countries live in over-crowded shelters, a second wave of the virus would also mean a serious health concern.

The fall in employment in the foreign markets will have long-lasting impacts at the source countries. Each year, Bangladesh needs to create approximately 2 million new jobs. Around 40 per cent of this need is filled in by overseas opportunities. Since March 2020, regular migration remained almost closed for all countries. Between January-August 2020 Bangladesh sent only 181 thousand workers compared to 441 thousand workers a year ago. Meanwhile, another 141 thousand workers returned to the country. In the case of India, which needs to generate as many as 12 million jobs each year, the challenge could be more crucial.

With a declining stock of migrant workers at the destination countries, the growth in remittance inflows in the coming years could slow down significantly. This might bring more serious macroeconomic consequences for countries like Nepal, where remittance is the single most source of foreign earnings. Furthermore, a fall in remittances will have detrimental impacts on poverty, nutrition, child labour, as well as human development. Also, falling out of jobs at the destination countries could trap these workers in a vicious circle of debt for years to come.

For combating the challenge of repatriating migrant workers, policies should be taken at four fronts. First, arranging special programmes for the returnee migrant workers, re-skilling them and re-integrating them in the domestic labour market. If required, collaboration should be sought from development partners and other development agencies. Second, governments should incentivise remittances, and at the same time, reduce remittance transaction costs. For instance, the initiative from the Government of Bangladesh in providing 2 per cent remittance incentive, reducing the number of papers required in claiming the incentive, or the loan facilities for the returnee migrant workers, all seem appropriate and timely. However, the GoB needs to be vigilant in ensuring that the schemes are functioning properly as desired. Third, a large number of the returnee migrant workers could be already indebted with loans (taken during migration but not paid yet). This phenomenon requires special attention from the policymakers. Last but not least, the host countries also should take up measures towards safeguarding the migrant workers. Retaining jobs of the migrant workers might help the destination countries in reviving their economies.

Mahtab Uddin is a Lecturer of Economics at the University of Dhaka and Research Fellow at SANEM.

This is a part of an on-going research on the subject matter.